Sign up for our Newsletter

Please fill out the following:

2012 Volume Issue 8

March 27, 2012

For a downloadable version, click the following:

…a bit more compressed version of the PDF

High Gas Prices - Recipe for Killing an Economic Recovery

The difference between the price of weather and gas prices

First the weather…

Everybody talks about the weather but nobody does anything about it.This quote, while typically associated with Mark Twain (Samuel Clemons), it was probably first used by his friend, Charles Dudley Warner.

And then Gas Prices… so you think it's all about demand and the prices on the world market, etc.? Well, think again. Here's some food for thought to consider.

People of the same trade seldom meet together, even for merriment and diversion, but the conversation ends in a conspiracy against the public, or in some contrivance to raise prices."Adam Smith-An Inquiry into the Nature and Causes of the Wealth of Nations

For [Adam] Smith, government should not seek to subvert the creative process that is the market, but should establish the framework necessary to keep it alive. It should enforce competition. It should not give in to the well-argued demands of monopolists and would-be monopolists. It should punish people and authorities who conspire to fix prices, divide up markets, or restrict production. "Monopoly," wrote Smith, "is a great enemy to good management."

Michael Forsyth MP (British)

Lest you think we are wagging a finger at just the big oil companies, you are wrong; we also see the machinations of environmental lobbyists and government itself conspiring to harm the consumer. Unlike the weather, something can and should be done about the price of crude oil, refined petroleum products and the entire spectrum of energy products we consume.

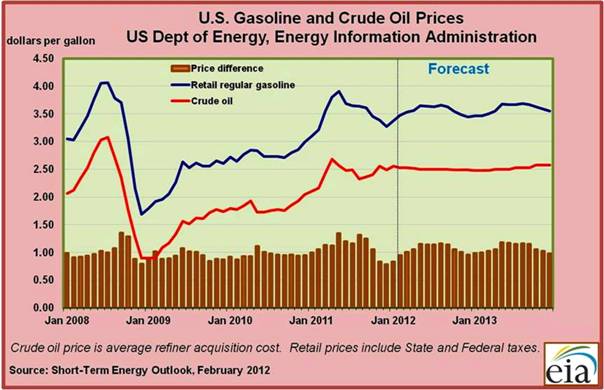

On March 10, 2012 we paid $4.039 per gallon for gasoline in Michigan. There's talk of $5 per gallon and more on the horizon over the summer

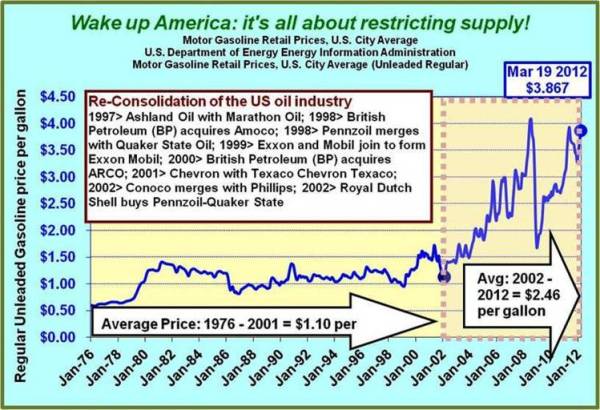

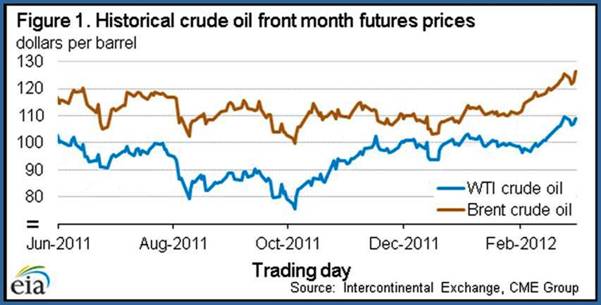

(www.youtube.com) The national average for [week ending 3/19/12] regular unleaded gasoline was $3.867 per gallon (U.S. Energy Information Administration (www.eia.gove/petroleum). The price of crude oil was $118.96 for Brent (imported) and $102.11 for West Texas Intermediate (domestic) in February 2012 (www.eia.gov)

If we look back to the summer of 2008, we saw national average gasoline prices of $4.11 and crude oil prices at the $145 per barrel level.

