2015 Volume Issue 10

July 31, 2015

For a downloadable version, click the following:

…a bit more compressed version of the PDF

A Tale of Two Prices: a discussion about international trade and foreign exchange

To paraphrase Charles Dickens, ‘We face a tale of two prices’. It is one of the best of all times in international trade discussions but one of the worst of all times in foreign exchange markets.

In most cases, transactions in international trade and investment involve two prices, not just one. The first is the effective price of goods and services in the domestic or home country; and the second, includes the financial securities acquired in another nation, accounting for not only the domestic price but also the price of acquiring the currency of the nation in which the goods, services and financial assets are purchased. The second price, acquiring the currency of the nation in question, is called the exchange rate. Discussions involving the issue of free and fair trade must consider both prices; the domestic price of the goods and services, and the foreign exchange rate, or they are doomed to futility.

First, a little History: Banding together in Common Currency Blocs

In a few cases, this second price, the foreign exchange rate, can be eliminated if a common currency is adopted such as the Euro, the currency of the European Union, for example. Nations within the currency bloc, such as the Eurozone eliminate the second price or exchange rate when international transactions within the zone occur. If the international transactions involve nations outside of the currency zone, then effective prices must include the exchange rate as well.

If a nation such as the United Kingdom opts out of accepting the common currency, the Euro in this case, the second price or foreign exchange rate must be considered. The U.K. Pound price of the Euro must be taken into consideration since the British have refused to give up the Pound as their currency and replace it with the Euro.

Why, you may ask, did they follow that course and still do so? As we have examined in earlier newsletters on this website, it really is a question of monetary sovereignty. Giving up a national currency and accepting a common currency with other nations, will eliminate much of a nation’s monetary sovereignty.

We can see this clearly in the U.S. even more clearly than in Europe. The Federal Reserve System is our central bank and determines the nation’s monetary policy (Federal Open Market Committee or FOMC). The fifty states have no independent monetary policy in this macroeconomic sense of the term.

Enter Bretton Woods at the end of WWII

Exchange rate systems such as the Bretton Woods Fixed Exchange Rate System, adopted just after WWII, is an example of the importance of including exchange rates in attempting to foster greater international trade as was the much heralded and greatly misunderstood Gold Standard of which the Bretton Woods fixed exchange rate system is a first cousin, so to speak.

JELLIN’ WITH YELLEN: The asymmetrical power of monetary policyJuly 13, 2014

www.econnewsletter.com/jul132014.html

In its best years, it came to an end when some nations felt they needed to take back their monetary sovereignty and left the system. Since the U.S version under FDR, the U.S. never tied the money stock to the gold stock; it was not really a true gold standard. When gold began to flow out, it was effectively abandoned. The IMF Bretton Woods fixed exchange rate system after WWII was linked to gold via the U.S. Dollar, but frequent and significant devaluations and revaluations made it more of a floating rate system than a true gold standard.

Again, as part of aiding the post WWII recovery, the U S. Dollar was deliberately over-valued and resulted in significant international trade deficits in the U.S Balance of Payments. This was done to help rebuild the nations which were most physically and economically damaged during the WWII. Recall that the failure to rebuild the nations with the greatest damage caused during WW I was a major factor leading very quickly to WWII.

The Bretton Woods fixed exchange system’s problems gradually increased and in effect some nations felt they needed to take back their monetary sovereignty and left the system. To avoid the total collapse of the system, many nations were allowed to devalue or revalue upward their currencies in relation to the U.S. Dollar. The system’s final demise after many currency valuation changes finally occurred. When the U. S. found it difficult to maintain it central position in the system while at the same time constructing a “Great Society” as the President Lyndon Banes Johnson years have been called, the system was abandoned and foreign exchange markets returned to a more or less floating rate structure.

In the Great Depression years, the U.S version of a gold standard was adopted under influence of FDR. But the U.S. never tied the money stock to the gold stock so it was not really a true full blown gold standard. When Gold began to flow out of the U.S., the Dollar was effectively devalued in terms of gold and the system was eventually abandoned.

