***volume

December 23, 2011

For a downloadable version, click the following:

MR. OBAMA'S ANALYSIS OF THE EFFECTIVENESS OF FISCAL POLICIES pdf

A CASE STUDY IN HISTORICAL REVISIONISM; MR. OBAMA'S ANALYSIS OF THE EFFECTIVENESS OF FISCAL POLICIES

Judge Learned Hand

en.wikiquote.org/wiki/Learned_Hand

Anyone may arrange his affairs so that his taxes shall be as low as possible; he is not bound to choose that pattern which best pays the treasury. There is not even a patriotic duty to increase one's taxes. Over and over again the Courts have said that there is nothing sinister in so arranging affairs as to keep taxes as low as possible. Everyone does it, rich and poor alike and all do right, for nobody owes any public duty to pay more than the law demands.

PART TWO OF A THREE PART SERIES

Earlier in December, the president of the U.S. of A. kicked off his campaign for re-election by giving us a lesson in historical revisionism. In a nutshell, he asserted that his economic policies have been and are working, while George Bush's, Ronald Reagan's, etc., did not. Come on Mr. President, give us a break! Here are some of Mr. Obama's revisionist tidbits.

Now, just as there was in Teddy Roosevelt's time, there's been a certain crowd in Washington for the last few decades who respond to this economic challenge with the same old tune. "The market will take care of everything," they tell us. If only we cut more regulations and cut more taxes - especially for the wealthy - our economy will grow stronger. Sure, there will be winners and losers. But if the winners do really well, jobs and prosperity will eventually trickle down to everyone else. And even if prosperity doesn't trickle down, they argue, that's the price of liberty.

It's a simple theory - one that speaks to our rugged individualism and healthy skepticism of too much government. It fits well on a bumper sticker. Here's the problem: It doesn't work. It's never worked. It didn't work when it was tried in the decade before the Great Depression. It's not what led to the incredible post-war boom of the 50s and 60s. And it didn't work when we tried it during the last decade.

I mean, understand, it's not as if we haven't tried this theory. Remember in those years, in 2001 and 2003, Congress passed two of the most expensive tax cuts for the wealthy in history. And what did they get us? The slowest job growth in half a century. Massive deficits that have made it much harder to pay for the investments that built this country and provided the basic security that helped millions of Americans reach and stay in the middle class: things like education and infrastructure, science and technology, Medicare and Social Security.

-- President Obama, Dec. 6, 2011

Remarks by the President on the Economy in Osawatomie, Kansas

This re-election campaign speech was apparently so in conflict with the reality of history that a writer for the Washington Post, hardly a bastion of conservatism, took issue with the President's remarks: our hats off to Glenn Kesslerat, his editor, and the Washington Post. Maybe we are witnessing a re-birth in responsible journalism.

The Fact Checker – Washington Post

Obama's Kansas speech: some suspect facts

Posted by Glenn Kesslerat 12/06/2011

www.washingtonpost.com/blogs/fact–checker/post/obamas

Inserting the words "for the wealthy" was interesting phrasing by the president, since he suggests these tax cuts were intended to benefit only the rich.

Glenn Kesslerat goes on to say that the focus of the 2001 tax cuts were on marginal tax rates affecting the middle class (i.e., tax credits and elimination of marriage penalty), and while the 2003 tax cuts included reduced taxes on dividends and capital gains, he also noted that while the higher income earners reaped benefits, they also paid the lion's share of the income taxes.

Kesslerat also noted:

The Bush tax cuts were certainly large..the John F. Kennedy tax cut of 1964 (-1.90 percent) and the Ronald Reagan tax cut of 1981 (-1.40 percent) were larger than Bush's 2001 tax cut (-0.80 percent.) But all of Bush's tax cuts in 2001, 2002 and 2003 combined would equal -2.00 percent.

As we have begun to review, in this three part series on this website, the policies of Franklin Delano Roosevelt the 32nd President of the U.S. of A. We saw that FDR initially out 'Hoovered' Herbert Hoover in policies of fiscal austerity to control budget deficits caused by a significant increase in spending and slumping tax revenues from a depressed level of economic activity.

