2013 Volume Issue 3

March 20, 2013

For a downloadable version, click the following:

…a bit more compressed version of the PDF

UPDATE from FOMC Meeting March 19-20, 2013

no change in from January meeting

FYI — release from March 19-20 FOMC Meeting

…the [Federal Open Market] Committee [FOMC] decided to continue purchasing additional agency mortgage-backed securities at a pace of $40 billion per month and longer-term Treasury securities at a pace of $45 billion per month.

In particular, the Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that this exceptionally low range for the federal funds rate will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee's 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored. In determining how long to maintain a highly accommodative stance of monetary policy, the Committee will also consider other information, including additional measures of labor market conditions...

The Federal Open Market Committee (FOMC) Rolls Along

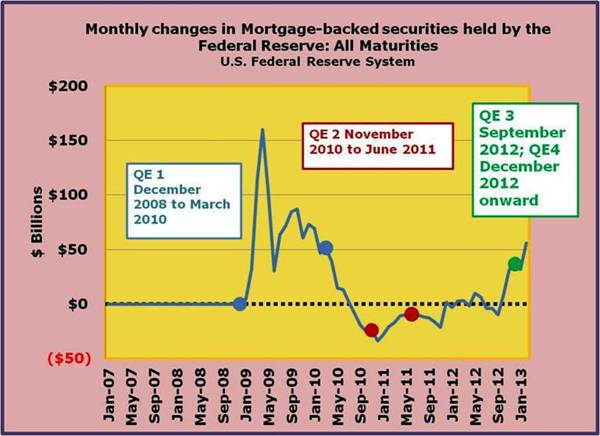

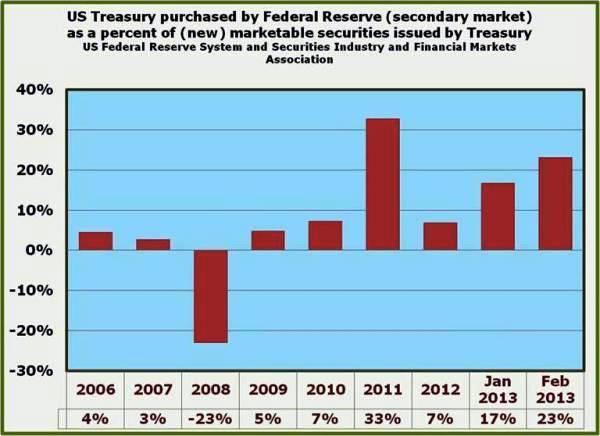

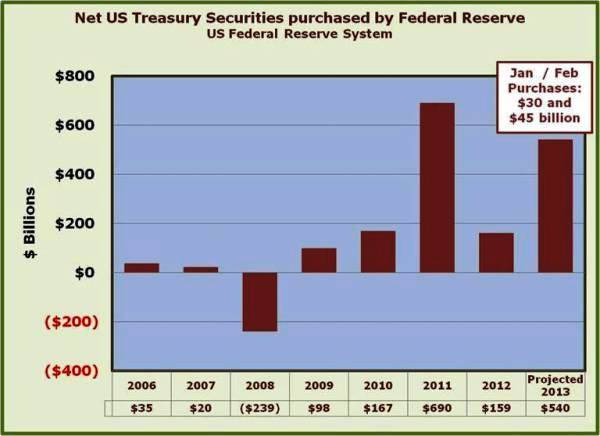

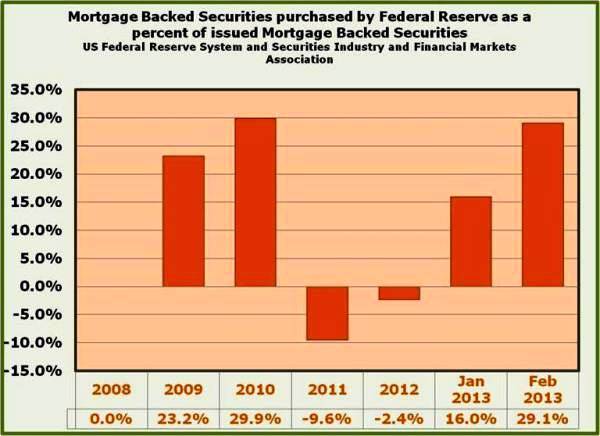

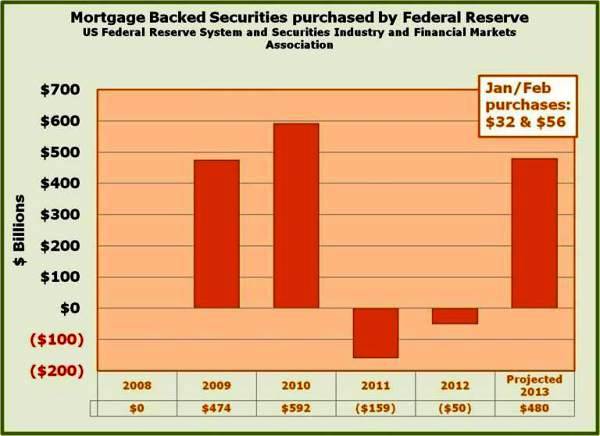

The minutes of their January meeting of the Federal Open Market Committee (FOMC), the monetary policy decision making committee of the Federal Reserve System (FED), the central bank of the U.S., were recently released. It appears that the FED will recommence as the dominant buyer of U.S. Treasury securities and mortgage-backed securities (MBS). Their current targets, at least until the next meeting of the FOMC (they meet every six weeks) on March 19-20, are $45 billion and $40 billion per month, respectively. This is a substantial percentage of the increases in the two types of debt securities as shown below; So much for the enthralled media bolstering the idea that a recovery is occurring in the U.S.

Minutes of the Federal Open Market Committee

January 29—30, 2013

www.federalreserve.gov/monetarypolicy/files/fomcminutes20130130.pdf

(pp. 14-15)

