2012 Volume Issue 5

March 6, 2012

For a downloadable version, click the following:

Has the US Economy Stalled? pdf

…a bit more compressed version of the PDF

HAS THE U.S. ECONOMY STALLED?

…or as the composition by J.S. Bach tells us, Sleepers Awake! (Wachet Auf!)…and connect the dots!

In the past several weeks, testimonies by officials of the Federal Reserve System (FED), news releases of several federal governments agencies such as the Bureau of Economic Analysis (BEA), and a variety of private sector reports have come forth like the proverbial 'shot across the bow' in a kind of a wakeup call that cuts through the 'fog of the ongoing political war' called the presidential election campaign.

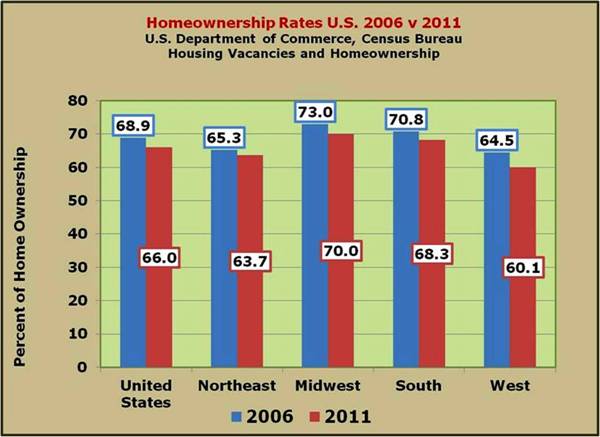

On February 28, 2012, Federal Reserve Board Governor Elizabeth A. Duke testified before a Committee of the U. S. Senate and joined in with a warning about the dismal outlook for household spending due to the continued decline in the housing picture. Her comments were reinforced by a repost from a private housing sector tracking service, S&P/Case-Schiller.

Federal Reserve Board Governor, Elizabeth A. Duke

The Housing Market

Before the Committee on Banking, Housing, and Urban Affairs, U.S. Senate, Washington, D.C.

February 28, 2012

www.federalreserve.gov/newsevents

The extraordinary fall in national house prices has resulted in $7 trillion in lost home equity, more than half the amount that prevailed in early 2006. This substantial blow to household wealth has significantly weakened household spending and consumer confidence. Another result of the fall in house prices is that around 12 million households are now underwater on their mortgages--that is, they owe more on their mortgages than their homes are worth.

Housing White Paper - The U.S. Housing Market: Current Conditions and Policy Considerations

January 4, 2012

federalreserve.gov/publications

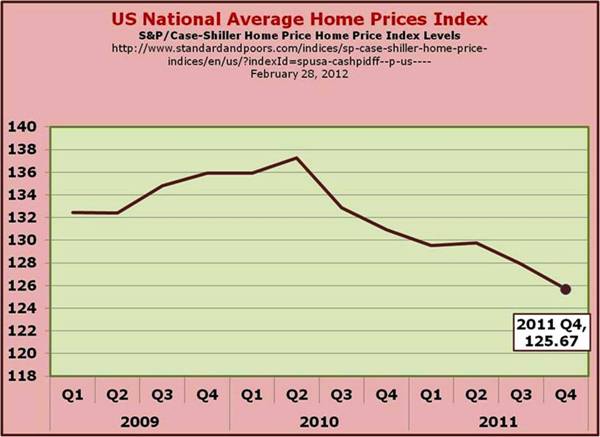

The S&P/Case-Shiller 10-City and 20-City Composites lead the National to new lows

February 29, 2012

Do you remember the former FED Board Chairman Alan Greenspan's remarks about the IRRATIONAL EXUBERANCE in respect to household spending? It was based upon the Wealth Effect due primarily to what has been described as the Housing Bubble. Failing to prevent the bubble from occurring in the first place, the FED implemented policies to help burst that bubble, leaving millions of homeowners under water or much worse.

To summarize: as Oliver Hardy used to tell Stan Laurel, "Well, here's another nice mess you've gotten me into!"

www.econnewsletter.com/jun082011.html

In Greenspan's own words, "Our forecasts and hence policy are becoming increasingly driven by asset price changes. The steep rise in the ratio of household net worth to disposable income in the mid-1990s, after a half-century of stability, is a case in point. Although the ratio fell with the collapse of equity prices in 2000, it has rebounded noticeably over the past couple of years, reflecting the rise in the prices of equities and houses."

