2022 Volume Issue 2

June 14, 2022

For a downloadable version, click the following:

June 2022 --- What a mess!

Jawboning…a technical term --- a government official can reduce inflation and bring about prosperity by just talking about it - trust me.

Examples speak volumes… President Biden on June 10, 2022 while touring the Port of Los Angeles.

Biden vows to battle inflation as prices keep climbing

"My administration is going to continue to do everything we can to lower the prices for the American people."

"The president's policies, his deals with the private sector, regulatory actions and public jawboning have failed so far to stop prices from marching upward."

Pictures speak/illustrate even more clearly…

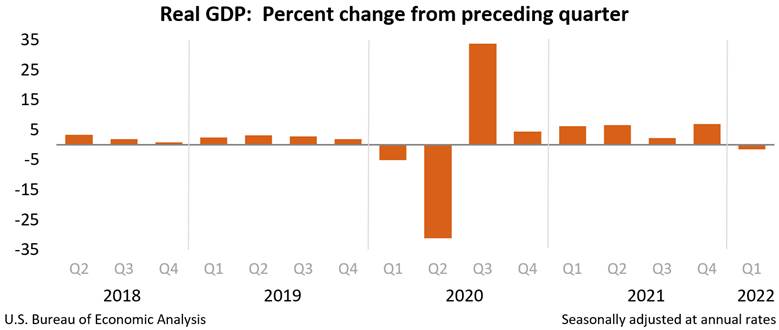

Real GDP (Gross Domestic Product) shrank by 1.4% in the 1st quarter (Jan - Mar 2022)