THE ECONOMICS OF CRUDE OIL PRICES AND THE IMPACT OF COMPETITION, OR THE LACK THEREOF

August 22, 2011

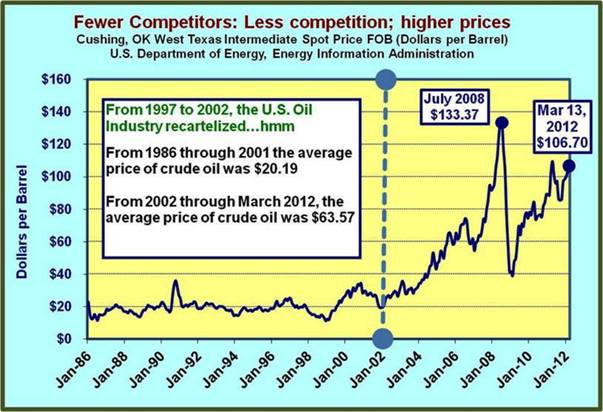

In 2004 OPEC (Organization of the Petroleum Exporting Countries) and OPIC (our acronym for domestic big oil - Organization of the Petroleum Importing Countries) struck again and raised their per barrel price from $35 and along with massive speculation in oil futures fostered by the same investment bankers that gave us (MBS) mortgage backed securities (CDOs, CDSs, etc.) and the financial chaos surfacing in 2008, the per barrel price rose to $145 in the June/July 2008.

With the ensuing recession, oil prices fell back to around the $40 range only to rise back up well above the $100 per barrel range.

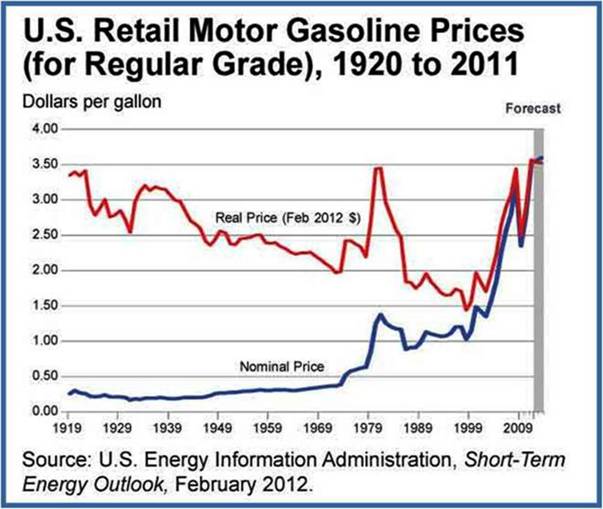

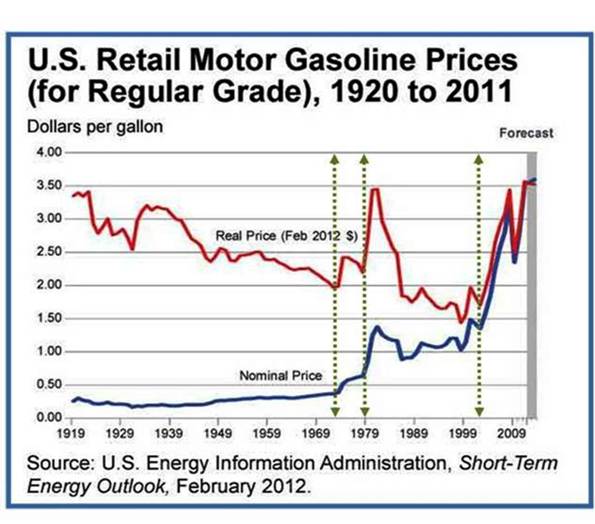

The first two dotted lines indicate the price spikes in gasoline resulting from OPEC oil embargo in 1973 and the fallout from the Iranian Revolution in 1979. Prior to 1973, the Seven Sisters controlled 85% of the world's oil supply. The group comprised Anglo-Persian Oil Company (now BP); Gulf Oil, Standard Oil of California (Socal) and Texaco (now Chevron); Royal Dutch Shell; and Standard Oil of New Jersey (Esso) and Standard Oil Company of New York (Socony) (now ExxonMobil). Following the consolidation (recartelization) of the domestic oil companies beginning in the 1990s and concluding around 2003, gasoline prices once again began rising and have remained high (note the third dotted line) due to the de facto expanded cartel, OPEC and OPIC within the U.S.