We focus on the past policies because in the social sciences we cannot experiment as they can and do in the physical sciences. We can only evaluate the habits of people; we cannot put their minds into a glass apparatus and heat it with a gas flame. What we can do is to look at the past as social experiments to see what works and does not work.

In the third and last article in this series to be posted in a few days, after this one, we will suggest what policies seem to work and why so and which do not seem to work and the reasons for their failure. While some may view President Obama's coziness toward a growing role for government such as he sees as the European way to redistribute the income and wealth, this policies do not usually reduce the instability in the economy nor do they reduce the unemployment rate appreciably. Priorities for creeping socialism and creeping egalitarianism account for the impasse between Congress and the White House. Please be patient and continue this journey with us through economic history. Since the rising federal debt increasingly blankets other issues, an examination of the use of debt by business, households and governments is critical in establishing fiscal policy priorities as there are similarities running through Hoover, Roosevelt, Clinton and Obama policy pronouncements. The fruit of these efforts will be seen in the final article in this series.

High Taxes and High Budget Deficits

The Hoover–Roosevelt Tax Increases of the 1930s (March 2003)

by Veronique de Rugy, Fiscal Policy Analyst, Cato Institute

www.cato.org/pubs/tbb/tbb–0303–14.pdf

After the crash and a sharp monetary contraction that pushed the economy into the Great Depression, the lessons of Mellon's successful tax cuts were forgotten. Presidents Hoover and Roosevelt pursued large tax increases based on the mistaken ideas that the budget should be balanced during a contraction and that high tax rates would achieve that goal.

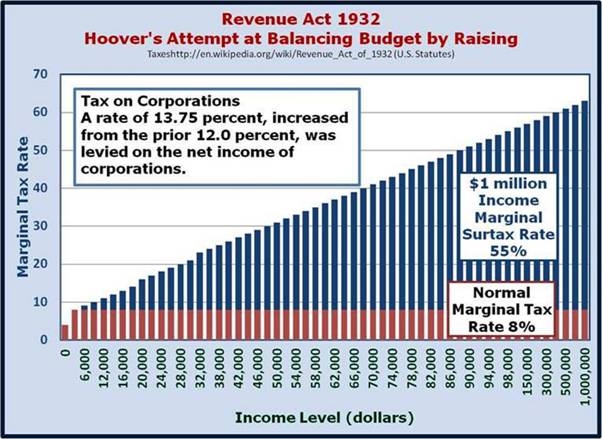

Veronique de Rugy goes on to say that in the Revenue Act of 1932, signed into law by Herbert Hoover, individual tax rates rose from 25% to 63% at the highest level.