"Consistent with its statutory mandate, the Federal Open Market Committee seeks monetary and financial conditions that will foster maximum employment and price stability In particular, the Committee seeks conditions in reserve markets consistent with federal funds trading in a range from 0 to ¼ percent. The Committee directs the Desk to undertake open market operations as necessary to maintain such conditions. The Desk is directed to continue purchasing longer-term Treasury securities at a pace of about $45 billion per month and to continue purchasing agency mortgage-backed securities at a pace of about $40 billion per month."

The short respite from quantitative easing in 2012 has ended and the realism of the economic malaise of the developed world including the U.S. is once again being realized by our monetary policy makers.

In our January 2006 Newsletter article, we warned of the FED's growing fear of asset bubbles: especially regarding the impending housing collapse and the danger of rising oil prices...

Killing Fields: Weak Links in Otherwise Strong Economy (January 6, 2006)

Predicting Financial Collapse January 2006

RISING MORTGAGE INTEREST RATES

"In addition to the rising energy costs and insecurity in the labor markets, households are now facing an additional burden of rising interest rates, affecting their mortgages. As short-term rates are driven up by the Federal Reserve actions in the Federal Funds rates, it influences other short-term interest rates to rise as well.

In the area of variable rate mortgages (ARMs), the Fed's actions are gradually triggering the adjustment clauses in these mortgages. This increases the monthly payments, reducing further the disposable income available to purchase other goods and services and also reduces the cushion protecting homeowners from defaulting on mortgages."

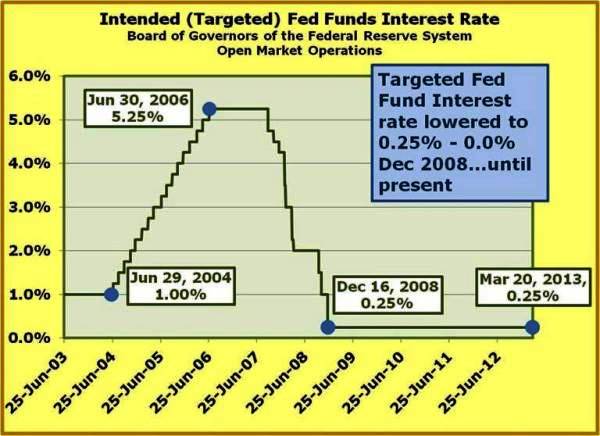

In June 2004, the FED began to move toward a policy of monetary restraint. In the meantime, our beloved investment bankers had struck a gold mine in structured debt obligations (CDOs) such as mortgage backed securities (MBSs). Commissions and fees rolled in and it elevated them above the ranks of the more modest and risk-averse, consuming most all who opposed them.