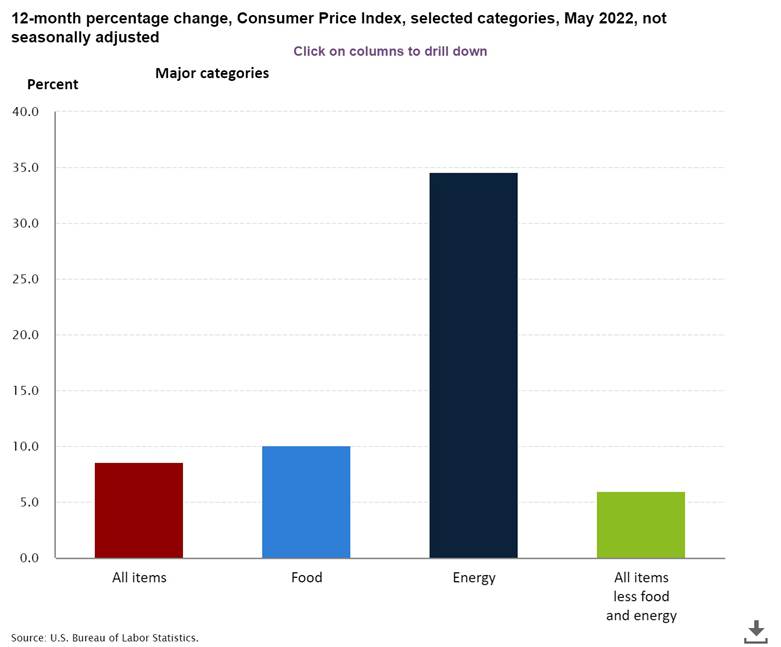

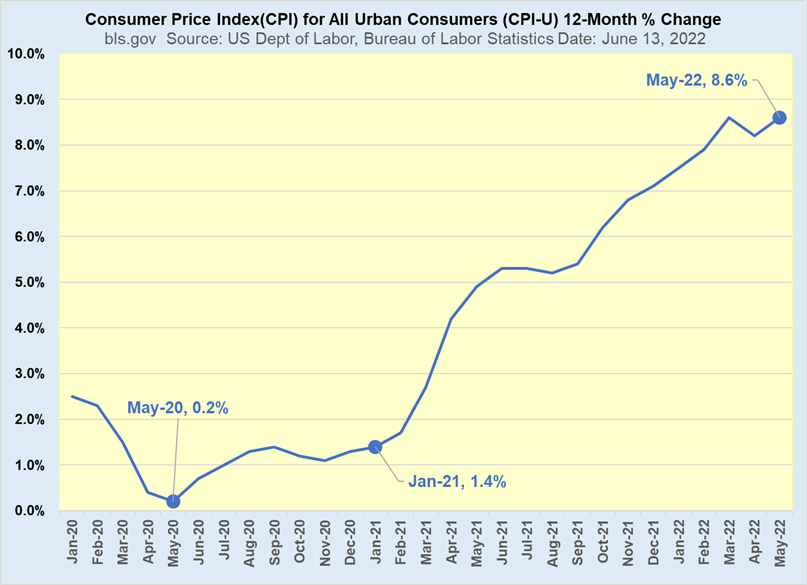

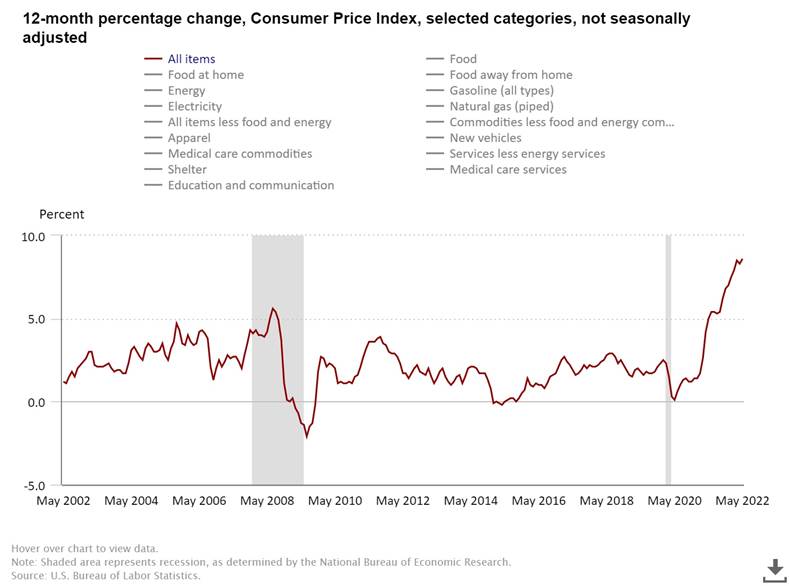

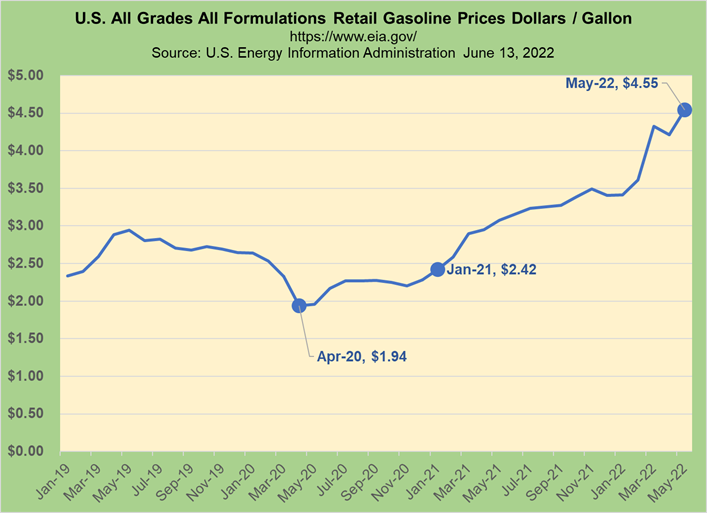

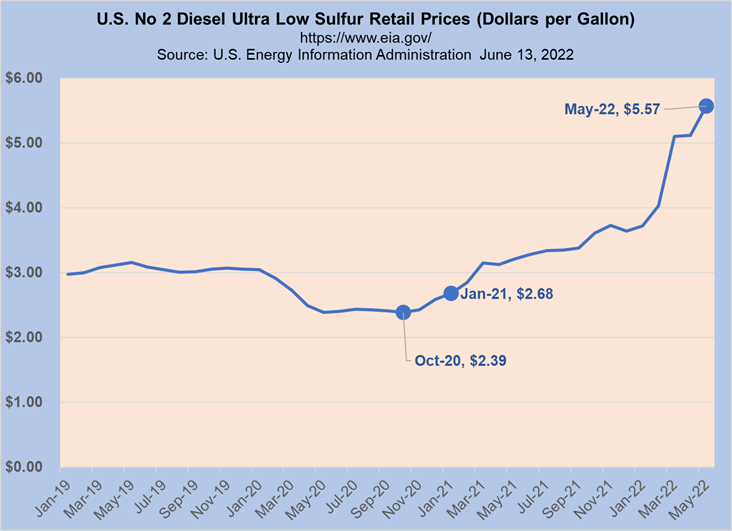

Consumer prices rose by 8.6% in May 2022

Current CPI (Consumer Price Index)

May 2022 12-month change (June 2021 - May 2022) 8.6%

Food up 10.1%

Energy up 34.6%

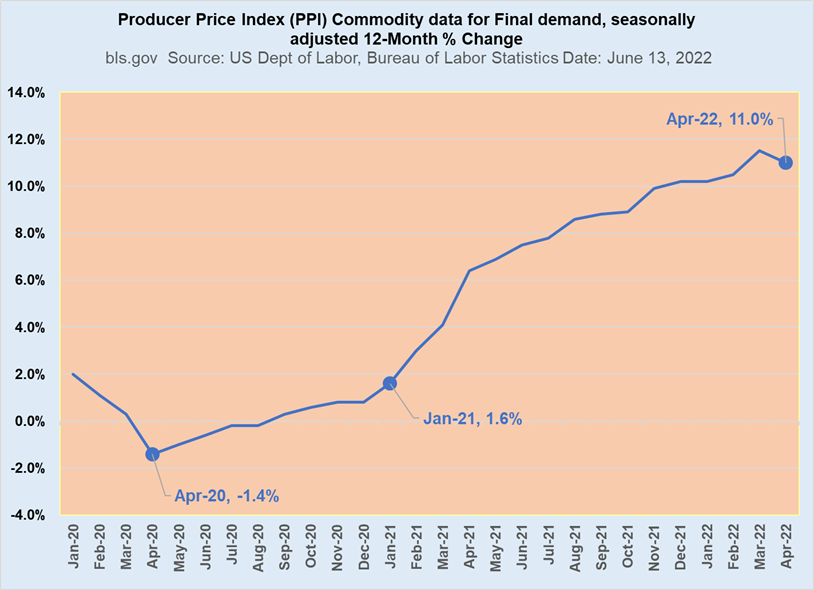

Prices at the producer level rose by 11.0% in April 2022

Current PPI (Producer Price Index)

April 2022 12-month change (May 2021 - April 2022) 11.0%

Taming Inflation

Cost push inflation can only really be addressed from a policy perspective - at the federal level, by executive and legislative branches. This would entail promoting access to energy sources (crude oil, natural gas production), encouraging continued re-entry into job markets, and other supply side issues.

On the demand side (demand pull inflation), the Federal Reserve, in the form of its policy making power through the FOMC - Federal Open-Market Committee, has a particularly tough task. Yes, it could reduce inflation on both sides - demand pull and cost push by driving up the Federal Funds Rate (from which all other interest rates are basically derived); but bear in mind that it wouldn’t address the underlying problem on the supply side, which again could only be fully addressed by executive/legislative actions at the federal level in particular and by the actions of market participants themselves.

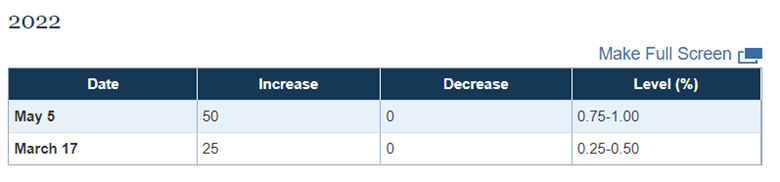

Regardless, the Federal Reserve - FED (through its monetary policy making body, Federal Open-Market Committee - FOMC) has embarked on a path of interest rate increases to help slow down borrowing and thus, slow down economic activity.

