2015 Volume Issue 1

March 8, 2015

For a downloadable version, click the following:

…a bit more compressed version of the PDF

SHADES OF THE GREAT DEPRESSION OF THE 1930s: a race to less than zero [interest rates] with central bank easings

The foreign exchange markets are beginning to look like a battlefield wherein is occurring a war of competitive depreciation involving a number of national and regional currencies. Can a Smoot-Hawley type tariff war be far behind? Perhaps it has already begun. The European Central Bank pressured interest rates on deposits refinancing rates into negative territory in 2014.

Less than Zero

When Interest Rates go Negative

March 4, 2015

www.bloombergview.com/quicktake/negative-interest-rates

We are witnessing just the overture to such a war which began with a series of actions by central banks to depreciate their currencies and a return series of salvos by other nations retaliating to offset the initial actions.

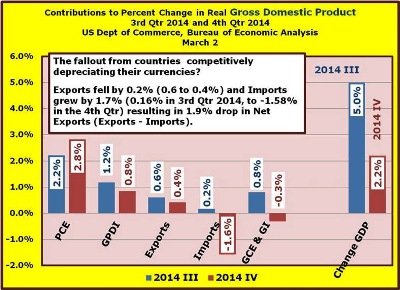

Collapsing GDP: 5% in Third Quarter 2014; 2.2% in the Fourth

Initial evidence of the impact in currency appreciation can be found in the most recent Gross Domestic Product data which in the case of the U.S. estimates the quarterly growth rate of real GDP which was reduced by around 2 percentage points. From the third quarter to the fourth quarter 2014, Net Exports (Exports – Imports) fell by 1.9%, going from 0.78% to -1.115%. With slowing economic growth rates and even recessions looming for some nations, can “Beggar Thy Neighbor” become an increasing practice by them? Time will tell if history is repeating itself.

So what’s the Downside to a Strong Dollar?

For those not well versed in this area, if the U.S. Dollar appreciates (grows stronger) against the currencies of its trading partners’ (the same as saying that if the currencies of its trading partners depreciates against the Dollar, since they are reciprocals of each other), U.S. imports of goods and services will tend to increase because the Dollar price of those foreign goods and services are now cheaper than before the change in the exchange rate. At the same time, U.S. goods and services become more expensive to our trading partners since the foreign currency prices of U.S. goods and services have increased.

Recall that imports tend to depress the domestic level of economic activity of the importing nation while exports tend to raise the level of economic activity of the exporting nation. One of the four components of a nation’s Aggregate Demand (AD) is Net Exports of Goods or merchandise and services (Exports minus Imports).

Beggar thy Neighbor: Depreciation is Underway – a Tale of Quantitative Easing the World Over

In the 1930s, such tactics as depreciating one’s currency and raising import tariffs were referred to as “Beggar thy Neighbor” policies. It is a major reason why international trade virtually came to a halt in the early 1930s and helped lengthen the Depression, providing ammunition for extremist movements such as fascism and communism.

There is no doubt that a number of regions have either begun to experience economic weakness or are continuing in the doldrums. Added to this growing problem was what some might call a spirit of optimism. But I call it wishful thinking at best or jawboning at worst by various public officials; including high ranking officials of the Federal Reserve System, that the worst was over and the FED could end its policy of Quantitative Easing. Concurrently, high ranking officials of the central banks of other nations including the European Union’s central bank (ECB) continue to pursue their own policies of quantitative easing.

The effect of the latest quantitative easing ending (QEs) in the U.S. while beginning in many other regions of the world, meant that downward pressure on interest rates would occur in those nations adopting QE and at best, interest rates holding steady if not beginning an ascending pattern in the U.S. This tends to cause a flight to the Dollar because of higher relative yields as well as a flight to quality and the U.S. Dollar. The net result is the appreciation of the Dollar brought on by bolder and more retaliatory policies by other countries moving further down the path toward “Beggaring Thy Neighbor”.

Strong Dollar Advocates Beware

Those advocating a “strong” Dollar, beware of the coming “Ides of March”. A strong Dollar or the appreciation of the Dollar leads to a rise in U.S. imports and a fall in U.S. exports. An existing trade surplus in the U.S. Trade Balance will shrink or an existing Trade Deficit will increase. Either reduces the aggregate demand (AD) of the U.S. economy and tends to reduce the growth rate of real GDP. As the saying goes, be careful of what you wish for, as your wish may be granted.