If prices at the pump in 2012 were at the 2004 level, we would be paying around $1.75 per gallon.

1990s --- MERGER MANIA --- higher prices today

Some of the arguments for consolidation included the desire to increase efficiencies and provide petroleum products at lower cost to the consumer…sure thing

- 1997 Ashland Oil combines most assets with Marathon Oil

- 1998 British Petroleum (BP) acquires Amoco

- 1998 Pennzoil merges with Quaker State Oil

- 1999 Exxon and Mobil join to form Exxon Mobil

- 2000 British Petroleum (BP) acquires ARCO (Atlantic Richfield)

- 2001 Chevron acquires Texaco to form Chevron Texaco

- 2002 Conoco merges with Phillips

- 2002 Royal Dutch Shell acquires Pennzoil-Quaker State

From May 2005

The Nature and Possible Solutions to the Current Energy Challenge

From 1991 through 2000, there were over 2,600 mergers in the petroleum industry. The largest of these mergers included Mobil and Exxon, the two biggest domestic oil companies at the time. As noted previously, the top three firms went from having about 20% market share to 30% market share. To put this in perspective, in the U.S. auto industry, the Big Three had over 90% of the domestic market share after WWII. Today, that same three have between 50 and 60%.

Federal Trade Commission

March 2007

Recent Mergers, Weak Anti-Trust Law Threaten Consumers

In just the last few years, mergers between giant oil companies-such as Exxon and Mobil, Chevron and Texaco, Conoco and Phillips-have resulted in just a few companies controlling a significant amount of America's gasoline, squelching competition. In 1993, the largest five oil refiners controlled one-third of the American market, while the largest 10 had 55.6 percent. By 2005, as a result of all the mergers, the largest five now control 55 percent of the market, and the largest 10 dominate 81.4 percent. This concentration has led to skyrocketing profit margins.

There has been much talk about energy independence, or more correctly, the dangers of being too dependent on imports: about supporting terrorist sponsoring regimes - or at least less-than likeminded 'allies'; environmental concerns over the endangered sage grouse and the like; whether or not domestic oil companies have the consumers' best interest in mind; and myriad other concerns from futures speculation to the wisdom of using up our seemingly dwindling reserves.

If you speak to a dozen people on these topics, you will receive several dozen opinions…

Most people would agree, however, that: 1) without low-cost energy, any hope of a strong economic recovery is not possible; and 2) the current price of petroleum products is far too high to make an economic recovery viable or lasting.

In subsequent articles, we will be discussing at least a few of the many aspects of the energy issues before us, but in this posting we will be focusing most of our attention on petroleum products.

First, a few facts:

1) The U.S. consumes around 18-19 million barrels of crude oil (or equivalents) per day.

When the economy expands, the consumption of crude oil will likely rise to the 20 to 21 million barrel per day range, where it was just a few years ago. As a percentage of the world oil usage, the U.S. has been consuming a shrinking portion for the last ten years or so.

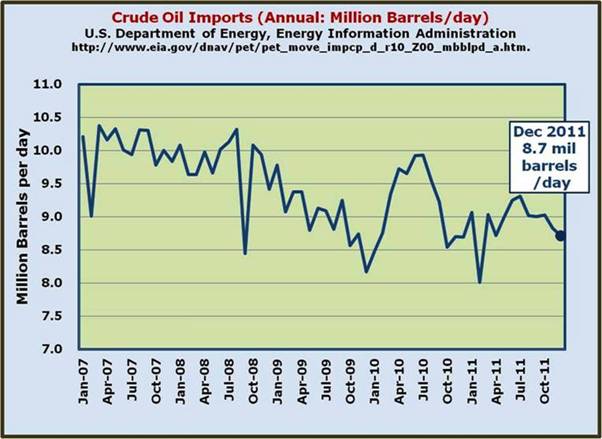

2) The U.S. imports 11 million barrels of oil per day, or roughly 2/3 of what is required.

There has been much in the news regarding fracking and horizontal drilling for natural gas. The huge potential of the Marcellus Shale, the Barnett Shale, Utica Shale, etc. is just beginning to be realized. The resulting boom in natural gas production has driven the price of natural gas from the $5-10+ per Thousand Cubic Feet, down to the $3-4 range.