Remarks by Chairman Alan Greenspan

Reflections on central banking

At a symposium sponsored by the Federal Reserve Bank of Kansas City, Jackson Hole, Wyoming

August 26, 2005

www.federalreserve.gov/Boarddocs

Was $7 trillion in lost homeowners' equity and 12 million homes under water enough of a reduction in asset prices for you, Mr. Chairman?

The wealth effect has now turned negative. Rationality by households calls for hunkering down.

Last week, Ben Bernanke, Chairman of the Federal Reserve Board added his voice to the wake-up call in a pair of testimonies before Congressional Committees.

Chairman Ben S. Bernanke: Semiannual Monetary Policy Report to the Congress

- Before the Committee on Financial Services, U.S. House of Representatives, Washington, D.C. on February 29, 2012

- Before the Committee on Banking, Housing, and Urban Affairs, U.S. Senate on March 1, 2012

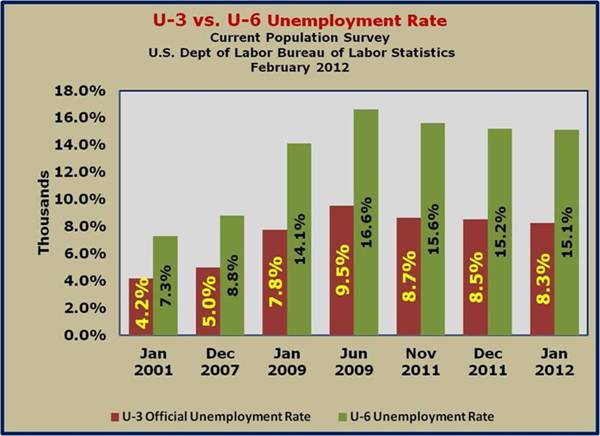

The unemployment rate remains elevated, long-term unemployment is still near record levels, and the number of persons working part time for economic reasons is very high.

Real household income and wealth were flat in 2011, and access to credit remained restricted for many potential borrowers.

The outlook for the labor market is dismal. The discouraged workers, those wanting to work but having given up looking due to no prospective jobs in sight, number in the millions and are better revealed in the U-6 unemployment rate (15.1%), the realistic measure not the sugar-coated measure called U-3 (8.3%). They are also reflected in the sharp fall in the labor force participation rate over the past few years as pointed out on this web site on several occasions.

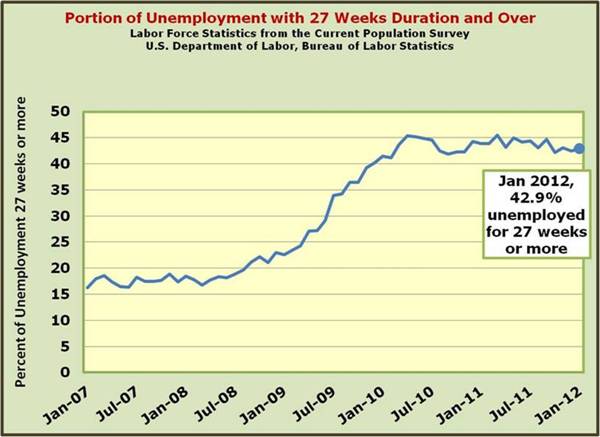

The half-year plus duration (27 weeks +) of a large number of unemployed constitutes more than 40% of those listed as unemployed and has been above that 40 percent mark for more than a year.

The entire labor force psychology has been altered over the last few years and in spite of the falling unemployment rate as measured by the sugar-coated U-3 rate over the last few months, the truth is that people continue to leave the labor force in droves because of no job prospects out to the horizon. Keep in mind the Labor Force is a subset of the Civilian Noninstitutional Population, those people 16 years and older (not in the military, incarcerated or other institutions) who are employed and those listed as unemployed…seeking employment.

