2016 Volume Issue 3

Economic Newsletter for the New Millennium

For a downloadable version, click the following:

February 16, 2016

…a bit more compressed version of the PDF

THE TRIALS AND TRIBULATIONS OF OUR CENTRAL BANK (FEDERAL RESERVE SYSTEM OR FED) IN DETERMINING AND EXECUTING MONETARY POLICY

The Lack of Symmetry in the Effectiveness of Monetary Policy

In several past issues of this newsletter over the thirteen years of its existence, we have examined the lack of symmetry in the FED’s (Federal Reserve System) ability to alter the macroeconomic behavior of the economy. It has awesome power to slow the economy down but it is very weak in its ability to stimulate it to a faster recovery. The last several years have been another example of this asymmetry. The FED’s chief tool of simulation for many years standing is the open market operation. In its attempt to help the economy recovery from the financial crisis of 2008-09, it pursued several rounds of Quantitat9ve Easing. It expanded its portfolio many fold. Yet we have been stuck for several years at around a 2% annual growth rate of real GDP. Recalling the spirit of Okun’s Law (http://econnewsletter.com/229401.html), this anemic growth rate has led the U.S. to a dismal and lengthy period of sub-par growth and has failed to generate enough jobs to maintain the labor force participation rate at the level it was at the beginning of the financial crisis several years ago. As the real world changes, economic doctrines rise, fall, and sometimes rise again.

I didn’t know that! The theory of money and credit creation and its relationship to monetary policy…the many faces of money

The terms money and credit have much more complex meanings than most people think they do. This leads to much confusion and often misleads the public to a view of the current status of the economy that is often incorrect. We have seen this in respect to other concepts such as the unemployment rate or the meaning of poverty and its magnitude in our society. Former president, Harry S. Truman, recalled an old saying many years ago that should give one pause when looking at data: there are lies, damned lies, and statistics, or as some call them, ‘sadistics’.

The concept of money is not a simple one. In textbooks of a previous generation, it was described as a liquid store of value, the unit of account, the medium of exchange and the standard of deferred payment. The usefulness of the theory of monetarism depends on what definition and hence measure of money is utilized as well as the behavior of the velocity of the monetary aggregate chosen. While at the present time, our Central Bank, the Federal Reserve System or FED as we shall henceforth refer to it, currently reposts on a regular basis two measures of money, M-1 and M-2. At least one branch of the FED reports M-3 periodically. Back in the 1970s, the FED regularly measured and reported five definitions of money, M-1 through M-5. Of all of these measures, money in its role as the medium of exchange is labeled as M-1.

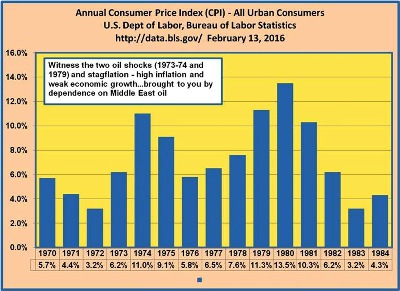

As inflation began to rock the economy in 1973 and continued to accelerate through early 1980, the FED eventually began reporting five measures of money. Each of these five measures has its’ own velocity in respect to nominal Gross Domestic Product or GDP. Velocity and its’ stability or lack thereof is a critical issue in determining whether or not the control of a monetary aggregate’s behavior in able to predictably influence the overall behavior of the economy. We will delve more deeply into this issue later in this newsletter.

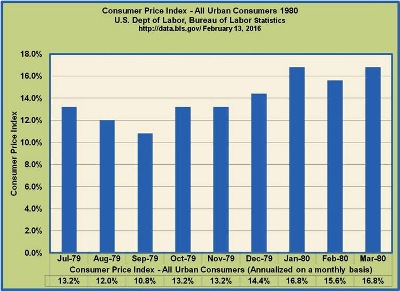

As the financial system began to change in order to cope with the accelerating inflationary burden that was occurring in the 1970s, numerous legislative changes were debated and some resulted in legislation to aid and occasionally to hinder that adaptive evolution. Recall that at its height in early 1980, the inflation rate reached was approaching 20% on an annualized basis.