U.S. Department of Energy, Energy Information Administration

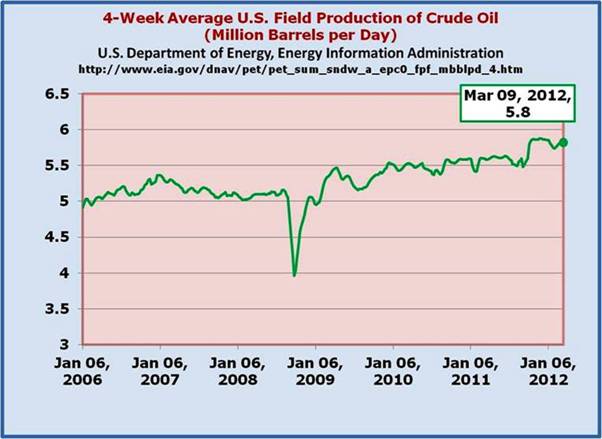

Employing the same type of fracking and horizontal drilling techniques used in the extracting natural gas, vast amounts of previously unreachable crude oil (typically along with natural gas and liquids) are adding to our domestic production.

March 9, 2011

Referring to Bakken…

It went from a mere 3,000 barrels a day in 2005 to 225,000 in 2010, according to the government's Energy Information Administration. EIA thinks it will produce 350,000 barrels a day by 2035, but most analysts think that estimate is far too low.

According to Harold Hamm, president of the energy company Continental Resources, it could produce a million barrels a day by 2020.

North Dakota crude oil production - Bakken (Williston Basin North Dakota and Montana)

Director's CutLynn Helms

NDIC Department of Mineral Resources

January Oil 16,927,453 barrels = 546,047 barrels/day (preliminary) (NEW all time high)

By Edward Klump - Mar 23, 2012 4:52 PM ET

Eagle Ford - Texas

Surging ProductionConocoPhillips (COP), the third-largest U.S. oil company, plans to boost production in the Eagle Ford to about 100,000 barrels of oil equivalent a day by the end of 2012 from more than 50,000 barrels a day in late December.

In last year's fourth quarter, Marathon Oil closed on purchases in the Eagle Ford for about $4.5 billion, according to a regulatory filing. The company said in February that daily output was about 15,000 barrels of oil equivalent in the formation, with plans for 30,000 barrels a day for the full year of 2012.

A Sanford C. Bernstein report last August estimated Eagle Ford production would reach 1.2 million barrels of oil equivalent a day in 2015, with 750,000 of that being liquids.

…and the really big daddy - Monterey/Santos

U.S. Department of Energy, Energy Information Administration

Review of Emerging Resources U.S. Shale Gas and Shale Oil Plays

July 2011

ftp://ftp.eia.doe.gov/natgas/usshaleplays.pdf

INTEK shale report's assessment of technically recoverable shale oil resources, which amount to 23.9 billion barrels in the onshore Lower 48 States. The largest shale oil formation is the Monterey/Santos play in southern California, which is estimated to hold 15.4 billion barrels or 64 percent of the total shale oil resources shown in Table 1. The Monterey shale play is the primary source rock for the conventional oil reservoirs found in the Santa Maria and San Joaquin Basins in southern California. The next largest shale oil plays are the Bakken and Eagle Ford, which are assessed to hold approximately 3.6 billion barrels and 3.4 billion barrels of oil, respectively.