WHAT PRICE BAILOUTS? WHAT PRICE THE ELIMINATION OF THE GLASS-STEAGALL RESTRAINTS AND THE continuance of the 'TOO BIG TO FAIL DOCTRINE'?

September 30, 2011

www.econnewslettersep302011.com/

Should Bank of America and the rest have avoided the lure of investment banking?

(Investment) Bank of America?

May 22, 2006

www.businessweek.com/magazine/content/06_21/b3985081.htm

BofA aims to build its way up to the top tier of investment banks. It won't be easy

"After all, it earned $16.9 billion last year, 85% of that in commercial and retail operations, where it's a force unequaled."

…

"BofA CEO Kenneth D. Lewis is convinced that bigger growth opportunities are in investment banking, especially stock underwriting, initial public offerings, and mergers-and-acquisitions advice."

Rating agencies also succumbed to the unspoken pressures to make these derivative securities palatable in terms of risk to the investors. Investors, often governments and pension funds let due diligence become virtually comatose and the stealthy villain of finance called greed overwhelmed them. George Bush was made the scapegoat. The financial crisis of 2008 was born and is still with us five years later.

It became increasingly clear at the time that TEASER RATE MORTGAGES, not to be confused with true adjustable rate mortgages, were becoming a large part of new mortgages being issued. Initial low mortgage rates resulted in relatively low monthly payments that would qualify otherwise unqualified buyers of residential housing. In a couple of years the mortgage contracts called for mandatory increases, often substantial, on the interest rates on those teaser rate mortgages. Of course delinquencies on these mortgages skyrocketed and the overrated derivative securities such as MBSs started to collapse in market value.

As we pointed out back in 2006, when the FED began to shift to a policy of constraint a bit earlier (June 2004), the true adjustable rate mortgages (ARMs), being tied to observable and thought to be free from manipulation short term market interest rates, such as the one year Eurodollar rate, the Libor, Cost of Funds Index, etc., began to rise sharply as did the monthly mortgage payments.

Libor Scandal

London Interbank Offered Rate

en.wikipedia.org/wiki/Libor_scandal

The original idea of the ARMs was to make them inflation proof in terms of real yields and market price. Unfortunately, the FED can cause significant upward pressure on interest rates by launching into a policy of monetary restraint….in June 2006 they did just that.

But it goes beyond the rising delinquencies on Teaser rate mortgages and true ARMs. The inverse relationship between asset prices and interest rates is always present and kicked in. Debt claims such as bonds and other assets to varying degrees, felt the brunt of rising interest rates. Asset bubbles, like balloons at a New Year's Party in a hailstorm, began to burst as the market prices fell from bonds and mortgages to stock and real estate. The rest is history.

For those who are not familiar with the effects of such purchases, a review of their place in the history of the Federal Reserve System's (FED) monetary policy actions and of how these monetary policies impact the creation of money and credit will prove helpful in assessing the FED'S ongoing policy actions. There is a lot of misinformation out there that is confusing the public, and a lot of it is coming from the so-called experts, especially in the media.

A Brief History of the FED's Monetary Policy Structure and Tools of Intervention to Control the Growth of Money and Credit