The M-1 Measure of Money

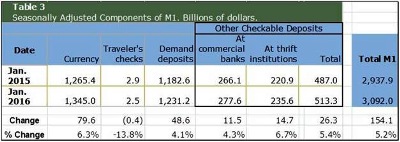

The definition of money as the medium of exchange (M-1) includes two components, checkable deposits and currency. Currency includes the paper money (now overwhelmingly consisting of Federal Reserve Notes) and coins. The paper money (Federal Reserve Notes) are the liabilities of the FED while the coins are liabilities of the U.S. Treasury. The checkable deposits are liabilities of the private sector depository institutions.

Yes, money, even M-1 (medium of exchange) money, is the debt of the issuer.

Depository Institutions Deregulation and Monetary Control Act of 1980

https://en.wikipedia.org/wiki/Depository_Institutions_Deregulation_and_Monetary_Control_Act

Prior to 1980, only the checkable deposits of commercial banks were counted as part of M-1. With the advent of savings banks being allowed to create NOW accounts for their customers, and with credit unions having share draft accounts, these so called thrift institutions (credit unions, savings banks, and savings and loan associations) to which they were usually referred, were incorporated into the term depository institutions and NOW accounts and share drafts were included as part of the checkable deposit component of M-1 along with demand deposits at commercial banks.

Money supply… https://en.wikipedia.org/wiki/Money_supply#United_States

- M1:

- The total amount of M0 (cash/coin) outside of the private banking system plus the amount of demand deposits, travelers checks and other checkable deposits

- M2:

- M1 + most savings accounts, money market accounts, retail money market mutual funds, and small denomination time deposits (certificates of deposit of under $100,000).

- M2 - time deposits + money market funds

- M3:

- M2 + all other CDs (large time deposits, institutional money market mutual fund balances), deposits of eurodollars and repurchase agreements.

- M4-: M3 + Commercial Paper

- M4:

- M4- + T-Bills (or M3 + Commercial Paper + T-Bills)

- L:

- The broadest measure of liquidity that the Federal Reserve no longer tracks. Pretty much M4 + Bankers' Acceptance

www.econnewsletterdec312003.com/

(Volume 2003: Issue 5) December 31, 2003)

(The Federal Reserve System: Sausage making and its relation to monetary policy)

Basic Understanding of Money and Credit Creation

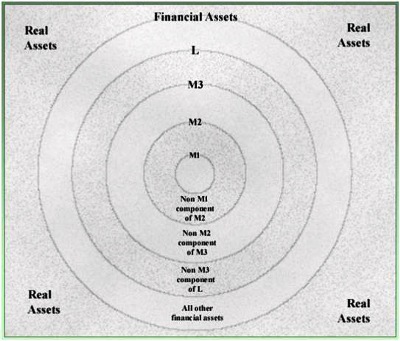

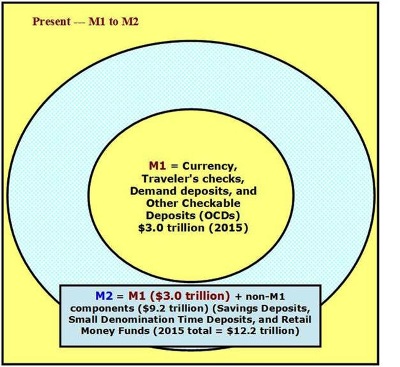

Nearly a decade ago, Prof. Byrne designed picture of how money is related to wealth. It has appeared in his text, FINANCIAL ECONOMICS, for several years. It is reproduced here for the reader. Money has two general meanings. First, its broad meaning is that money is a set of assets the store wealth in a very liquid manner. Its second meaning is that money is anything generally acceptable as a medium of exchange. These are the most liquid assets of all. In this nation, the Fed defines the two types of measure. M-1 has traditionally meant the medium of exchange. M-2, M-3, L or liquidity, M-4, M-5, M-1 a, M-1b have been some of the designations given money especially as a liquid store of value. The composition changes over time. At one time years ago, gold coins and gold certificates were included but have not for many years now.

The current designation for money as a medium of exchange is M-1. It is composed of three elements: currency, checkable deposits, and non-bank travelers’ checks. The last of the three is so small, it is often ignored. Nearly 99% of M-1 is either currency or checkable deposits. If we divide the economy into the underground economy (in pursuit of indictable activities including tax evasion) and the above ground economy or legitimate economy, which money as a medium of exchange is dominant, if radically different? While currency is roughly one-half of M-1 money and checkable deposits about two thirds, nearly 100% of the transactions in the underground or illegitimate economy is facilitated by currency while the corresponding figure in the legitimate or above ground is nearly 5%. A major part of the currency component of M-1 serves as the preferred currency in places like Cuba, Russia, etc., where local currencies evoke little faith in their ability to hold value.