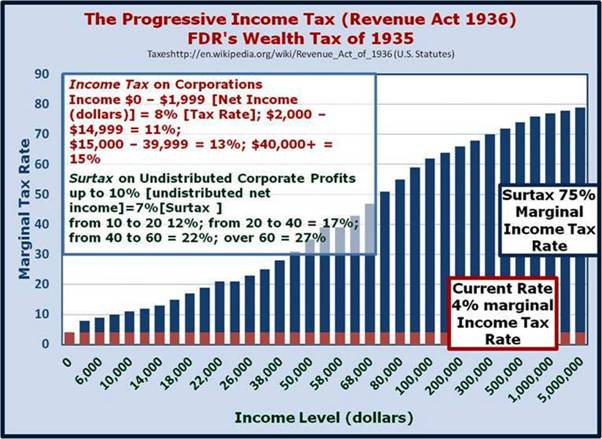

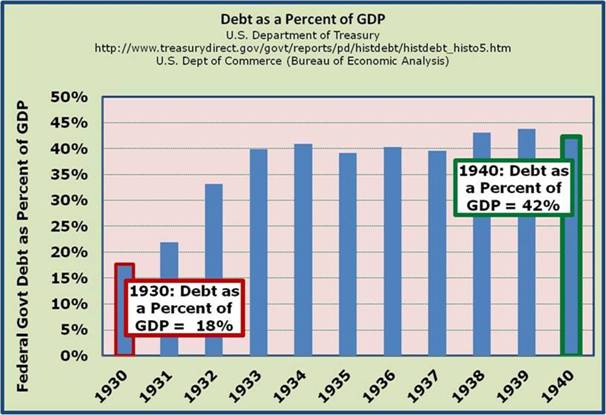

Likewise, FDR followed on with a relish, and with passage of the Revenue Act of 1936, the highest marginal income tax rate went to 79% while reducing exemptions and earned income credit at the lower end. By 1940 the federal corporate income tax rate rose to 24% from its 12% level in 1930. Roosevelt also signed laws introducing or raising excise taxes on dividends, a capital stock tax, liquor taxes and higher estate taxes (inter-generational transfer of wealth).

Another reason that tax rate increases do not succeed in balancing the budget is that they shrink the tax base by reducing economic growth and spurring greater tax avoidance. As a result, the government typically gains only a fraction of the revenues it hopes to receive. Thus Hoover was tragically misguided when he advised in 1933 that it is obvious that the budget cannot [be] balanced without a most substantial increase in revenues.

en.wikipedia.org/wiki/Revenue_Act_of_1932

The Hoover Analogy Flunks

by Alan Reynolds

en.wikipedia.org/wiki/Revenue_Act_of_1932

www.cato.org/publications/commentary/hoover

President Herbert Hoover asked for a temporary tax increase…in June 1932, raising the top income tax rate from 25% to 63% and quadrupling the lowest tax rate from 1.1% to 4%. That didn't help confidence or the Treasury. Revenue from the individual income tax dropped from $834 million in 1931 to $427 million in 1932 and $353 million in 1933.

FDR Tax Hikes

Revenue Act of 1935

en.wikipedia.org/wiki/Revenue_Act_of_1935

- The Revenue Act of 1935, 49 Stat. 1014 (Aug. 30, 1935), raised United States taxes on higher income levels, gifts, estates and corporations, by introducing the "Wealth Tax". It was a new graduated tax that took up to 75 percent of the highest incomes in taxes,[1] starting at incomes above $50,000.

- It was signed into law by President Franklin D. Roosevelt to generate needed funds for the projects of his Second New Deal.

- The 1935 Act also was popularly known at the time as the "Soak the Rich" tax.[2] Many wealthy people used loopholes in the existing tax code to evade these taxes, and the Revenue Act of 1937[1] cracked down on this by revising tax laws and regulations.[1]

The Revenue Act of 1936

en.wikipedia.org/wiki/Revenue_Act_of_1936

- The Revenue Act of 1936, 49 Stat. 1648 (June 22, 1936), established an "undistributed profits tax" on corporations in the United States.

- It was signed into law by President Franklin D. Roosevelt.

- The act was applicable to incomes for 1936 and thereafter.

The Revenue Act of 1940

en.wikipedia.org/wiki/Revenue_Act_of_1940

- The Revenue Act of 1940 temporarily and permanently increased individual income tax rates, temporarily and permanently increased corporate tax rates (top rate rose from 19% to 33%), and temporarily increased most excise tax rates to 30-50%.

- The personal exemption fell from $2,500 to $2,000 (married couples).

The Revenue Act of 1941

en.wikipedia.org/wiki/Revenue_Act_of_1941

- The Revenue Act of 1941 permanently extended the temporary individual, corporate, and excise tax increases of 1940, increased the excess profits tax by 10 percentage points (top rate rose from 50 to 60 percent) and increased corporate tax rates 6-7 percentage points (top rate increased from 24 percent to 31 percent).

- Some excise taxes were temporarily increased (on alcohol, tires, etc.) and the personal exemption fell from $2,000 to $1,500 (for married couples).

