2015 Volume Issue 11

September 11, 2015

For a downloadable version, click the following:

…a bit more compressed version of the PDF

What should/will the FED* do on the monetary policy front?

*FED, as in Federal Reserve System – Federal Open Market Committee, in particular Punishment fitting the crime – or Monetary Policy Actions

Just as Gilbert and Sullivan in their light opera, ‘The Mikado’ exhorted us to be sure that the punishment fit the crime; even more so, we exhort policymakers at the FED to be sure that the policy undertaken fits the given problem requiring a solution.

The FED’s role in Popping Speculative Bubbles or Errant Monetary Policy

Many post-mortems concerning the causes and lengthiness of the Great Depression have helped fill the literary journals concerned with economics and business. Many conclude that the continuance if not the cause of the Great Depression, was in significant part due to errant Federal Reserve System’s policies. Speculative bubbles have long been the concern of monetary and fiscal policy makers. Is it a speculative bubble or is it the beginning of a long-term trend due to changes in basic forces in that particular market?

In the case of the Great Depression, the sudden surges in stock market prices jangled the nerves of policy makers on more than one occasion. Instead of adjusting margin requirements on stock purchases, the FED, not yet empowered to use that strategy until the adoption of Regulation T, and followed by Regulation U pursuant to the Securities Exchange Act of 1934, usually sought to make all credit more costly by using discount rate changes (which were much more important at that time than open market operations which was just coming into vogue and would later dominate the execution of FED monetary policies) or by restrictive open market operations that put upward pressure on all interest rates by reducing the capacity of the banking system to create money and credit.

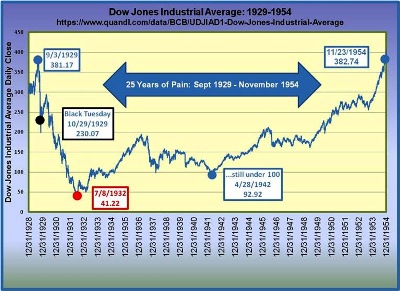

Some background on the lead up to Black Tuesday, October 29, 1929

It appears from evidence gleaned from margin requirements on stock purchases may have played less of a role leading up to the Black Tuesday (October 29, 1929) crash than has been portrayed. According to Gene Smiley and Richard Keehn in their paper, Margin Purchases, Brokers’ Loans and the Bull Market of the Twenties (http://www.thebhc.org/sites/default/files/beh/BEHprint/v017/p0129-p0142.pdf), the literature and hearings involving the Securities Act of 1933, the Banking Act of and Exchange 1933 and the Securities and Exchange Act of 1934 centered heavily on the margin requirements relating to the acquisition of securities.

The first charge was that the brokers made no effort to examine the creditworthiness of their clients, leading to speculation by individuals who did not have the skill and financial resources to do so.

That sounds similar to the criticisms leveled at the credit rating agencies leading up to the latest crisis in 2008…

ARE THEY THE ARTISTS AND SCIENTISTS OF HYPOCRISY PAR EXCELLENCE: Our beloved rating agencies, bless them all; or have they learned their lesson?

August 11, 2011

A major factor in the collapse of mortgage backed securities (MBSs), [or] the first phase of the financial and economic collapse in which we are currently mired, was the overrating of the MBSs by the rating agencies.

…back to Smiley and Keehn

Second, the Report charged that the though the number of margin customers was not large, this small number of margin customers created instability in the financial markets.

Reference to ‘Report” is from the June 1934 report of the Committee on Banking and Currency on Stock Exchange Practices. (The “Report” included citations on papers from Irving Fisher and Francis Hirst from 1930-1931 pointing to margin issues running up to the Crash – October 29, 1929)

Third, the Report criticized high levels of brokers’ loans found in 1928 and 1929…strained beyond the point of safety.

Smiley and Keehn:

There seems to be general agreement that margin requirements were rising from either late 1928 or early 1929, through September 1929.note: In a letter from the Journal of Commerce, October 1928

It is necessary that conditions influencing security market movements are such at the present time that a higher degree of protection on accounts is necessary…Therefore, our requirements will be as follows: Securities selling below $10, cash only; from $10 - $20, 50 per cent; $20 to $30, 10 points; above $30, 30 per cent of purchase price…No margin accounts will be opened on an initial deposit less than $1,000.