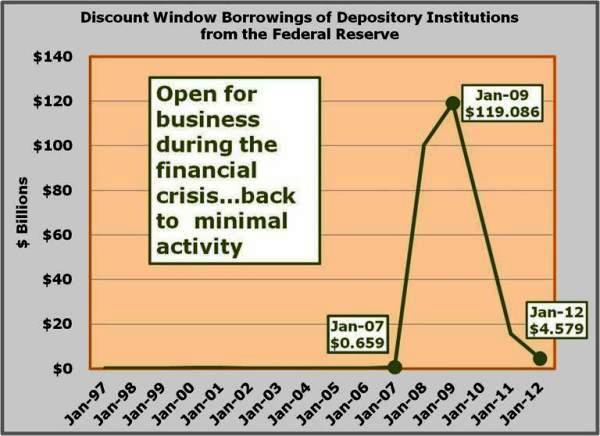

When the FED began to operate after the passage of the Federal Reserve Act in 1913 en.wikipedia.org/wiki/Federal_Reserve_Act, its quantitative tools to execute monetary policies were changes in the Discount Rate, changes in Legal Reserve Requirements, and Open Market Operations. The most used tool back then was the Discount Rate and its control of the Discount Window facility.

The Discount Window is a facility through which depository institutions can discount or sell eligible notes receivable, which were a result of their making loans or creating credit.

www.federalreserve.gov/monetarypolicy/discountrate.htm

"The discount rate is the interest rate charged to commercial banks and other depository institutions on loans they receive from their regional Federal Reserve Bank's lending facilitythe discount window. The Federal Reserve Banks offer three discount window programs to depository institutions: primary credit, secondary credit, and seasonal credit, each with its own interest rate. All discount window loans are fully secured."

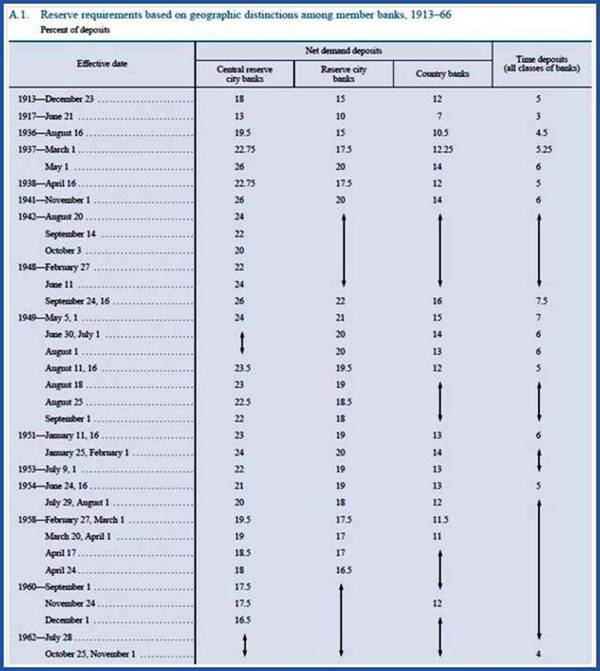

Changes in legal reserve ratios were its second most used quantitative tool. Due to the lack of depth in the financial markets back then, Open Market Operations were but a minor tool in the tool box of the FED as it sought to execute its' policy decisions. Substantial growth in the financial markets, especially the U.S. Government marketable securities segment, would occur as the federal deficit ballooned due to the Great Depression and the Second World War.

Reserve Requirements

www.federalreserve.gov/monetarypolicy/reservereq.htm

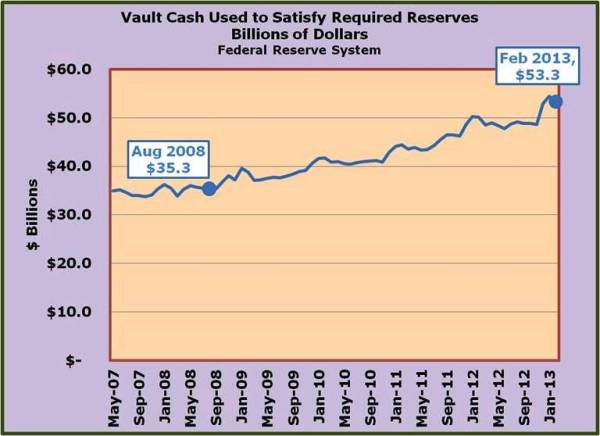

"Reserve requirements are the amount of funds that a depository institution must hold in reserve against specified deposit liabilities. Within limits specified by law, the Board of Governors has sole authority over changes in reserve requirements. Depository institutions must hold reserves in the form of vault cash or deposits with Federal Reserve Banks.