The Revenue Act of 1942

en.wikipedia.org/wiki/Revenue_Act_of_1942

- The United States Revenue Act of 1942, Pub. L. 753, Ch. 619, 56 Stat. 798 (Oct. 21, 1942), increased individual income tax rates, increased corporate tax rates (top rate rose from 31% to 40%), and reduced the personal exemption amount from $1,500 to $1,200 (married couples). The exemption amount for each dependent was reduced from $400 to $350.

- A 5% Victory tax on all individual incomes over $624 was created, with postwar credit.

- The 35-60% graduated rate schedule for excess profits tax was replaced with a flat 90% rate.

- The Act also created deductions for medical expenses.[1]

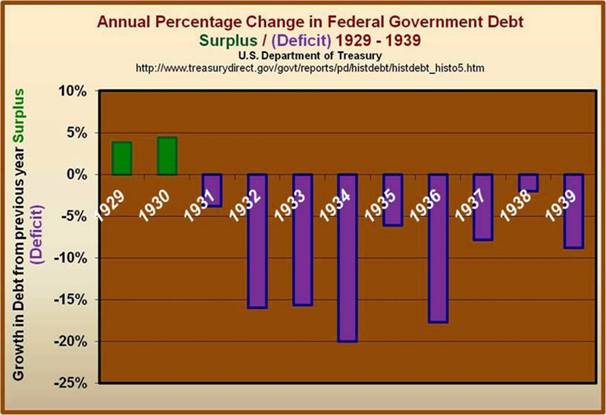

In 1932 election campaign, FDR argued for instituting a policy of fiscal austerity and argued for raising taxes to control budgetary deficits much as Mr. Obama has been preaching for his three years in office. But the behavior of the economy from the time of FDR shows such policies as failures, if not immediately, with a lagged impact on the economy.

In the1932, Congress enacted the recommendations of Hoover (and blessed by FDR) and tax rates rose. Not having the desired effects, FDR's policy recommendations turned from those of fiscal austerity to significant increases in spending.

High Taxes and High Budget Deficits

The Hoover–Roosevelt Tax Increases of the 1930s (March 2003)

by Veronique de Rugy, Fiscal Policy Analyst, Cato Institute

The scale and scope of the 1930s tax increases were extraordinary. Hoover and Roosevelt argued that large tax increases were necessary to balance the federal budget. Hoover proclaimed repeatedly, that "nothing is more necessary at this time than balancing the budget."¹ Although Hoover believed in restraining spending, he also believed in large "temporary" tax hikes. Roosevelt argued that "we should plan to have a definitely balanced Budget…and seek a continuing reduction of the national debt," and blamed Hoover for not increasing taxes enough.²

- Message to Congress, May 5, 1932, in State Papers and other Public Writings of Herbert Hoover, ed. William Starr Myers (New York: Doubleday, Doran, 1934).

- Annual Budget Message, January 3, 1934, in Public Papers and Addresses of Franklin D. Roosevelt, ed. William Starr Myers (New York: Random House, 1938).

www.presidency.ucsb.edu/ws/index

The willingness of our people to accept this added burden on these times in order impregnably to establish the credit of the Federal Government is a great tribute to their wisdom and courage. While many of the taxes are not as I desired, the bill will effect the great major purpose of assurance to the country and the world of the determination of the American people to maintain their finances and their currency on a sound basis.

Note: As enacted, the Revenue Act of 1932 (H.R. 10236), approved June 6, 1932, is Public, No. 154 (47 Stat. 169)

Read more at the American Presidency Project: Herbert Hoover: Statement on Signing the Revenue Act of 1932.

www.presidency.ucsb.edu/ws/index

Statement on Signing the Social Security Act.

August 14, 1935

Read more at the American Presidency Project:

www.presidency.ucsb.edu/ws/index

This social security measure gives at least some protection to thirty millions of our citizens who will reap direct benefits through unemployment compensation, through old-age pensions and through increased services for the protection of children and the prevention of ill health.

We can never insure one hundred percent of the population against one hundred percent of the hazards and vicissitudes of life, but we have tried to frame a law which will give some measure of protection to the average citizen and to his family against the loss of a job and against poverty-ridden old age.