Irving Fisher noted that in 1929 margin requirements were higher than ever before in the history of Wall Street. George Soule reported that a few months prior to the crash the brokerage houses raised their requirements to 50 percent.

Since the margin requirements were not low from a historical point of view, Smiley and Keehn turned to the broker lending issue. According to Benjamin H. Beckhart (1931), in the 1927-1929 timeframe, broker lending had to do with corporations:

Instead of investing in securities or in the enlargement of plant equipment, the owners loaned them to brokers where they probably realized a higher return than if utilized in savings.

This sounds eerily similar to the chasing of yields running up to the collapse in the financial markets in 2007-2009, where bundled asset backed securities included ‘teaser rate mortgages’ and other adjustable rate mortgages brought us the BNP Paribas fiasco and the rest.

Excessive Subprime Lending; or Misguided Monetary Policy – A Reasoned Critique

August 2007

The Meltdown

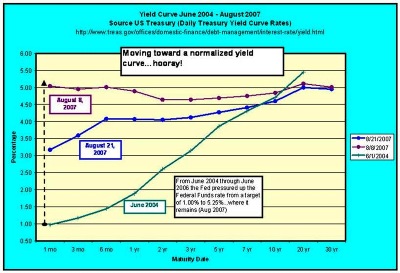

This view of Fed policy of constraint resulting in rising short-term rates abruptly changed when the largest French bank, BNP Paribas announced that it was unable to estimate the value of mortgage related asset backed securities of its investment companies. The Fed reacted very quickly, supplying funds to the financial markets through repurchase agreements, cutting the effective Federal Funds rate from an elevated 5.41% on August 9 to 4.54% on August 14, 2007. On August 15, Countrywide Mortgage, the largest U.S. mortgage lender, recently purchased by private equity firm KKR, followed BNP Paribas’ lead, announcing that they had similar problems in valuing their assets. As of Thursday afternoon, August 16, 2007, not only had the effective Federal Funds rate fallen, but the 10-year U.S. Treasury constant maturity bond had also fallen to 4.66, or 7 basis points below what it was when the Fed began its credit crunch in 2004.

In summary, Smiley and Keehn concluded that:

The perception that margin requirements were extremely low during the twenties, and particularly in 1928 and 1929, has been shown to be wrong. We argue that brokers’ loans played a facilitating role, but not an initiating role, in the boom and the crash.

The Securities Exchange Act of 1934

Federal Reserve Bank of San Francisco

March 2000

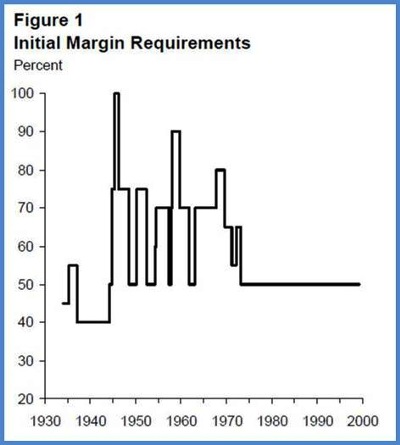

The Securities Exchange Act of 1934 mandated federal regulation of purchasing securities on margin… Federal Reserve Regulations T and U govern the extension of credit by broker-dealers, banks, and other lenders to customers for the initial purchase of certain securities, including common stocks. The initial margin requirement represents the minimum amount of funds that investors must put up to purchase stocks on credit…Since 1934, the Federal Reserve has changed the initial margin requirements in stocks 23 times (see Figure 1). The current rate, set in 1974, is 50%.

Using a Pin prick rather than a Hammer to Pop a Bubble

With the thought of tackling bubbles directly and raising margin requirements of stock purchases, why wouldn’t the FED consider such policy prescriptions? Surely the FED officials are not more concerned with the profitability of investment banking firms than with the economy as a whole! Such an error in judgment by the FED has been on display in recent times; consider what occurred in the Greenspan era when the Chairman of the Federal Reserve Board of Governors encouraged the FOMC to opt for raising all interest rates and not using margin requirement changes on stock purchases. The lack of arm’s length behavior in this regard when stock market bubbles occur is a continuing problem.