Those individuals who are no longer in the Labor force have left in droves due to the lack of job opportunities and are either forced to turn to families or government assistance to survive. The Labor Force Participation Rate, which had been in the 67% range as recently as 2007, dropped below 64% and continues to fall. The Labor Force Participation Rate (LFPR) represents the total of the Labor Force (employed + unemployed…and still searching for a job) as percent of the Civilian Noninstitutional Population (which includes everyone 16 years of age and older). Simply put, when people fall out of the ranks of the labor force, they are no longer included in the employment/unemployment numbers.

One more consideration is in order. If we are going to reduce the size of our military, which are now not considered part of the labor force, as they muster out to civilian life and they begin to look for work, they will be counted as unemployed and thus part of the labor force and increase the labor force participation rate. This will increase both the U-3 sugar-coated rate as well as the realistic U-6 rate. Should they not find work and become "discouraged' and no longer seek employment, they will not be considered unemployed and not in the labor force and therefore reduce the LFPR. The more realistic U-6 measure will show them as unemployed. How large of an effect? You plug in the size of the force reduction (whatever size is decided upon 100,000, 200,000) and then make the calculations.

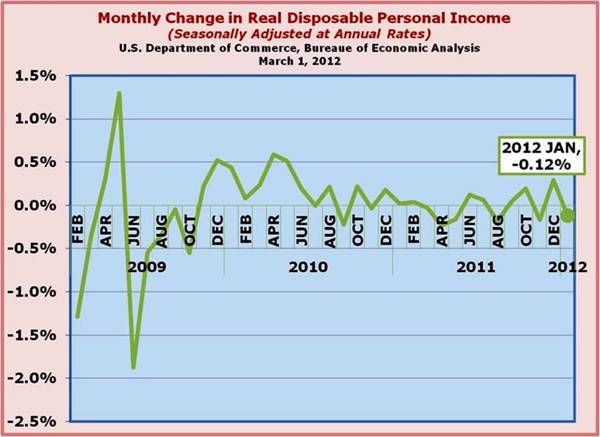

Real Disposable Personal Income looks like a flat line on the patient's heart monitor.

PERSONAL INCOME AND OUTLAYS, JANUARY 2012

U.S. Department of Commerce, Bureau of Economic Analysis

Personal income increased $37.4 billion, or 0.3 percent, and disposable personal income (DPI) increased $14.1 billion, or 0.1 percent, in January, according to the Bureau of Economic Analysis.

Real disposable income decreased 0.1 percent in January, in contrast to an increase of 0.3 percent in December.

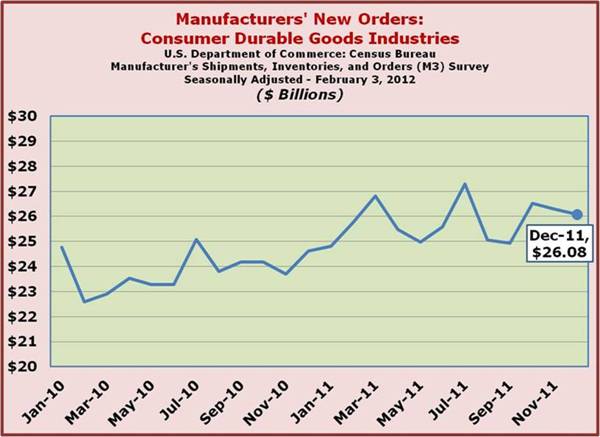

Durable goods took a nosedive last month. The decline was in both consumer durables as well as an even larger decline in business durables spending.

Home prices continue to fall and household net worth still depressed.

The testimony by Federal Reserve officials and the latest S&P/Case-Schiller report on housing indicates the bottom of housing prices has not yet been reached as prices last month fell further.

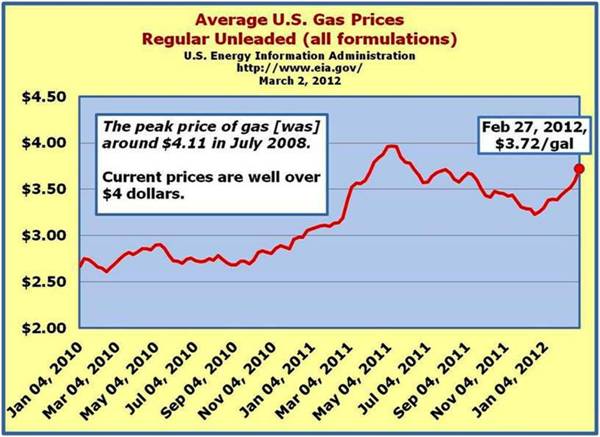

OIL AND PETROLEUM DERIVATIVE PRICES

Despite (and also a major cause of) petroleum product prices like gasoline flirting with record levels, major refineries supplying the U.S. are shutting permanently.