Federal Funds Rate

Federal Reserve Board - Open Market Operations

https://www.federalreserve.gov/monetarypolicy/openmarket.htm

These last two increases are just the opening salvos and there will be a series of hikes coming in short order from 0.25-0.5 to 0.75-1.00. We can be fairly certain that the FED (FOMC) will be very aggressive going forward. The reality is that the FED has little choice but to move rapidly to increase those rates to significantly higher levels.

The FED’s latest Conundrum/Challenge - how to slow inflation without crashing the economy…

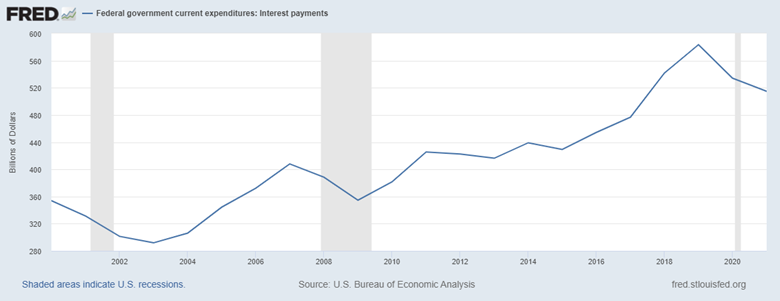

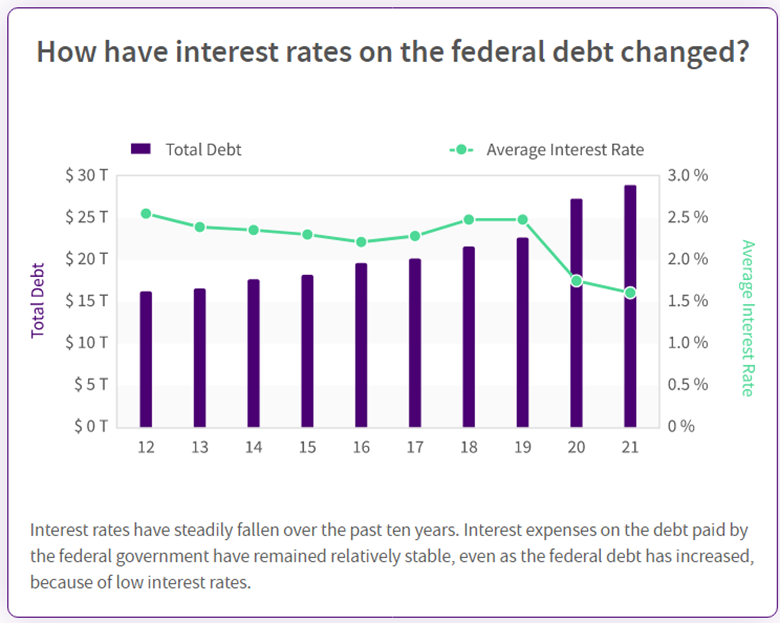

The FED has two basic problems: 1) it must tamp down inflation aggressively, or it will spiral out of control; and 2) it must not keep those rates high for any length of time. The reason for the latter has to do with our federal debt.