MISSION ACCOMPLISHED; REDUCE HOUSEHOLD NET WORTH PRIMARILY THROUGH COLLAPSING REAL ESTATE VALUES BY $7 TRILLION, THUS NEUTRALIZING THE WEALTH EFFECT AND ENDING IRRATIONAL EXUBERANCE

June 8, 2011

In Greenspan’s own words,Our forecasts and hence policy are becoming increasingly driven by asset price changes. The steep rise in the ratio of household net worth to disposable income in the mid-1990s, after a half-century of stability, is a case in point. Although the ratio fell with the collapse of equity prices in 2000, it has rebounded noticeably over the past couple of years, reflecting the rise in the prices of equities and houses.Remarks by Chairman Alan Greenspan Reflections on central banking At a symposium sponsored by the Federal Reserve Bank of Kansas City, Jackson Hole, Wyoming

August 26, 2005

Excessive Subprime Lending; or Misguided Monetary Policy – A Reasoned CritiqueAugust 2007

CURRENT U.S. MONETARY POLICY ON THE VERGE OF CHAOS… A FINANCIAL CHERNOBYL IN THE MAKING

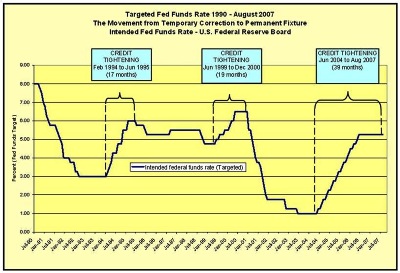

In June 2004 the Fed, fearing a return of inflation caused by rising oil prices, as was experienced in the 1970s, began a policy of constraint which drove the federal funds rate from 1.00% to its current targeted rate of 5.25%. What it was not able to do (fortunately) was to drive the intermediate and longer-term rates significantly higher. This led to a flattening, and at times, an inversion of the yield curve – where short term rates were equal to or higher than long term rates. This was the cause of former Fed Chairman, Alan Greenspan’s “conundrum”. What the Fed was able to do (unfortunately) was to cause the resetting of variable rate mortgages as they passed through their short fixed rate term – usually two or three years.

The FED operating at Arms’ Length from Wall Street – moving toward Open Market Operations

In many types of problems, the FED has shown its ability to operate at arms’ length in relation to the individual firms such as member commercial banks. When the debt markets expanded and matured as the amount of U.S. government debt securities (Treasury bills, notes and bonds) grew enormously with the ballooning U.S. government debt due to the Great Depression and WWII), the FED moved to emphasize open market operations relative to the Discount Window and Discount Rate Mechanism. Instead of judging each individual member bank to see if they would be eligible to borrow at the Discount Window, they simply expanded the capacity of the system to create money and credit if a stimulus stance was desired or contract the capacity of the commercial banking system to create money and credit if a policy of restraint was called for. Individual institutions were free to go the Fed Funds and other short-term markets to adjust their individual positons. This created the arms’ length distance needed for the FED in dealing with banks and avoided the need to micromanage the institutions which they regulated, and it also avoided the appearance of favoritism. This approach was more typical of the FED’s overall approach to carrying out its policy decisions.

In addressing specific asset bubbles, changes in margin requirements instead of expanding and contracting the overall capacity of the system to create money and credit would avoid the charge that the FED’s actions [restrictive monetary policy actions] were a basic cause of a number of economic downturns.

As we have argued before on this website, investment banking firms (the broker, dealer, and underwriting firms) should not be part of holding companies, especially when commercial banking operations are a sister subsidiary. Instead, as the financial crisis of 2007-2009 was occurring, such inclusions of investment banking firms with commercial banking firms in the same holding company increasingly became the rule and not the exception. The next time a financial crisis begins to occur; and yes, it is a question of when and not if, the financial system is ripe for an even greater crisis as a result of these ill-conceived policies.

By the way, not unlike the FED’s use of open-market operations in a restrictive monetary policy setting, the punishment prescribed by Mikado (Emperor of Japan) always seemed to lean toward execution, no matter the crime…