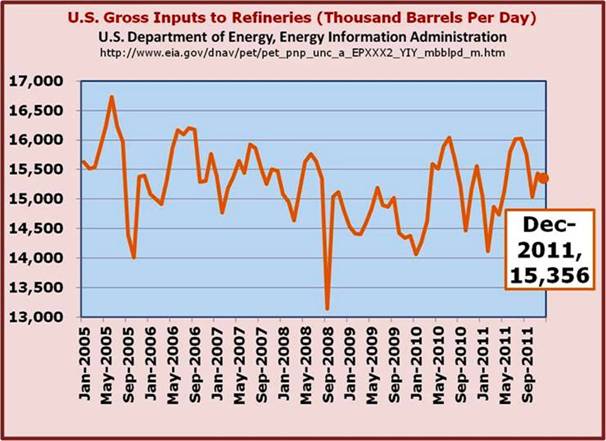

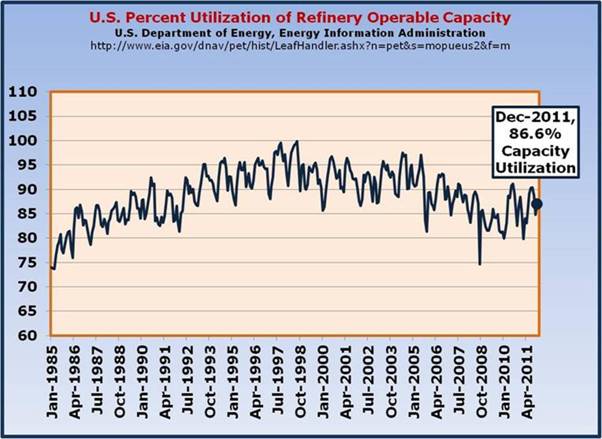

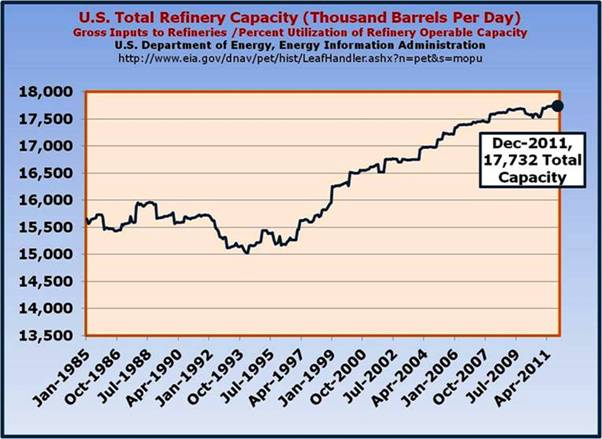

The good news on refineries…

3) While the U.S. hadn't built a new oil refinery since 1976, the capacity has risen due to renovation and expansion in older facilities.

There are two new facilities scheduled to come on stream:

Arizona Clean Fuels (Yuma, Arizona)

www.arizonacleanfuels.com is scheduled to launch in 2013. It has been in the works since 2007 (or earlier). It's scheduled to process 150,000 barrels per day.

Hyperion Center (Elk Point, South Dakota) www.hyperionic.com is scheduled to launch in 2015. It has been in the works since 2007 (or earlier). The refinery will be a 400,000 barrel-per-day greenfield facility. This highly-complex, full-conversion facility will produce green transportation fuels - ultra low sulfur gasoline and ultra low sulfur diesel.

With another in Pennsylvania geared toward processing natural gas from the Marcellus Shale…

The ethylene cracker plant would convert natural gas liquids into other, more profitable chemicals, which then go into everything from plastics to tires to antifreeze.

The bad news on refineries…

The U.S. has lost nearly 5 percent of its refining capacity in the past three months, as a handful of old refineries have shut down."

…two large refineries outside Philadelphia shut down: Sunoco's plant in Marcus Hook, Pa., and a ConocoPhillips plant in nearby Trainer, Pa. Together they accounted for about 20 percent of all gasoline produced in the Northeast."

Hovensa finished shutting down its refinery in St. Croix [U.S. Virgin Islands]. The plant processed 350,000 barrels of crude a day, and yet lost about $1.3 billion over the past three years, or roughly $1 million a day."

The reasons for shutting down the refineries:

The U.S. refining industry is being split in two. On one hand are the older refineries, mostly on the East Coast, which are set up to handle only the higher quality Brent "sweet" crude-a benchmark of oil that comes from a blend of 15 oil fields in the North Sea. Brent is easier to refine, since it has a low sulfur content, though it's gotten considerably more expensive recently.

The Hovensa facility, for example, in addition to being forced to use the more expensive imported crude oil, was also using petroleum to power the refinery itself, while many of its stateside competitors process the cheaper West Texas Intermediate and use natural gas to power their facilities. Similarly, the shuttering Pennsylvania refineries don't have access to the cheaper West Texas Intermediate and are dependent on imported oil.

One of the unique ideas addressing the NIMBY (not in my backyard) mentality was the proposal put forth to convert decommissioned military installations into refineries.

From military bases to oil refineries By The Washington TimesThursday, April 28, 2005

In a speech Wednesday at the National Small Business Conference in Washington, President Bush proffered the idea of converting closed military bases into oil refineries. He promised to "direct federal agencies to work with states" to spur refinery-building and "to simplify the permitting process for such construction.