The dollar amount of a depository institution's reserve requirement is determined by applying the reserve ratios specified in the Federal Reserve Board's Regulation D to an institution's reservable liabilities (see table of reserve requirements). Reservable liabilities consist of net transaction accounts, nonpersonal time deposits, and eurocurrency liabilities. Since December 27, 1990, nonpersonal time deposits and eurocurrency liabilities have had a reserve ratio of zero."

Reliance on the Discount Window and the Discount Window facility gradually decreased over the years as did the use of changes in the Legal Reserve Ratios. The role of Open Market Operations gradually became the work horse of the quantitative tools of the FED in carrying out its' policy decisions both in what often were called its 'defensive and dynamic' policies.

Open Market Operations

www.federalreserve.gov/monetarypolicy/openmarket.htm

"Open market operations (OMOs)the purchase and sale of securities in the open market by a central bankare a key tool used by the Federal Reserve in the implementation of monetary policy. The short-term objective for open market operations is specified by the Federal Open Market Committee (FOMC). Historically, the Federal Reserve has used OMOs to adjust the supply of reserve balances so as to keep the federal funds ratethe interest rate at which depository institutions lend reserve balances to other depository institutions overnightaround the target established by the FOMC."

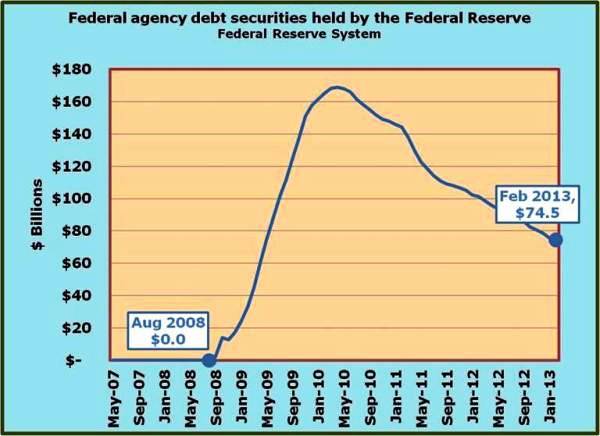

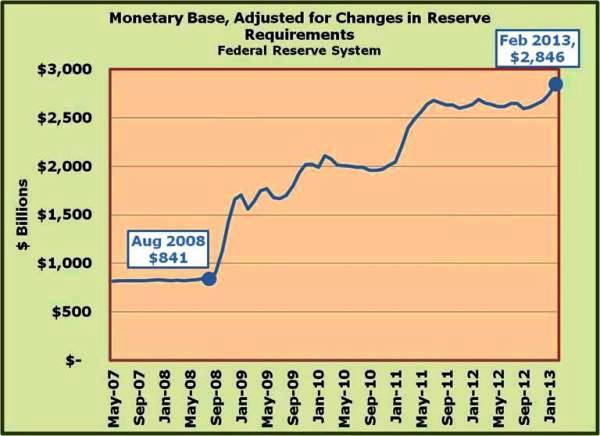

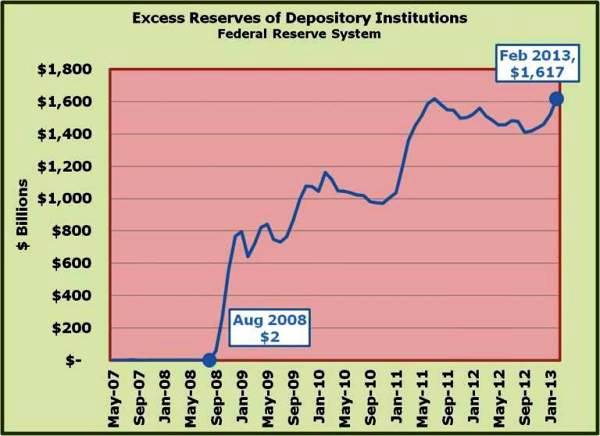

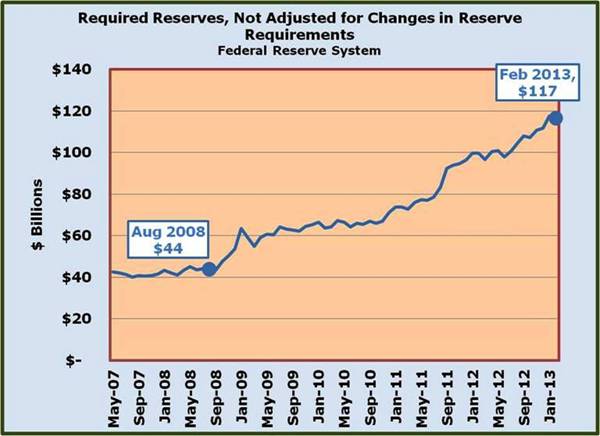

The financial crisis of 2008 resuscitated the Discount Window facility for a short time, but it seems to have quickly returned to a more quiescent state. Changes in the Legal Reserve ratios continued hibernating as a quantitative tool to effectuate monetary policy. As a result of that financial crisis, the Open Market Operations have grown to gargantuan proportions in the last few years and have been extended to private sector securities as the above illustrations clearly show.

If, and do not hold your breath waiting for a real economic recovery to occur, but if it should come, the enormous increase in the monetary base and excess legal reserves of depository institutions that has occurred, will have to be reversed.