This law, too, represents a cornerstone in a structure which is being built but is by no means complete. It is a structure intended to lessen the force of possible future depressions. It will act as a protection to future Administrations against the necessity of going deeply into debt to furnish relief to the needy. The law will flatten out the peaks and valleys of deflation and of inflation. It is, in short, a law that will take care of human needs.

Citation: Franklin D. Roosevelt: Statement on Signing the Social Security Act., August 14, 1935. Online by Gerhard Peters and John T. Woolley, The American Presidency Project. www.presidency.ucsb.edu/ws

Read more at the American Presidency Project:

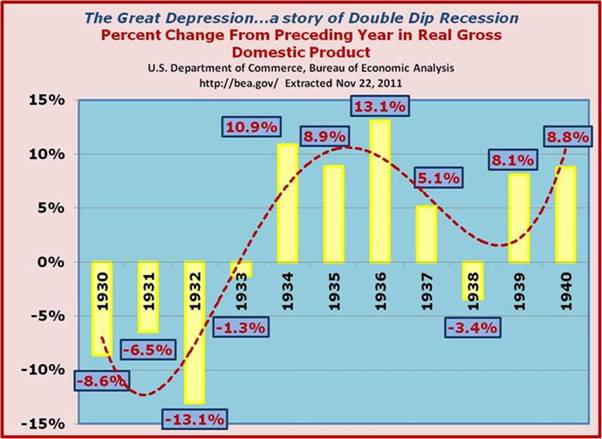

The economy began to recover for a while but with a resulting significant increase in the national debt. To combat the rising deficits and national debt, FDR once again turned to fiscal austerity and the economy collapsed again in 1937 in what is now referred to as a double dip.

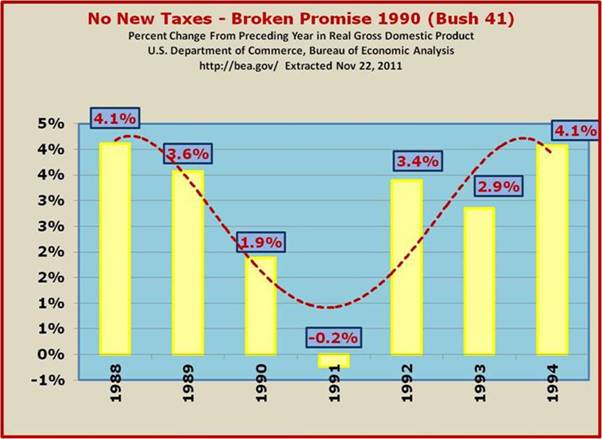

Not remembering the lessons of history, Congress under the acquiescence of George Bush 41 of 'read_my_lips:_no_new_taxes' fame, enacted taxes increases and caused the economy to collapse during Bush's last year.

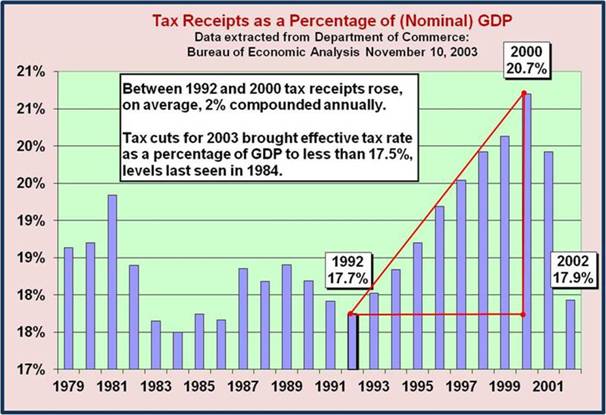

History would repeat itself again when President Clinton and his Treasury Secretary, Lloyd Bentsen (and later Robert Rubin), convinced Congress to enact significant tax increases in 1993. They appeared to be working in terms of deficit reductions but alas, the inevitable occurred and in Clinton's last year in office, the economy went from significant real economic growth peaking in 1998-99 to a tumultuous crash in 2000.