The IMF Bretton Woods fixed exchange rate system after WWII was linked to gold via the U.S. Dollar, but, as pointed out earlier in this article, frequent and significant devaluations and revaluations made it more of a floating rate system than a true gold standard.

THE CURRENT CACOPHONY OF MONETARY POLICIES THROUGHOUT THE MAJOR NATIONS

July 4, 2013

www.econnewsletter.com/jul042013.html

History shows that whenever a nation faces serious problems, such as winning a war or running out of international reserves (part of which is gold), or continuing domestic policies that seem incompatible with other nations’ goals, the often restrictive fixed exchange rate systems (including a single currency system such as that based on the Euro) have frequently led to abandonment of such standards. This has been the case EVEN IF THERE WAS A GOLD STANDARD! The U.S. did so under the ‘watered down gold standard’ brought back by FDR. Over the years, even the link of the gold backing to the currency portion of M-1 money was gradually reduced. After WWII when the U.S. sponsored a form of a gold exchange standard referred to as the Bretton Woods IMF Fixed Exchange Rate System and when the U.S. began to experience significant balance of payments deficits, the gold price of the Dollar was altered (increased, i.e., the Dollar was devalued which is a form of depreciation in respect to gold) to avoid austerity policies to eliminate those deficits causing the outflow of gold.

When the Bretton Woods system collapsed in the early 1970s, we reverted back to what is called a floating rate system, in much of the world. It would be better called a dirty float for some nations like Mainland China. To prop up a failed economic system, they adopted a form of mercantilism by intervening in the foreign exchange markets and sold Yuan in order to depreciate or cheapen their currency. This effectively lowered the price of their goods and services to other nations while at the same time increasing the price of imports from other nations. This Balance of Trade surplus stimulated their lackluster economy at the expense of other nations who ran trade surpluses. While they claim they no longer cheapen their currency, they certainly are maintaining the already achieved cheapness of the Yuan in order to continue the propping up of their weak economy.

Enter the Trans-Pacific Partnership Trade Agreement or TPP

en.wikipedia.org/wiki/Trans-Pacific_Partnership

The Trans-Pacific Partnership involves Pacific Rim trading partners in negotiations to reduce or eliminate trade restrictions (tariffs, quotas, etc.) When you consider the fact that the agreement focuses solely on trade, ignoring the exchange rate relationship, it becomes a cautionary tale. Free trade is, in general terms, very beneficial for the participating players (why else would they partake?), but in the absence of addressing the influencing of currency exchange rates, it becomes much more complicated.

So again, do not get too excited over trade negotiations unless they incorporate some control over foreign exchange rates. “Fooled once, shame on you, fooled twice, shame on me.”

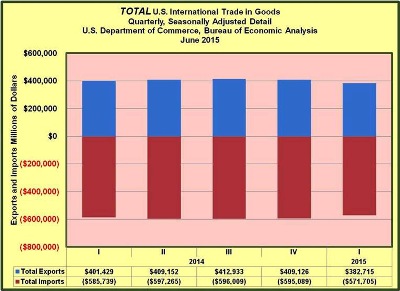

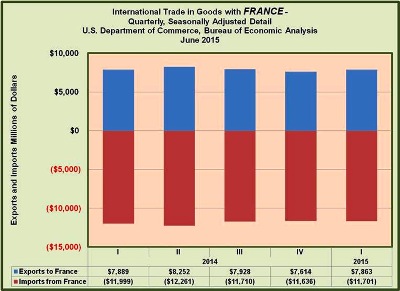

As it stands right now, the U.S. dollar has pretty much appreciated across the board.