The monetary base is the sum of the legal reserves of depository institutions and the currency in circulation outside of the depository system. Legal reserves consist in the reserve deposits of the depositories at the FED and much of the depositories' vault cash.

The enormous increase in the monetary base and excess reserves is a result of the several year buying binge of assets by the FED and resulting large excess of legal reserves will have to be quickly reduced to a more normal size in order to eliminate the greatly enlarged capacity of depository institutions for money and create creation that could fuel significant inflation when a real recovery occurs.

The reduction of the excess reserves can be achieved by either selling assets that have not yet reached their maturity or by raising the legal reserve ratios that would convert the excess reserves into required reserves.

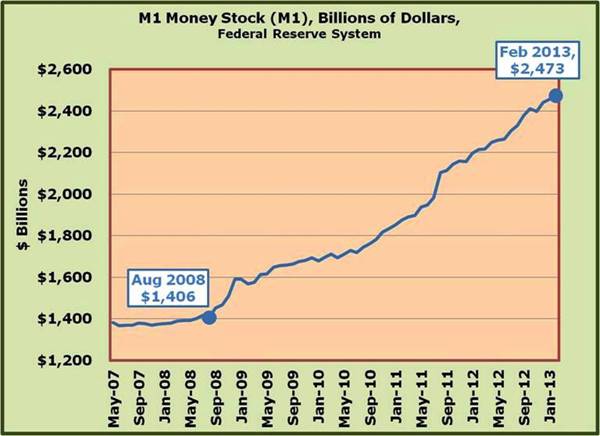

When the FED buys any asset(s) such as Treasury securities, Federal Agency securities, or mortgage backed securities, the seller receives payment from the FED with electronic funds transfers to the seller's checkable deposit Accounts at a depository institution, more often than not, a commercial bank. At the same time, the depository's reserve deposit account at the FED has increased by the same amount. While M-1, in the form of a checkable deposit account, is increased by the amount of the proceeds of the sale, the monetary base also increases by that amount. Unless a cash withdrawal occurs, the excess reserves rise by 90% of the proceeds, the other 10% would be the increase in required reserves for the checkable deposit increase from the sale by the original holder of the securities in question.

While additional transactions may shift some of the legal reserves to other depositories, the depository system as a whole has additional capacity to create additional checkable deposit money and credit. Again assuming no resulting currency drain, each dollar of excess reserves enables the depository institution system to create additional checkable deposit money and credit of 10. This multiple assumes a legal reserve ratio of 10 percent and is determined by dividing 1.0 by 0.10 or ten percent: this is called a multiplier.