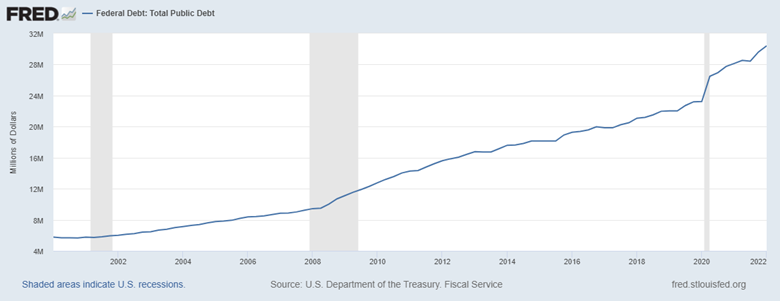

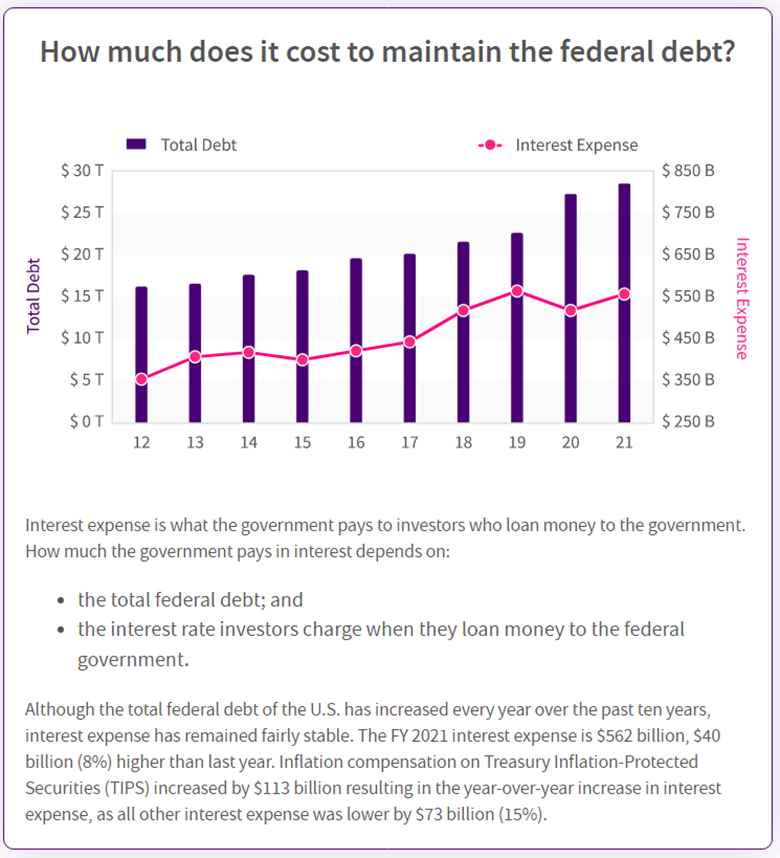

The Backdrop - servicing the debt

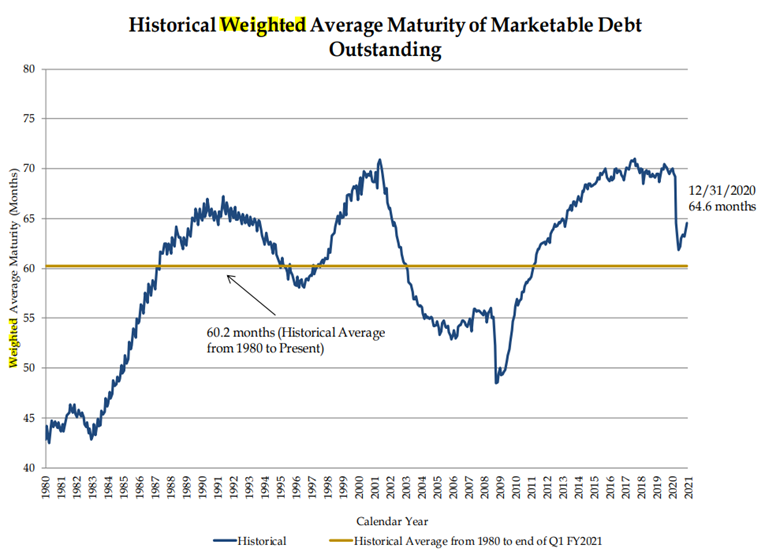

The current federal debt is at $30.4 trillion and we are paying a bit over $500 billion per year to service that debt - interest payments on that debt. The average maturity of that debt is around 5 years. Keep in mind that the debt consists of Treasury securities with maturity dates ranging from 30-days to 30 years. In short, since we won’t be paying off that debt any time soon, that debt will roll-over in five years and the Treasury will have to issue new debt.