A major player in the natural gas market, Chesapeake Energy, has announced its intention to significantly cut back its production because of low natural gas prices. The significant uptick in the supply of natural gas has been the one bright spot in all this news.

-Chesapeake to cut natural gas production by 8%

-Natural gas prices at 10-year low amid production boom

-Chesapeake's move "throws down gauntlet" for other producers, analyst says.

The glut of natural gas partly stems from the U.S. energy industry's success with new exploration techniques, notably hydraulic fracturing of shale formations, or fracking.

In Argentina, the government is pressuring their domestic oil producers to step up production or lose their licenses/leases.

March 2, 2012

Chubut Province Governor Martin Buzzi has given the battered oil and gas company YPF SA (YPFD.BA, YPF) seven days to present plans to raise production at three fields in the province or lose its concessions.

Buzzi leads a group of governors from Argentina's top oil-producing provinces that has been highly critical of oil and gas companies, saying they aren't investing enough. The group recently gave the companies, including YPF, two years to boost production by 15% or lose their concessions.

As Henry Morgenthau said of FDR's policies, we can say of recent and current economic policies, they are not working and the unemployment rate is horrible and the Federal Government's budgetary deficit continues to be huge causing the national debt to rise meteorically. To paraphrase the popular song heard around the Christmas season, "We're beginning to look a lot like Europe."

Henry Morgenthau Jr. — close friend, lunch companion, loyal secretary of the Treasury to President Franklin D. RooseveltWe have tried spending money. We are spending more than we have ever spent before and it does not work.

I say after eight years of this Administration we have just as much unemployment as when we started. … And an enormous debt to boot!

The date: May 9, 1939. The setting: Morgenthau's appearance in Washington before less influential Democrats on the House Ways and Means Committee.

Déjá Vu?

Are you beginning to experience a sinking feeling that history may be repeating itself? Are the last few years beginning to look more like the Great Depression years? Are the policy failures referred to by Henry Morgenthau back in 1939 being mirrored by current economic policies? Is it as bad as the Conference Board's Kenneth Goldstein's very dismal warning issued recently?

Conference Board Economists: U.S. Economy Transitioning To A New Normal

The economy that we had before the recession is gone, said Kenneth Goldstein, economist at the Conference Board. It's not coming back. The U.S. economy is transitioning to a new normal in which businesses invest less and consumers spend less than before the recession, Goldstein told The Huffington Post in an interview last week. As a result, he said, economic growth and job growth will be slower than before.

How did we get into this mess? How can we extract ourselves from it?

Mafia level credit card rates did not help. Reluctance to make loans by financial institutions and reinforced by regulators closing a large number of financial institutions has not helped either. The excess capacity to create credit is there in abundance. But economic dangers lurk everywhere. The great cloud of uncertainty overhangs one of the largest sectors in our economy, health care. Sovereign risk stalks many nations and is beginning to cast a shadow on the sky rocketing national debt of the U.S.

Despite a proven abundance of domestic energy reserves, bad environmental policies along with cartelistic control of both foreign and domestic energy reserves cause unreasonably high energy prices especially in downstream petroleum markets such as gasoline. Income redistribution is the obsession with the White House instead of real income growth. As in the days of Hoover and early FDR, promoting big government is in and tax increases are the easy way to assure its success, so the pundits argue.

Remember that is the only world we have and though daunting, we have to work our way out of this tangled mess. Don't lose faith. We'll do our level best to help you recognize the dots, and then we have to follow them to their logical conclusion. As we indicate on the first page of our newsletter, we're about logic, not ideologic.

In upcoming newsletters, we will focus on the leading culprits causing the stall out of the U.S. economy, such as energy [and related] policies, the trade deficit, and others.