2008 Dan Burton, Indiana 5th District (Republican)

Provisions of Dan Burton's Energy Plan (HR6544): Refining Capacity

Increases refining capacity by allowing the president to designate old, unused military bases for refining production.

Encourage new refinery construction by requiring IRS to take action to allow tax exempt bonds to be used for construction of certain refineries, and make federal lands available for refinery construction.

STARK OPPOSES BUSH PLAN TO CONVERT CLOSED MILITARY BASES TO REFINERIES

Thursday, April 28, 2005

WASHINGTON, DC -- Today, Rep. Pete Stark (D-Fremont) announced his strong opposition to President Bush's plan to build oil refineries on closed military bases, which the President announced yesterday and is expected to address during his press conference this evening.

The President has never seen an environmental problem he thought couldn't be solved by covering it over with an oil rig or a refinery. Unfortunately, refineries don't reduce our dependence on foreign oil and they won't erase this administration's failure to decontaminate closed military bases," said Stark.

Stark represents the former Alameda Naval Air Station in Alameda, Calif. The 2,479 acre site was closed for military use in 1997 but still lies largely unoccupied because of significant contamination problems.

This leads to the next issue…

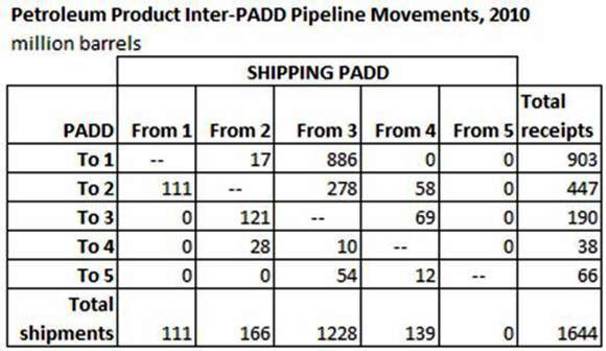

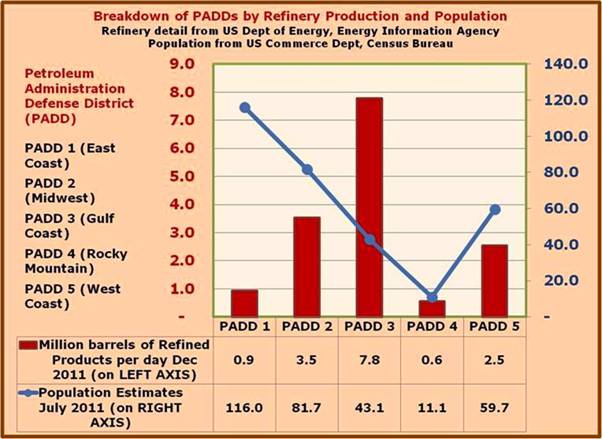

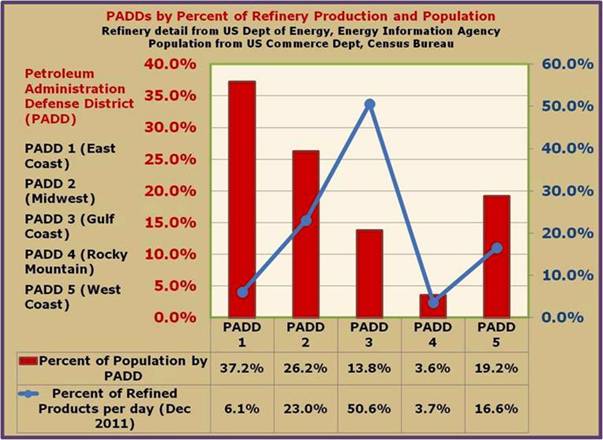

4) Most of the refining operations in the U.S. are NOT necessarily where the populations they serve are located.

Dating from World War Two, the U.S. is divided up into what are referred to as Petroleum Administration Defense Districts or PADDs. In mobilizing for a wartime economy, established to help efficiently and expediently allocate petroleum products (primarily gasoline and distillates - diesel fuel).

PADD's were delineated during World War II to facilitate oil allocation.

- PADD 1 (East Coast):

- PADD 1A (New England): Connecticut, Maine, Massachusetts, New Hampshire, Rhode Island, Vermont.