Government - Debt to the Penny (Daily History Search Application) (treasurydirect.gov)

https://treasurydirect.gov/govt/reports/pd/debttothepenny.htm

$30.4 trillion U.S. Federal Debt

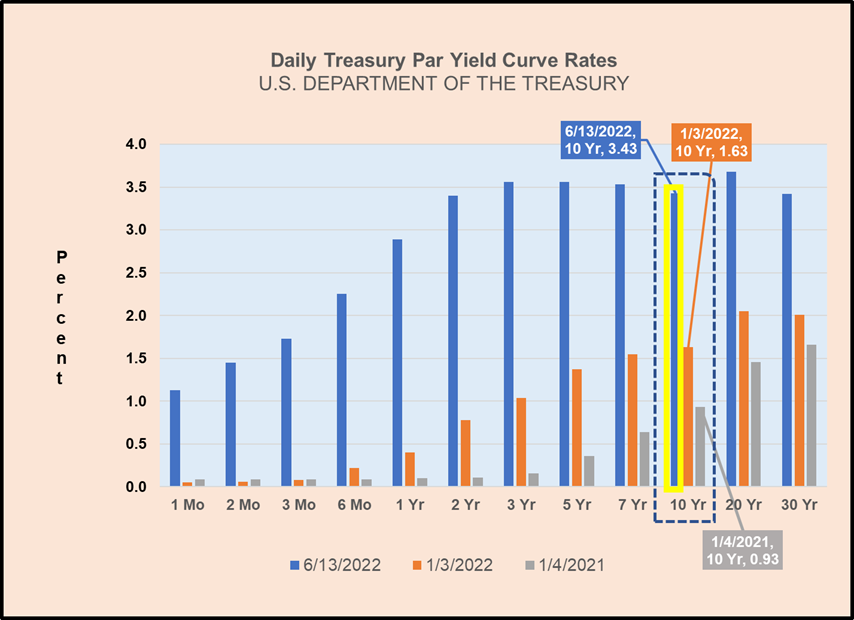

That current average interest rate paid on that $30.4 trillion is around 1.5% --- very low. If the FED drives up interest rates for any length of time, the interest on new issue Treasury securities will rise as well - as is currently the case. The 10-year US Treasury Note is at 3.43% (June 13, 2022) while last year it was 1.45% (June 10, 2021).

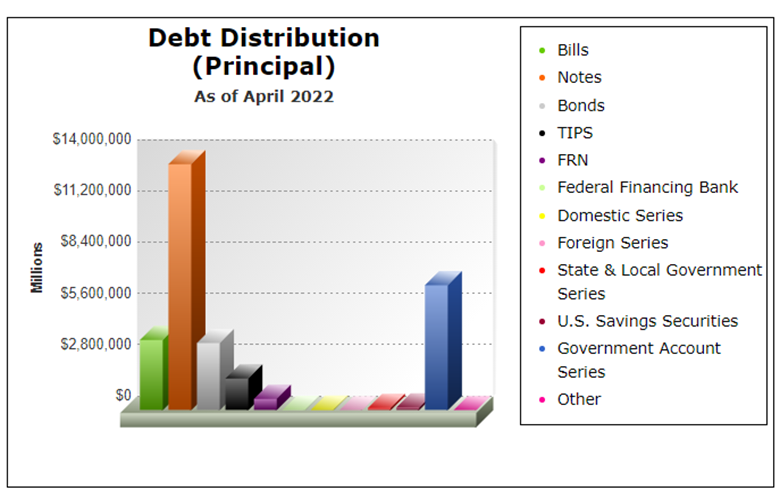

The average maturity of Treasury's $30+tril portfolio is around 62 months, with majority of holdings in notes (1-yr >>> 20-yr) Government - Debt Distribution (treasurydirect.gov)

https://www.treasurydirect.gov/govt/charts/principal/principal_debt.htm.

TreasuryPresentationToTBACQ12021.pdf

https://home.treasury.gov/system/files/221/TreasuryPresentationToTBACQ12021.pdf

Summary of debt for the United States | U.S. Treasury Data Lab (usaspending.gov)

https://datalab.usaspending.gov/americas-finance-guide/debt/analysis/

Here’s the problem…two scenarios

First…

Let’s just say that the FED takes its time in trying to bring down inflation and that average interest on the debt goes from 1.5% up to 3.0%, that means that the interest paid on servicing that debt will top $1.0 trillion annually (if it went to 4.5% that would move the interest payments to $1.5 trillion).