Of course there will be at least some currency drain which reduces the excess reserves as it begins to circulate in public. In this way, some of the very expansive effects of the FED's purchase of securities are lessened. One dollar of additional currency in circulation absorbs the M-1 checkable deposit form of M-1 and credit creating capacity of the monetary base on a 1 to 1 basis. Remember that the monetary base consists of the legal reserves of depository institutions and the currency in circulation among the public. With a constant monetary base, an increase of one dollar in currency in circulation causes the legal reserves of depository institutions to decrease by one dollar. The legal reserves of depository institutions consist of reserve deposits at the FED and much of the depositories' vault cash. Also remember that M-1 consists of the checkable deposits of the public at depository institutions and the currency in circulation among the public.

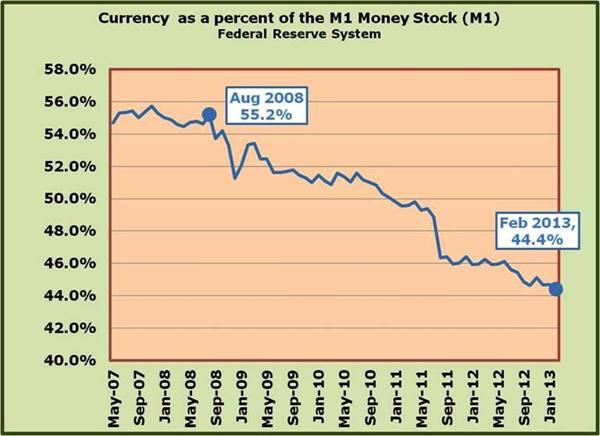

A very large percentage of the currency in circulation is held outside the U.S. by foreign interests. They have more trust in the strength of the U.S. Dollar than in their own nations' currency. Given currency devaluations over the last century and the very recent events in Cyprus, is there any wonder why?

The currency drain is a powerful reducer of the expansive effects of an increasing monetary base in terms of money and credit creation.

If we fast-forwarding in this article to the relationship of the currency in circulation as a percent of M-1 money, we can see that the currency drain is nearly 45% of total M-1 money (currency in circulation plus checkable deposits). Without getting into more complex calculations, this reduces the M-1 multiplier (M-1 monetary base) to approximately 7. As the ratio of currency in circulation to the M-1 the money stock changes, the size of this multiplier changes. The additional amount of M-1 money and credit for each dollar of excess reserves that can be created also varies inversely to the relative size of the currency drain.

As the legal reserve ratios are increased, the M-1 multiplier decreases causing increases in the monetary base to be less expansive in terms of M-1 money and credit creation. In effect, some excess legal reserves become required reserves for any given amount of checkable deposits of the depository institution system.

There is a precedent of monetary policy actions for something similar to the current situation of enormous excess reserves and the FED's need to do something should a recovery occur. It occurred after the Second World War when FED's support for financing the war effort left the economy with an excessively large monetary base. Price controls were relied upon to constrain inflationary pressures. President Truman convinced Congress to eliminate the price controls. The FED responded by raising legal reserve ratios to eliminate the enlarged capacity of commercial banks (the only depository institution creating checkable deposits at that time) to create money and credit that would fuel the inflation. A repeat of such a policy action could ensue when a recovery really does take hold. Selling massive amounts of MBS and U.S. Government marketable securities to reduce the monetary base and excess legal reserves would cause a great deal of price and interest rate instability in those markets.

Reserve Requirements: History, Current Practice, and Potential Reform; the Accord between the Treasury and the FED

www.federalreserve.gov/monetarypolicy/0693lead.pdf

In 1951, the Federal Reserve resumed an active, independent monetary policy. In subsequent years, reserve requirements were adjusted numerous times, usually to reinforce or supplement the effects of open market operations and discount policy on overall monetary and credit conditions. In the short run, however, reserve requirements placed little constraint on the expansion of deposits because the Federal Reserve largely accommodated any such expansion through open market operations. Over time, though, if the Federal Reserve sought to reduce the availability of money and credit by providing reserves less generously through open market operations, it could and often did augment its actions by raising reserve requirements.

Because a rise in the legal reserve ratios is a much blunter tool, the current fragile condition of the financial markets throughout much of the world seems to favor changing 'Legal Reserve Ratios' over 'Open Market Operations' sales of assets, should a real recovery occur. But the last few financial crises have shown our own central bank to favor the open market operations approach resulting in much market instability. Never forget the inverse relationship between interest rates and asset prices and the huge periodic materializing of what used to be a fairly docile interest rate risk.