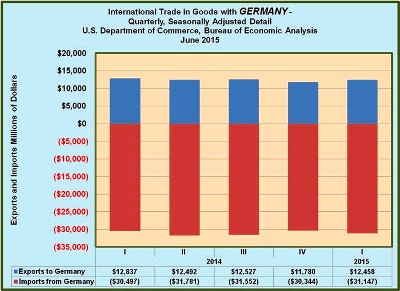

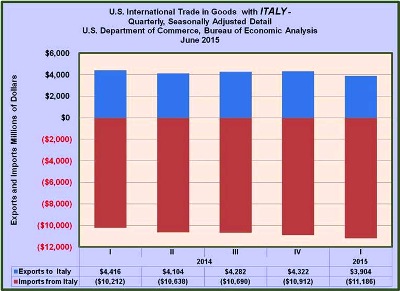

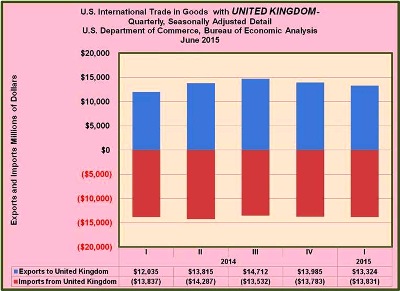

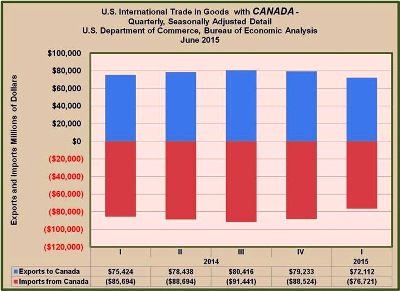

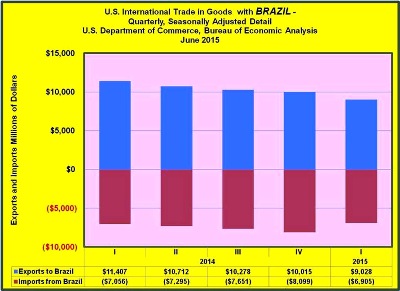

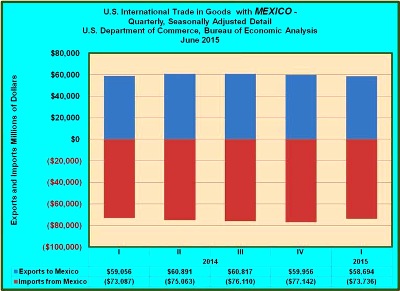

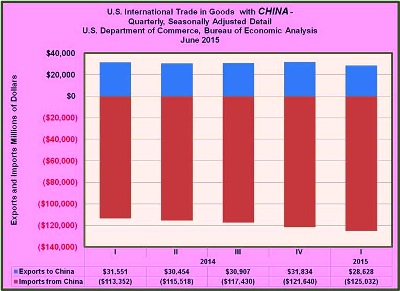

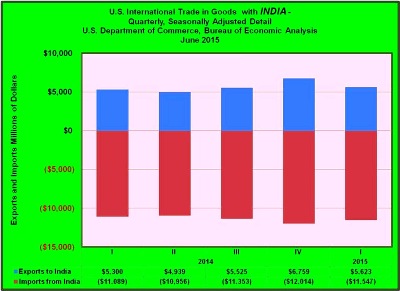

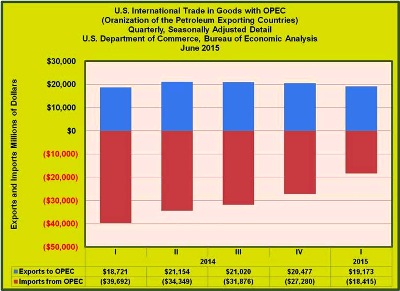

The Current Lay of the Land with Exchange Rates and Trade (Merchandise or Goods) Balances

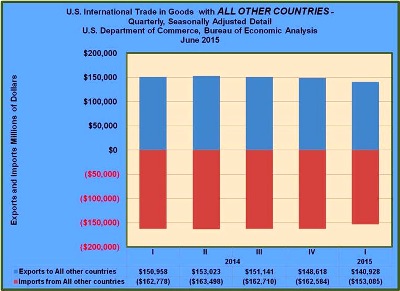

The following graphically explains the current situation in terms of exchange rates and balance of payments (goods or merchandise, in this presentation)…sometimes, pictures really do help clarify.

