February 2, 2004

Volume 2004: Issue 1

Current Statistics (02-02-2004)

The Employment Picture

Unemployment Rate ({6.0% Oct }…{5.9% Nov })…{5.7% Dec}

The December Unemployment Rate came in at 5.7%. According to the Bureau of Labor Statistics, unemployment dropped from 6.4% in June to 5.7% (Seasonal adjusted measure) of the labor force in December, constituting a significant and continued brightening in the employment picture.

When looking at the numbers based on Job Creation, the performance of the economy has been less than bright: October was adjusted down from 137,000 to 100,000; November from 57,000 to 43,000; and December coming in at a paltry 1,000 jobs. This leaves the net Jobs Creation/Loss at -74,000 for 2003.

While the unemployment rate dropped 0.2% in December, the lack of job creation has left many to wonder what is going on. The answer to that is likely to lie more in the increased numbers of people either retiring or re-retiring (as the stock market has rebounded), rather than any significant increase in job seekers giving up on hope of employment (we are well past the discouraged worker effect phenomenon at this stage of the recovery/expansion). In addition, the Department of Labor instituted information gathering and reporting changes around June 2003. In implementing those changes, and tying out year-end numbers, the December numbers appeared to be skewed badly; the changes had ripple effects going back several years.

Speaking of structural unemployment…

In his teleconference speech before the HM Treasury Enterprise Conference, London, England on January 26, 2004, Chairman Greenspan noted, "We can thus be confident that new jobs will displace old ones as they always have, but not without a high degree of pain for those caught in the job-losing segment of America's massive job-turnover process."

FRB: Speech, Greenspan--Economic flexibility--January 26, 2004

for entire transcript of address

Weblink URL address: http://www.federalreserve.gov/BoardDocs/speeches/2004/20040126/default.htm

Jobless Claims

(4-wk rolling avg: 347,750 Jan-15, to 345,250 Jan-22, to 346,000 Jan-29)

The new Jobless Claims data came in at a 342,000 for the week ending January 29, 2004 a decrease in claims of 1,000 from the previous week's 343,000. The much-watched four-week average increased slightly for the week ending January 29, 2004.

According to Labor, "The advance number of actual initial claims under state programs, unadjusted, totaled 386,263 in the week ending Jan. 24, a decrease of 104,269 from the previous week. There were 434,888 initial claims in the comparable week in 2003."

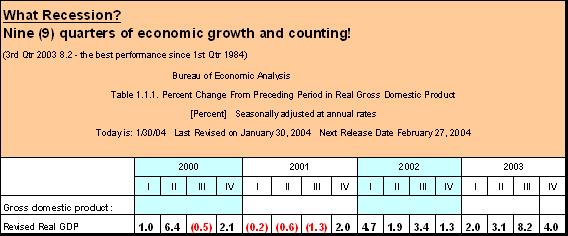

GDP (4th Quarter 2003 Real GDP: 4.0% - Preliminary)

The preliminary numbers for the fourth quarter of 2003 showed continued positive growth in real GDP. The Commerce Dept. reported a 4.0% growth rate for the 4th Quarter 2003 (on an annualized basis). It marked the 9th consecutive quarter of economic expansion. The 4th Quarter 4.0% rate is a respectable number, given the 8.2% growth in the preceding quarter. Again, the GDP growth was spread across the board, but Personal Consumption Expenditures (PCE) off, going from a 6.9% growth in the third quarter to a 2.6% increase in the fourth. Likewise, durable goods purchases rose 0.9% in the fourth quarter versus a 28.0% growth in the third. Much of the changes in fourth quarter were attributable to the expenditures on autos (down in terms PCE) and automotive investment (up in the area durable goods - motor vehicle inventory investment). Updated 4th Quarter GDP numbers will be released in February 2004.

According to figures released by the Conference Board on January 22, "The leading index increased by 0.2 percent in December. This index increased 0.2% in November and 0.5% in October. "The leading index has now increased at a 4.7 percent annual rate from its most recent low in March, and this pickup has continued to be widespread."

Construction (put in place)

The most recent data from the Census Bureau shows continued strong levels of construction put in place. The December figure of $933.2 billion annualized, shows an increase of 0.4% above the November numbers. Additionally, the 2003 data is 4.3% above that of 2002. This amounts to an annual amount of $898.2 billion for construction in 2003. This sector continues to perform strongly through the current expansion.

New Housing Starts

The most recent U.S. Census Bureau data available shows continued near record levels of new housing starts. The December figures are running at a seasonally adjusted annual rate of 2.088 million units, 1.7 percent higher than the 2.054 million-unit revised rate reported for November. An estimated 1.848 million units were started in 2003. This is 8.4% higher than December 2002 figure of 1.705 million units.