Currency consists of coins and paper money, nearly all of which are Federal Reserve Bank notes. While the coins are heavy, they are swamped in dollar value by the Federal Reserve notes. Checkable deposits consist of demand deposit, negotiable orders of withdrawal (NOW accounts), share drafts at credit unions and ATS or automatic transfer accounts (zero balance checking accounts attached to a savings account. Just below is a breakdown of the components of M-1 along with those of M-2 and M-3. Until a short while ago, L or liquidity was also published but has been discontinued."

The Broader or More Inclusive Meanings of Money

Most of the broader measures were dominated by liquid assets that did not serve as the medium of exchange and as the measure of money became more inclusive, it approached a more European view of the causes of price level changes, that of the behavior of all liquid assets. Of course, to the extent that the European view is more correct than monetarism, it makes monetary policies more difficult to execute.

Monetarism; the Resurrection of the Quantity Theory

Monetarism argues that the behavior of money is the major cause of price level changes (inflation or deflation). However, most monetarists opt for a broader measure of money than M-1 as the determinant of these price level changes. Such a broader measure is M-2. It includes M-1 plus some of the savings deposits which are not checkable.

- (M-1)

- Consists of (1) currency outside the U.S. Treasury, Federal Reserve Banks, and the vaults of depository institutions; (2) travelers checks of nonbank issuers; (3) demand deposits at all commercial banks other than those due to depository institutions, the U.S. government, and foreign banks and official institutions, less cash items in the process of collection and Federal Reserve floa;t and (4) other checkable deposits (OCDs), consisting of negotiable order of withdrawal (NOW) and automatic transfer service (ATS) accounts at depository institutions, credit union share draft accounts and demand deposits at thrift institutions. Seasonally adjusted M1 is calculated by summing currency, travelers’ checks, demand deposits, and OCDs, each seasonally adjusted separately.

- (M-2)

- Consists of M1 plus savings deposits (including money market deposit accounts), small-denomination time deposits (time deposits-including retail RPs-in amounts of less than $100,000), and balances in retail money market mutual funds. Excludes individual retirement account (IRA) and Keogh balances at depository institutions and money market funds. Seasonally adjusted M2 is computed by summing savings deposits, small denomination time deposits, and retail money fund balances, each seasonally adjusted separately, and adding this result to seasonally adjusted M1.

- (M-3)

- Consists of M2 plus large-denomination time deposits (in amounts of $100,000 or more), balances in institutional money funds, RP liabilities (overnight and term) issued by all depository institutions, and Eurodollars (overnight and term) held by U.S. residents at foreign branches of U.S. banks worldwide and at all banking offices in the United Kingdom and Canada. Excludes amounts held by depository institutions, the U.S. government, money funds, and foreign banks and official institutions. Seasonally adjusted M3 is calculated by summing large time deposits, institutional money fund balances, RP liabilities, and Eurodollars, each adjusted separately, and adding this result to seasonally adjusted M2.

(from the Board of Governors Federal Reserve System - December 12, 2003)

Monetarism evolved out of the classical quantity theory which started with the identity called the equation of exchange and turned it into a theory of the determination of price level changes. The equation of exchange states that Money times its Velocity must be equal to the quantity of real output times their prices. That is to say that MV must equal OP where equals is three short horizontal lines and not two of them.

By arguing that Say’s Law prevailed, output was close if not equal to its capacity level, and if the velocity of money was constant, the price level was determined by the quantity of medium of exchange money (now referred to as M-1 money). Remember that checkable deposits have dominated transactions in the legitimate or above ground economy only in the last century and one half or so. Some estimates place the settlement of transactions in the legitimate or above ground economy using checkable deposits at around 90% with the remaining g settled with the use of currency. The underground or illegitimate economy is quite a different picture where nearly all transactions are settled with the use of currency. When the quantity theory became popular, currency was the dominant form for settling transactions. While currency is still nearly half of all M-1 money, much of it is in the rest of the world where it serve as the currency of choice by people who do not trust their own nation’s currency for obvious reasons.