Federal Reserve System — Reserve Requirements

The current Legal Reserve ratio is approximately 10% for the depository system now consisting of not only commercial banks but the savings banks, credit unions and what is left of the savings and loan associations. The latter three types of depositories were formerly called the thrift institutions but were given the authority to create checkable deposits. Recall that the M-1 measure of money consists of checkable deposits along with currency (overwhelmingly Federal Reserve Notes, the paper money, and coins issued by the Treasury). The checkable deposit form of M-1 money (demand deposits and other checkable deposits consisting of NOW accounts, Share drafts of credit unions and ATS accounts) facilitate around 90% of the legitimate or above ground economy's transactions. The transactions of the illegitimate or underground economy are overwhelmingly facilitated by the currency portion of M-1 money.

From the NY Fed

As of December 2007, currency in circulation—that is, U.S. coins and paper currency in the hands of the public—totaled about $829 billion dollars. The amount of cash in circulation has risen rapidly in recent decades and much of the increase has been caused by demand from abroad. The Federal Reserve estimates that the majority of the cash in circulation today is outside the United States."

By some estimates, up to two-thirds of the currency in circulation is outside of the U.S.

Given the current approximate legal reserve ratio of 10% and ignoring the effects of the currency drain, one dollar of legal reserves will support at a maximum, ten dollars of checkable deposit money (currently nearly 55% of the M-1 measure of money or money as the medium of exchange). That means that one dollar of excess legal reserves can result in a maximum of ten dollars of the checkable deposit form of M-1 money. Hence the current huge volume of excess legal reserves of depository institutions could result in a huge increase in the checkable deposit form of M-1 money. The printing presses are NOT needed for the creation of the checkable deposit form of M-1 money as is heard from the media and others. Most of the expansion of M-1 money is from depository institution loan officers creating credit by giving the borrowers an increase in their checkable deposits and NOT, REPEAT NOT involving running the printing presses!!!!!!! Around the Civil War, nearly 150 years ago you could bring printing presses into the matter, but nowadays it is the checkable deposit form of M-1 money and that does not involve printing presses at the Treasury's Bureau of Engraving (or the Mint for coins).

The closest involvement of printing presses is the printing of the new blank checks for depositors and even that linkage is being eliminated by debit cards, the retail version of electronic funds transfers or EFTs.

The Money Supply and those (supposedly) Overworked Printing Presses

January 14, 2011

www.econnewsletterjan142011.com/

If you ask why the large increase in legal reserves has not resulted in large increases credit and in the checkable deposit form of M-1 money, it is because of two reasons. The first is that until the economy really recovers, loans are very risky both to individuals and to business. This reduces and often eliminates their profitability. The second reason is that the supervision and regulation departments of the FED, the FDIC and the Controller of the Currency have been acting like wounded grizzly bears threatening depositories with draconian punishment should they make loans that turn bad. It has been especially hard for small business to obtain credit and small depositories have been frequently closed or a victim of forced mergers, etc. While the FED expands the capacity of depositories to create additional credit and M-1 money (checkable deposit form of M-1 money), the risk levels are still too high and the sup(ervision) and reg(ulation) girls and boys are causing the expanded capacity of depositories to create money and credit to be unused resulting the large amount of excess legal reserves of the depository system. This is not a unique situation but occurs whenever a significant economic or financial crisis occurs.

A few random but relevant and related issues

Why has the stock market held up so well recently? First of all, interest rates on debt securities have been kept low, driven by the FED's quantitative easing initiatives. This gives stock an edge in terms of dividend yields. Secondly, when the bankruptcy judge ruled that the ownership of General Motors should go to the government and the labor unions, this effectively threw the bondholders under the bus, so to speak. If that stupidity becomes a precedent in future bankruptcy hearings, the required rate of return on debt capital will rise. Since the FED has put a lid on interest rates, it has helped shift investors toward equity from debt. In the not too distant future, if a reasonably strong recovery does not occur, the stock market may be in for a shock in the form of a downside correction. Time will tell. Keep tuned in to this newsletter.