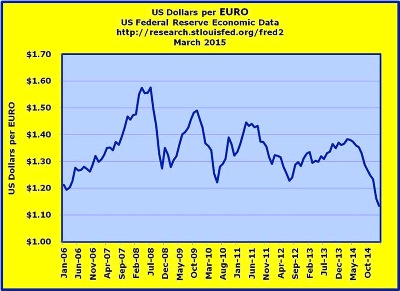

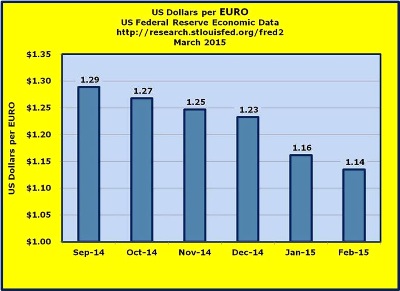

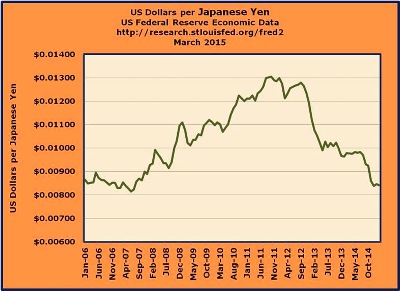

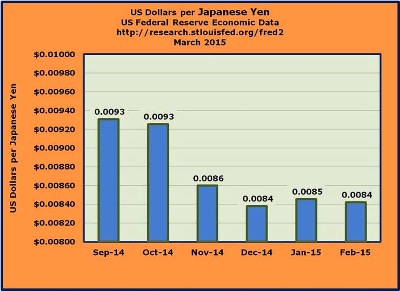

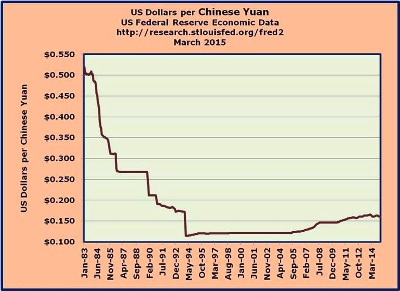

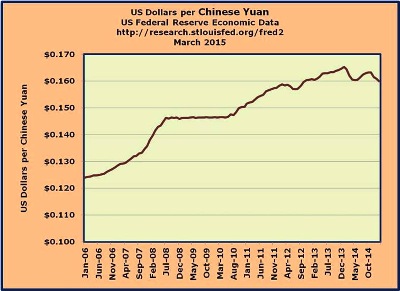

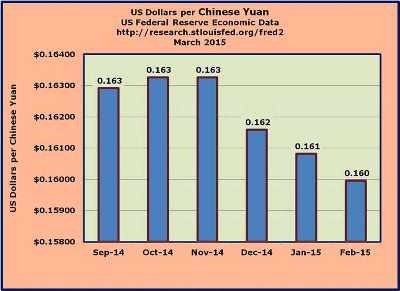

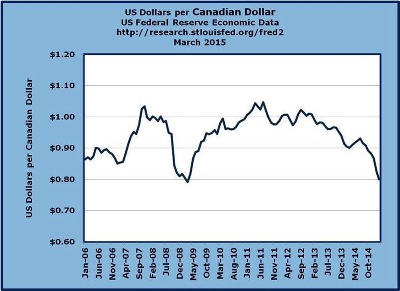

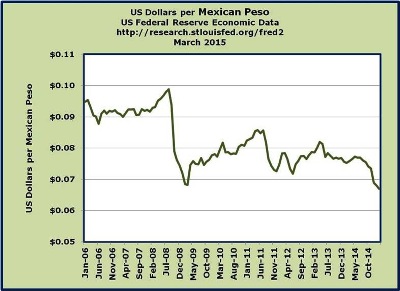

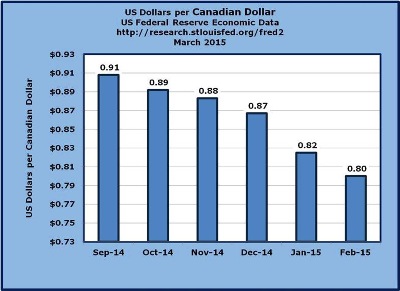

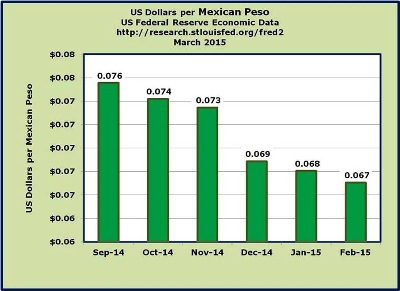

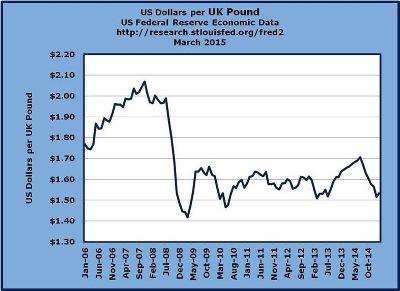

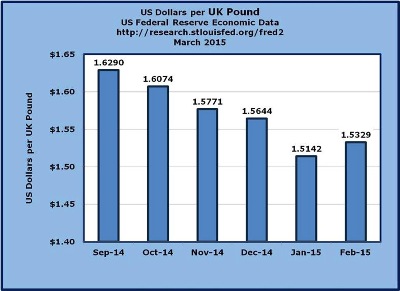

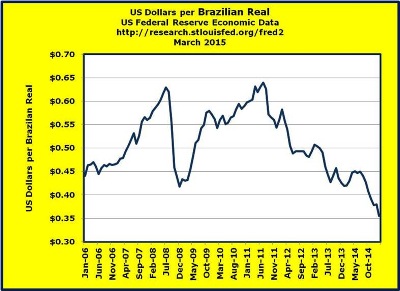

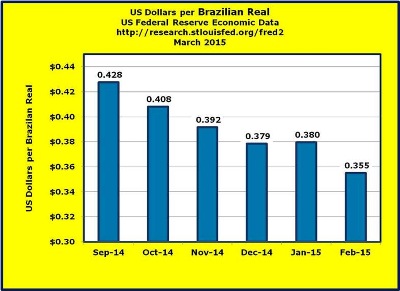

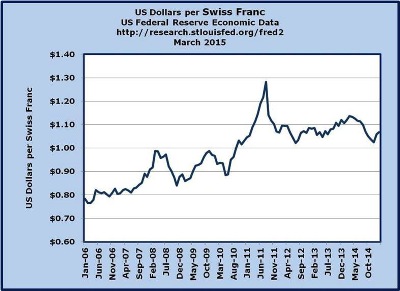

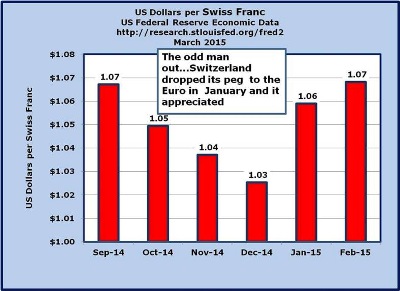

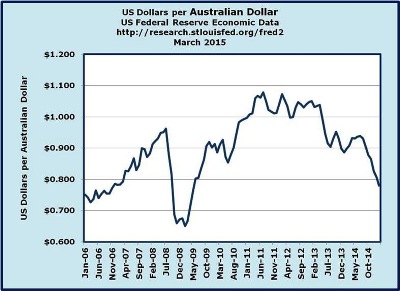

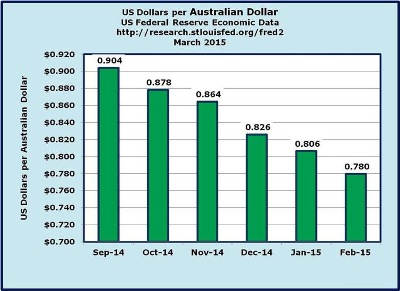

Graphs of the Ongoing Fallout from Currency Depreciation

In the following graphs we will depict various foreign currency relationships with the U.S. Dollar.

The first will be a historical look going back to 2006 and the second is a look at the last six months (October 2014 through February 2015). For the Chinese Yuan, we have a chart going back to the 1980s as well depicting the deliberate plan to devalue the Yuan versus the U.S. Dollar…witness the Chinese miracle (not unlike the Japanese and German miracles that preceded it)