Federal Reserve Bank of New York Staff Reports

Cash Dollars Abroad

https://www.newyorkfed.org/medialibrary/media/research/staff_reports/sr400.pdf

A recent strand of the literature estimates the stock of banknotes held abroad (Porter and Judson 1996, Feige 1994, 1996, 1997, and Doyle 2001). Porter and Judson (1996) find that 70 percent of U.S. dollars were held abroad in the 1990s, rising from 40 percent in the 1960s.

Board of Governors of the Federal Reserve System Money Stock Measures - H.6

www.federalreserve.gov/releases/h6/

The Bugaboo of Monetarism: the instability and difficulty in predicting reliably the velocities of the monetary aggregates

Recall that the velocity of the a monetary aggregate is determined by dividing nominal GDP (usually for one year since product is a flow concept) by the quantity of the monetary aggregate in question as on a given date or its average for a period of time such as one calendar year since the monetary aggregate is a stock concept. Most monetarists use a monetary aggregate that is more inclusive than M1 such as M-2 or M-3. For some monetarists, a more customized measure of money is preferred than the officially defined ones. The more inclusive is the monetary aggregate, the more stable it velocity tends to be. As the monetary aggregate becomes more broadly defined or more inclusive, it includes more of the close substitutes and switching from one such as savings accounts to money market mutual fuds in the broader aggregates need NOT entail moving out of a less inclusive aggregate into a more inclusive one. The problem is that the more inclusive is the monetary aggregate that is more correlated to changes in the price level, the more complicated is the control of that aggregate by the monetary authority such as the FED.

As more liquid financial products and processes were added during this period of time, the walls of separation between the monetary aggregates became more porous and their velocities became more unstable and less predictable. Monetarism had reached its zenith and began to fall in popularity as well as u buts usefulness to the FED for guidance in determining and executing monetary policy to control price level changes such as inflation.

The Velocity of Money and its impact on the Success of or Failure of Monetary Policies guided by Monetarist Doctrine

The velocity of the monetary aggregate and its stability and predictability are critical issues since its stability or lack of it is important in discerning whether or not monetarism is helpful in understanding price level changes and in forming monetary policy to control those changes. Monetarism and its most influential modern proponent, Milton Friedman reached their peak of modern popularity in the Great Inflation from about 1973 through earl 1980. The resulting change in financial products and process caused by the very high inflation was its undoing. For skeptics, be careful what you predict, for like Phoenix, monetarism may rise again when changes in the financial landscape have slowed appreciably and the velocities of the monetary aggregates stabilize.

The Nature and Shocks that Cause Changes in the Financial Landscape and the Velocities of the Monetary Aggregates

The major initiating cause of the accelerating inflation rate in this period was assertion of the Organization of Petroleum Exporting Countries (OPEC) in respect to production and pricing decisions of the Seven Sisters, the name given the major oil companies holding the concession to produce oil in these nations. These production and pricing decisions would no longer be determined by the Seven Sisters but rather by the countries from where the oil came. This new assertive role of OPEC has continued down to recent times when a phenomenon called FRACKING exploded on the scene after a rather lethargic period of existence. Domestic production from Marcellus Shale, Bakken, and Eagle Ford, suddenly became the ‘plays’ as they are often termed.

In macroeconomic theory, the resulting acceleration of inflation from the oil shock is referred to as a form of cost push inflation rather than demand pull inflation. It is a much more difficult form of inflation facing the monetary policy makers than is demand pull inflation.

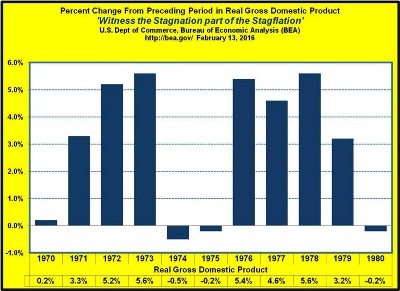

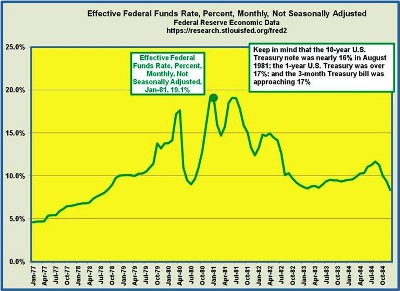

To ease the economic adjustments to the new more aggressively cartelized oil markets and reduce the negative effect on the level of domestic economic activity, the FED adopted a high inflation rate strategy which as a side effect, aided the significant increase in the inflation rate. Its purpose was to ease the adjustment of many now energy inefficient manufacturing firms to be gradually updated or replaced given the new reality of an OPEC using its market power to maximize profits. As the inflation rate in the U.S. approached the 20% rate, the FED finally let the hammer down in 1980/1981 and squelched most of the inflation with the side effect of a temporally collapsing the real level of real economic activity.