Second…

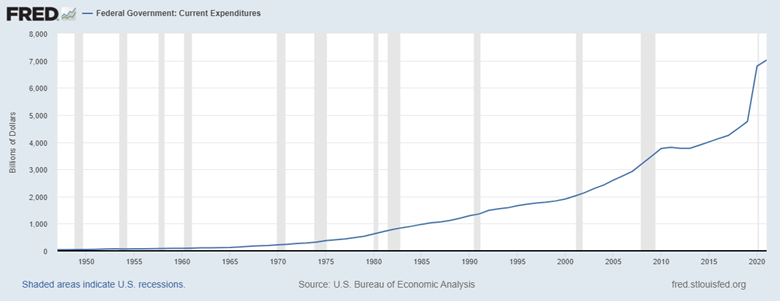

From how I see it, the FED has no choice but go strong and fast in pressuring up interest rates. The reason why I am focusing on the servicing of interest on the debt is that the funding must come from the current budget.

2021 Current Federal Government Expenditures: $7.0 trillion

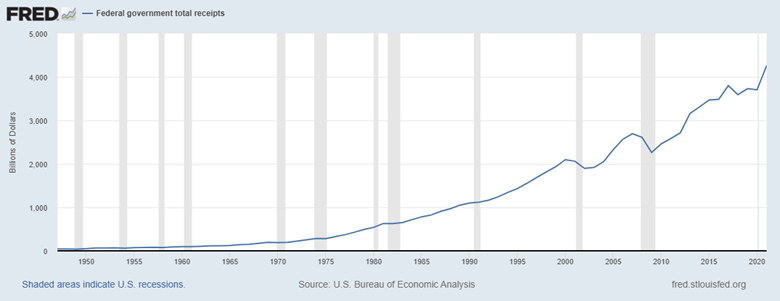

2021 Current Federal Government Receipts: $4.3 trillion

Action…

Keep in mind that if the FED acts swiftly and aggressively, this will cause a great deal of pain and the pretty much certain recession, and again, it will be painful. If they move more slowly, there will still be significant pain from a more extended recession that will certainly result in an even further fall-off in tax receipts, resulting in compounded budgetary problems.

I have no idea how a recession can be avoided at this point considering the stance taken on energy and still relatively weak labor markets and other supply issues; in conjunction with the large amount of money still sloshing around from the stimulus payments and other government programs that are keeping labor force participation rates lower than where they would otherwise be.

Labor Force Participation Rate (LFPR) = Labor Force [employed + unemployed] / Civilian Noninstitutional Population [Labor Force + Not in labor force]

Labor Force Participation Rate: February 2020 63.4%

Current Labor Force Participation Rate: May 2022 62.3%

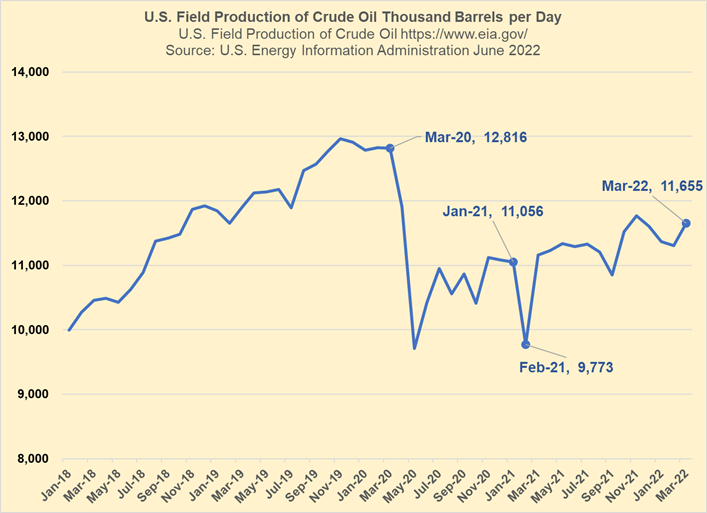

Crude Oil Production March 2022 = 11,655,000 barrels per day

Crude Oil Production March 2020 = 12,816,000 barrels per day

Will the FED be able thread the needle in tamping down inflation, while avoiding an extended recession? A recession is pretty much inevitable at this point - it’s really just a matter of how long it will last and how much damage will result.

To be continued…