THE CHINESE MIRACLE; OR IS IT REALLY A U.S. POLICY DEBACLE?

February 3, 2012

www.econnewsletter.com/feb032012.html

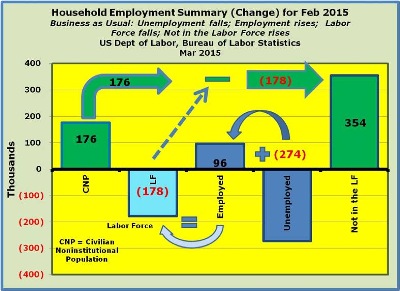

Next up on the block --- February Employment Report: 295,000 added in Payroll Report (Establishment Survey); while in the Household Survey, a whopping 354,000 moved to the sidelines.

We'll have our next newsletter out shortly to address this issue.

The word on the Street: an awesome Jobs Report, which will provide cover for the FED to raise the target on Federal Funds from the current 0.0 - 0.25% rate.

Is such a move really warranted given the appreciating dollar and a much less than awesome Employment Report?

176,000 people added to the Civilian Noninstitutional Population (CNP) (16+ years, not in military, prison, or otherwise in institutions)

The CNP = the Labor Force (those employed + those unemployed, actively seeking employment) and those Not in the Labor Force.

Labor Force dropped by 178,000 as the net effect of falling unemployment (274,000) did not translate into adequate jobs (96,000 added to employed).

The NET effect for the month was that 176,000 adds to the CNP and 178,00 dropped from the Labor Force leaves us with an additional 354,000 people on the sidelines ---- 354,000 Not in the Labor Force!

We'll delve more into this in the next newsletter article.