WHAT IS HAPPENING IN THE CRADLE OF DEMOCRACY?www.econnewsletter.com/jul262011.html

When Clinton became President in 1993, he inherited an annual federal deficit of $290 billion (1992) and a U-3 unemployment rate of 7.5% (1992). In 1995, he appointed Robert Rubin as Secretary of the Treasury (http://en.wikipedia.org/wiki/Rubinomics). He and President Clinton lobbied Congress to dedicate the higher taxes legislated in 1993 toward reducing the federal deficit and they agreed with him.The Financial Fiasco of Two-Thousand Eight (FFTTE)

January 2, 2009

www.econnewsletter.com/jan022009.html

The rapidly rising tax revenues resulting from several years of tax rate increases recommended by the Treasury Secretary Robert Rubin were turning the Federal Government Budget deficit into a surplus and applying a heavy duty braking to the U.S. economy. A growing trade deficit was also applying additional braking to the economy. Shortly after the FED joined the orgy of policy restraints, the economy collapsed in the third quarter of 2000. It fell from a real growth rate of 7.3% in the Fourth Quarter of 1999 to a negative real growth rate of 0.5% in the Third Quarter of 2000 – not 2001.

Clinton Tax Hike – Omnibus Budget Reconciliation Act 1993

en.wikipedia.org/wiki/Omnibus_Budget_Reconciliation_Act_of_1993

- It created 36 percent and 39.6 income tax rates for individuals in the top 1.2% of the wage earners.

- It created a 35 percent income tax rate for corporations.

- The cap on Medicare taxes was repealed.

- Transportation fuels taxes were raised by 4.3 cents per gallon.

- The taxable portion of Social Security benefits was raised.

- The phase-out of the personal exemption and limit on itemized deductions were permanently extended.

- Part IV Section 14131: Expansion of the Earned Income Tax Credit and added inflation adjustments

It would be wise to remember the criticism of Henry Morgenthau (FDR's Treasury Secretary), that FDR's policies were failures and the unemployment rate remained high until the military draft during which nearly 8 million, many of whom were unemployed, became members of the armed forces.

econnewsletter.com/dec102011.html

William Beach January 14, 2009

Henry Morgenthau Jr. — close friend, lunch companion, loyal secretary of the Treasury to President Franklin D. Roosevelt — and key architect of FDR's New Deal.

We have tried spending money. We are spending more than we have ever spent before and it does not work.

I say after eight years of this Administration we have just as much unemployment as when we started. … And an enormous debt to boot!

The date: May 9, 1939. The setting: Morgenthau's appearance in Washington before less influential Democrats on the House Ways and Means Committee.

www.econlib.org/library/Enc/GreatDepression.html

Great Depression

by Gene Smiley

It is commonly argued that World War II provided the stimulus that brought the American economy out of the Great Depression. The number of unemployed workers declined by 7,050,000 between 1940 and 1943, but the number in military service rose by 8,590,000.

This historical review is building a case for tax rate reductions, not increases. To the extent that reducing the huge deficits should occur to prevent a further slide toward an unacceptably high degree of sovereign risk and an eventual Federal Government default on its debt, cuts in spending rather than increases in tax rates is the only solution as history shows us. These policy issues will be the focus of the third in this series on this website.

Let's now take a look at the history in terms of tax cuts to stimulate the economy. Such a policy was instituted by Andrew Mellon the Treasury Secretary under President Coolidge, and more recently popularized by Arthur Laffer.

Taxation – President Coolidge

en.wikipedia.org/wiki/Calvin_Coolidge

Coolidge's taxation policy was that of his Secretary of the Treasury, Andrew Mellon: taxes should be lower and fewer people should have to pay them… the Revenue Act of 1924, which reduced income tax rates and eliminated all income taxation for some two million people. They reduced taxes again by passing the Revenue Acts of 1926 and 1928, all the while continuing to keep spending down so as to reduce the overall federal debt. By 1927, only the richest 2% of taxpayers paid any federal income tax. Although federal spending remained flat during Coolidge's administration, allowing one-fourth of the federal debt to be retired, state and local governments saw considerable growth, surpassing the federal budget in 1927.