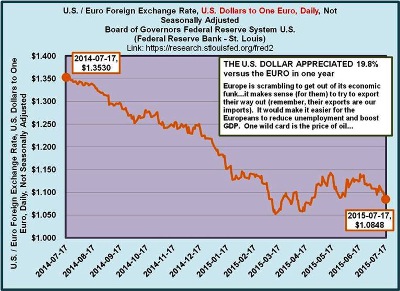

THE U.S. DOLLAR APPRECIATED 19.8% versus the EURO in one year

Europe is scrambling to get out of its economic funk…it makes sense (for them) to try to export their way out (remember, their exports are our imports). It would make it easier for the Europeans to reduce unemployment and boost GDP. One wild card is the price of oil…

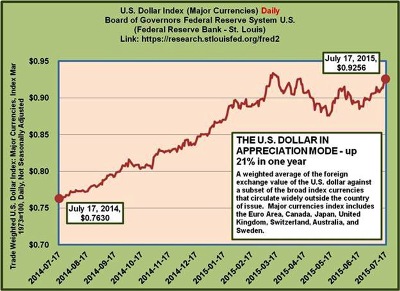

THE U.S. DOLLAR IN APPRECIATION MODE - up 21% in one year in the Major Currencies Index

A weighted average of the foreign exchange value of the U.S. dollar against a subset of the broad index currencies that circulate widely outside the country of issue. Major currencies index includes the Euro Area, Canada, Japan, United Kingdom, Switzerland, Australia, and Sweden.

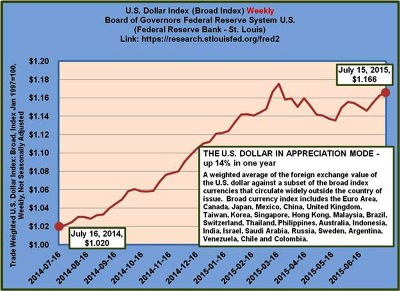

THE U.S. DOLLAR IN APPRECIATION MODE - up 14% in one year in the Broad Index of Currencies

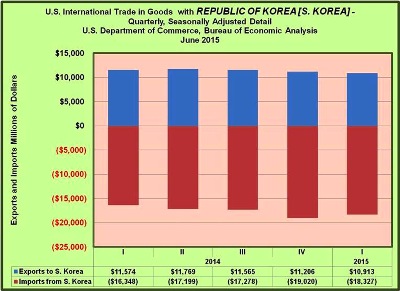

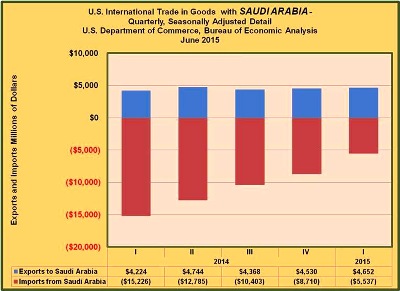

A weighted average of the foreign exchange value of the U.S. dollar against a subset of the broad index currencies that circulate widely outside the country of issue. Broad currency index includes the Euro Area, Canada, Japan, Mexico, China, United Kingdom, Taiwan, Korea, Singapore, Hong Kong, Malaysia, Brazil, Switzerland, Thailand, Philippines, Australia, Indonesia, India, Israel, Saudi Arabia, Russia, Sweden, Argentina, Venezuela, Chile and Colombia.

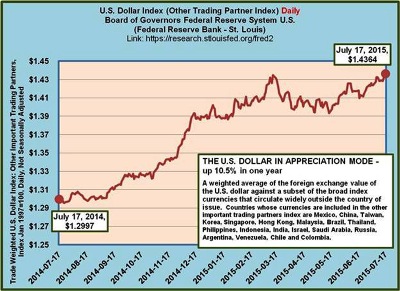

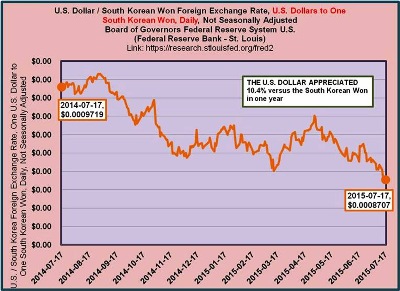

THE U.S. DOLLAR IN APPRECIATION MODE - up 10.5% in one year in the ‘Other Important Trading Partners’ Index of Currencies

A weighted average of the foreign exchange value of the U.S. dollar against a subset of the broad index currencies that circulate widely outside the country of issue. Countries whose currencies are included in the other important trading partners index are Mexico, China, Taiwan, Korea, Singapore, Hong Kong, Malaysia, Brazil, Thailand, Philippines, Indonesia, India, Israel, Saudi Arabia, Russia, Argentina, Venezuela, Chile and Colombia.