- PADD 1B (Central Atlantic): Delaware, District of Columbia, Maryland, New Jersey, New York, Pennsylvania.

- PADD 1C (Lower Atlantic): Florida, Georgia, North Carolina, South Carolina, Virginia, West Virginia.

- PADD 2 (Midwest): Illinois, Indiana, Iowa, Kansas, Kentucky, Michigan, Minnesota, Missouri, Nebraska, North Dakota, Ohio, Oklahoma, South Dakota, Tennessee, Wisconsin.

- PADD 3 (Gulf Coast): Alabama, Arkansas, Louisiana, Mississippi, New Mexico, Texas.

- PADD 4 (Rocky Mountain): Colorado, Idaho, Montana, Utah, Wyoming.

- PADD 5 (West Coast): Alaska (North Slope and Other Mainland), Arizona, California, Hawaii, Nevada, Oregon, Washington.

A big topic in the news of late has to do with the Keystone XL Pipeline, which targets a pipeline running from the Athabasca Tar Sands in Alberta (producing 1.3 million barrels of oil per day), in a more direct Southeastern route to Kansas (an environmental snag has to do with running the pipeline through Nebraska and concerns over the potential leaks in the Ogalalla aquifer), on to Cushing, Oklahoma, and then further south to the refineries on the Gulf Coast. While expanding pipeline capacity is quite helpful and meaningful, it equates to 500,000 to 700,000 more barrels of crude oil a day making its way to the refineries, wouldn't it also be helpful for that crude oil to make its way further east, where there is a huge dependence on imported, more expensive oil?

Think about it…if the expansion in the crude oil production in the west could be redirected to points east (in lieu of or in addition to the Keystone XL initiative, it would help reduce the shortage of and hopefully reverse the shuttering of refineries dependent on the more expensive (and sweeter - easier to refine) imported Brent Crude.

Why the U.S. Desperately Needs an East - West Oil Pipelineby Keith Schaefer on March 21, 2012

Reductions in Northeast Refining Activity: Potential Implications for Petroleum Product Markets

U.S. Department of Energy, Energy Information Administration

Release date: December 23, 2011

Reduction in refining activity in the Northeast, as reflected in recently announced plans to idle over 50% of the regional refining capacity, is likely to impact supplies of petroleum products.

Three southeastern Pennsylvania refineries that comprise over 50% of the total refining capacity in the Northeast (Central Atlantic and New England States) have recently been proposed for sale. Two of these refineries have already been idled.

Refineries on the East Coast mainly serve the Northeast, supplying approximately 40% of Northeast gasoline sales and 60% of distillate sales in 2010. About half this supply came from three refineries expected to be offline.

In 2010, the three refineries at issue combined to produce 315,000 bbl/d of gasoline, 194,000 bbl/d of distillate and 41,000 bbl/d of jet fuel.

When we consider the many issues confronting us regarding our energy needs in general, we have to keep in mind that there are many competing interests involved that are not necessarily in agreement with the greater good of the consumer - and always remember that we are all consumers. As we move forward in our analysis, we return to this recurring theme: without plentiful and cheap energy, an economic turnaround affording opportunity and access for all Americans is just not possible…

In the following graphs, we want to illustrate the problem facing consumers from on two levels concerning petroleum production, both stemming from the consolidation (make that reconsolidation…remember Standard Oil - John D. Rockefeller) of the domestic oil industry from primarily the 1990s and concluding around 2002. Both the crude oil and the refined petroleum products experienced massive consolidation/concentration.

U.S. Government Accountability Office

July 7, 2004

ENERGY MARKETS - Mergers and Many Other Factors Affect

U.S. Gasoline Markets

One of the many factors that can impact gasoline prices is mergers within the U.S. petroleum industry. Over 2,600 such mergers have occurred since the 1990s. The majority occurred later in the period, most frequently among firms involved in exploration and production. Industry officials cited various reasons for the mergers, particularly the need for increased efficiency and cost savings. Economic literature also suggests that firms sometimes merge to enhance their ability to control prices.

Two major changes have occurred in U.S. gasoline marketing related to mergers, according to industry officials. First, the availability of generic gasoline, which is generally priced lower than branded gasoline, has decreased substantially. Second, refiners now prefer to deal with large distributors and retailers, which has motivated further consolidation in distributor and retail markets.