New Residential Sales

According to the Census Bureau, sales of new homes dropped from November's numbers of 1.117 million units, to 1.060 million units (on a seasonally adjusted annualized basis) in December, representing a fall-off of 5.1%. This rate exceeds the December 2002 figure of 1.052 million units by 0.8%.

Durable Goods

The most recent report from the Commerce Department shows that New Orders for Manufactured durable goods decreased 0.2% in December (excluding defense) to $181.4 billion. Excluding defense, new orders decreased 2.9% (excluding transportation, new orders were down 0.7%). For year 2003, new orders were 2.8% above 2002.

Shipments increased at a 0.6% rate or $1.2 billion. This followed a 0.3% increase for November. For the year 2003, shipments were 0.8% above 2002.

Unfilled orders increased 0.4%, or $2.0 billion, with transportation leading the way at 0.8%. This followed an increase of 0.7% in November.

Meanwhile, Inventories increased 0.2% in December, reversing the November decrease of 0.3%.

Capital Goods Industries:

Defense, new orders increased 0.1% to $9.2 billion; shipments increased $0.2 billion or 2.9% to $7.7 billion; unfilled orders increased $1.5 billion or 1.1% to $138.2 billion; inventories increased by $0.3 billion or 0.2% to $105.2 billion.

Nondefense new orders increased by $0.1 billion or 0.2% to $58.1 billion; shipments decreased by $0.1 billion or 0.2% to $58.7 billion; unfilled orders decreased by $0.6 billion or 0.3% to $220.6 billion; and inventories fell by $0.2 billion or 0.2% to 105.2 billion.

The durable goods measure continues to be a volatile indicator and will likely continue in this manner.

Current Account Balance (Trade Balance)

The Current Account Balance consists of the Trade Balance (Net Exports (Exports less Imports) of Goods and Services), the Income Balance (Income Receipts and Income Payments), and net Unilateral Current Transfers. The Department of Commerce publishes the Current Account Balance data on quarterly basis.

As reported by the Commerce Department on January 14, 2004, the trade deficit in November 2003 stood at $38.0 billion, shrinking by (8.7%) $3.6 billion from the $41.6 billion (revised) reported for October 2003. November exports were at $90.6 billion up by $2.5 billion from $88.1 billion revised figure for October. Imports were at $128.6 billion, down $1.0 billion (rounding) from the revised $129.7 billion reported for October.

On a good note, exports have improved from October, growing by 2.8%.

Imports, improved from last month, dropping 0.8% from October.

The "better" part of the ugly news is that while the trade balance continues to remain in deficit territory, it improved significantly, dropping 8.7% in November (attributable more to increasing exports, than to diminishing imports).

CPI 0.2% / PPI 0.3% (Seasonally adjusted)

CPI - On a seasonally adjusted basis, the CPI-U (all urban consumers), which had declined 0.2% in November, rose 0.2 percent in December. Much of the increase in costs for the month and the year were in the areas of energy, food (beef) and medical care.

PPI - On a seasonally adjusted basis, the Producer Price Index for Finished Goods increased 0.3 percent in December. This increase culminated in a year-end 2003 unadjusted number of 4.0% (Finished Goods). Finished Consumer Food rose a 7.7% for the year, while Finished Energy Goods rose 11.5% (Dec 2002 - Dec 2003).

While low inflation continues to be the rule rather than the exception, it will be interesting to see if upward pressure from the Producer Price end will manifest itself in the CPI in 2004:

{PPI (Finished Goods) 2001 - 2002 = 1.2%; 2002 - 2003 = 4.0%}

{CPI (All Urban Consumers) 2001 - 2002 = 2.4%; 2002 - 2003 = 1.9%}

Until now, this inability for producers to pass on price increases to the consumer is further evidence of New Paradigm in action.

Productivity, Unit Labor Cost and Compensation (Seasonally Adjusted)

No change in this indicator from last month, but it's worth a replay…

According to a Department of Labor report, published on December 3, 2003 Productivity gains amounted to 9.4% for the 3rd Quarter 2003. This was revised from the November estimates of 8.1%, adding to the 7 percent gain from the second quarter. Unit Labor Cost was revised downward from -4.6% to an incredible -5.8%, versus a 3.2 percent drop in the second quarter. Lastly, Compensation was revised down from a 3.1% in the third quarter to 3.0%, down from 3.6 in the second quarter.

In keeping with the New Paradigm, this is the best quarterly productivity increase in more than twenty years (2nd Quarter 1983).

10-year U.S. Government Bond Rate

The 10-year Maturity U.S. Government Security continues to remain trading at a relatively low rate. For the month of December 2003, the yield averaged 4.27 percent.

The 10-year rate continues to remain at low yield levels, trading in the low 4.0 - 4.5% range.