The Change in Reality that began the Great Inflation and the Pursuant Changes in the Financial Landscape and Monetary Policy

Recall that two major oil price increases after OPEC reconstituted the cartel. The first price shock came in 1973, raising the per barrel price from $3.50 to $14.00 and the second in1978 from $19 per barrel to $38 per barrel. The several year drift in crude oil prices from $14 to $19 more or less matched he accelerating price inflation between the two major price hikes of the reconstituted oil cartel, OPEC.

This tumultuous period of economic chaos had a great impact on the financial system and the real activity in the economy as well. The tremendous pressure for a shorter work week which had been building up for a number of years, disappeared quickly. The need for replacing much of the manufacturing infrastructure which had become energy inefficient now became paramount. Accompanying this push to new or upgraded manufacturing facilities that were more energy efficient was also a rapid increase in financial products and processes that became available to help cope with the rocketing inflation rate. These financial changes were to destabilize the velocities of the monetary aggregates and make its predictability increasingly difficult. In part to satisfy the broad range of definitions of the monetary aggregates used by various viewpoints of the monetarists, the FED began to report and publish the various measures of the monetary aggregates culminating in M-1 through M-5.

What Destabilized the Velocities of the Monetary Aggregates?

As we pointed out earlier in this newsletter, the stability of the velocity of the monetary aggregates or at least the reliability of estimates of the changing velocities is necessary if monetarism is going to be useful in guiding monetary policies that control price level changes such as inflation. As also noted previously, textbooks of an earlier generation stressed that money plays several roles in our economy. It is a liquid store of value, a standard of deferred payment, a unit of account as well as the medium of exchange. One definition and measure of money cannot meet all of these goals, hence the multiplicity of definitions and measures of money. When inflation accelerates to high levels such as 10%, 15% and even 20%, a zero nominal rate of interest on cash balances of firms, which is the usual case, becomes a real negative rate of interest equal to the actual rate of inflation occurring at the time. Strict cash management becomes crucial. The phenomenon of swept balances becomes one way of minimizing the loses from idle cash balances now carrying a large negative yield due to a high and accelerating inflation rate.

For large enough firms more aggressive use of overnight investments such as Eurodollars, carried large enough nominal yields to offset at least most of the negative effect of inflation in their real yields. While some forms of kiting cross the line of illegality, that line was more closely approached to lessen cash balances. These were but a few of the changes in cash management that began to occur. The net effect was to increase the velocity of the narrower monetary aggregates like M-1 and M-2. As these new products and processes evolved to aid in combatting the effects of accelerating inflation on real yields, the FED increased the number of regularly reported and measured monetary aggregates. The popularity of monetarism declined as these changes occurred. The determination and execution of monetary policy suffered from these rapid changes. Also making monetary policy more difficult to formulate and carry out in the battle against inflation was the fact that cost push inflation is a much more difficult form of inflation to control than is demand pull since the containment of inflation when cost push is the source of the problem requires policies that depress aggregate demand thus adding to the recessionary effects of an already declining economy.

At the commercial level, other than trade credit extended by sellers to buyers, credit is extended by financial institutions to borrowers in one of two ways. Depository institutions such as commercial banks can create new M-1 money usually in the form of checkable deposits and lend them to the borrower in exchange for a an asset labeled as a loan receivable on the bank’s balance sheet.

The other financial institutions that are not depository institutions such as finance companies create credit by increasing the velocity of M-1 money.

One of the major effects of serious inflation is it leads to new financial products and processes that break down the walls of separation between the monetary aggregates and tend to destabilize the velocities of the monetary aggregates, especially the less inclusive measures of money. This happened during the period of 1973 to 1980 and led to the decline in the popularity of monetarism as a guide to monetary policy makers.

The financial crisis of 2008-09 and the huge additional to the portfolio of assets of the FED as a result of the rounds of Quantitative Easings has put the FED in a position of using open market operations to control the entire spectrum of interest rates of all maturities and eliminated the possibility of a Greenspan type conundrum. The chaos of the Great Inflation of 1973-80 and the Great Recession resulting from the financial crisis of 2008-09 did have some positive byproducts.