Simply put, he argued that tax revenues are the product of the tax base times the tax rates. Initial tax reductions stimulate the tax base over time. While the initial result may be a short-term fall in tax revenues, the growth in the tax base will quickly cause a rise in tax revenues and will gradually reduce budgetary deficits. This behavior is one of several resembling a J shape. This will have a parallel effect of reducing the unemployment rate which tax increases do not seem to bring about as history is replete with supporting evidence. This was the case under Truman, Kennedy, Reagan, and Bush II (GW Bush; 43), all facing problems of falling economic growth and rising unemployment.

Truman Tax Cuts…sort of: Revenue Act of 1948

en.wikipedia.org/wiki/Revenue_Act_of_1948

The United States Revenue Act of 1948 reduced individual income tax rates 5-13 percent, increased the personal exemption amount from $500 to $600, permitted married couples to split their incomes for tax purposes, made the distinction between community property jurisdictions and non-community property jurisdictions less relevant in the administration of the income, estate, and gift taxes, and provided additional exemption for taxpayers age 65 and older. The Revenue Act of 1948 was vetoed by President Harry S. Truman, but his veto was overridden on April 2, 1948, by a two-thirds vote of each House of the Republican-controlled Eightieth Congress of the United States.

Kennedy Tax Cut 1962

en.wikipedia.org/wiki/Revenue_Act_of_1962

The United States Revenue Act of 1962 established a 7% investment tax credit and required information reporting to the government for interest and dividend payments

Reagan Tax Cuts…again, keep in mind that it's Congress that passes legislation

en.wikipedia.org/wiki/Economic_Recovery_Tax_Act_of_1981

The Office of Tax Analysis of the United States Department of the Treasury summarized the tax changes as follows[2]:

- phased-in 23% cut in individual tax rates over 3 years; top rate dropped from 70% to 50%

- accelerated depreciation deductions; replaced depreciation system with ACRS

- indexed individual income tax parameters (beginning in 1985)

- created 10% exclusion on income for two-earner married couples ($3,000 cap)

- phased-in increase in estate tax exemption from $175,625 to $600,000 in 1987

- reduced windfall profit taxes

- allowed all working taxpayers to establish IRAs

- expanded provisions for employee stock ownership plans (ESOPs)

- replaced $200 interest exclusion with 15% net interest exclusion ($900 cap) (begin in 1985)

Bush Tax Cut 2001 Economic Growth and Tax Reduction Act

en.wikipedia.org/wiki/Economic

Income tax

- EGTRRA generally reduced the rates of individual income taxes:

- a new 10% bracket was created for single filers with taxable income up to $6,000, joint filers up to $12,000, and heads of households up to $10,000.

- the 15% bracket's lower threshold was indexed to the new 10% bracket

- the 28% bracket would be lowered to 25% by 2006.

- the 31% bracket would be lowered to 28% by 2006

- the 36% bracket would be lowered to 33% by 2006

- the 39.6% bracket would be lowered to 35% by 2006

The EGTRRA (Economic Growth and Tax Reduction Act) in many cases lowered the taxes on married couples filing jointly by increasing the standard deduction for joint filers to between 174% and 200% of the deduction for single filers.

Additionally, EGTRRA increased the per-child tax credit and the amount eligible for credit spent on dependent child care, phased out limits on itemized deductions and personal exemptions for higher income taxpayers, and increased the exemption for the Alternative Minimum Tax, and created a new depreciation deduction for qualified property owners.

Capital gains tax

The capital gains tax on qualified gains of property or stock held for five years was reduced from 10% to 8% for those in the 15% income tax bracket.

In the last of this series to be posted on this website in the near future, the effects of massive government intervention and the growth of regulations will be examined as well as the conflict of income redistribution policies with policies to reduce the unemployment rate and restore a reasonable rate of real economic growth.