THE U.S. DOLLAR APPRECIATED 19.8% versus the EURO in one year

Europe is scrambling to get out of its economic funk…it makes sense (for them) to try to export their way out (remember, their exports are our imports). It would make it easier for the Europeans to reduce unemployment and boost GDP. One wild card is the price of oil…

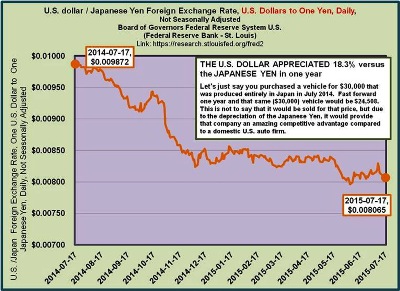

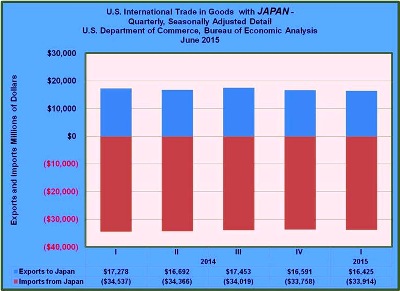

THE U.S. DOLLAR APPRECIATED 18.3% versus the JAPANESE YEN in one year

Let's just say you purchased a vehicle for $30,000 that was produced entirely in Japan in July 2014. Fast forward one year and that same ($30,000) vehicle would be $24,508. This is not to say that it would be sold for that price, but due to the depreciation of the Japanese Yen, it would provide that company an amazing competitive advantage compared to a domestic U.S. auto firm.

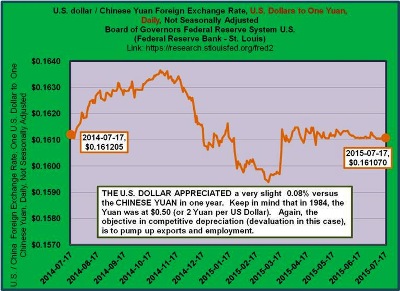

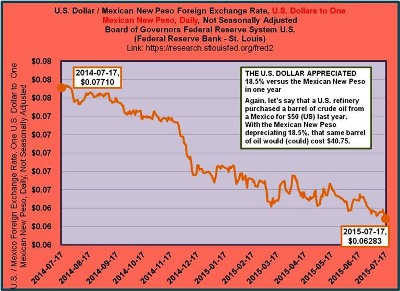

THE U.S. DOLLAR APPRECIATED a very slight 0.08% versus the CHINESE YUAN in one year.

Keep in mind that in 1984, the Yuan was at $0.50 (or 2 Yuan per US Dollar). Again, the objective in competitive depreciation (devaluation in this case), is to pump up exports and employment.

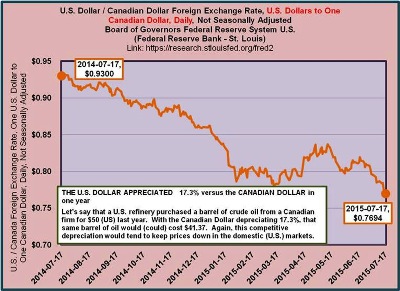

THE U.S. DOLLAR APPRECIATED 17.3% versus the CANADIAN DOLLAR in one year

Let's say that a U.S. refinery purchased a barrel of crude oil from a Canadian firm for $50 (US) last year. With the Canadian Dollar depreciating 17.3%, that same barrel of oil would (could) cost $41.37. Again, this competitive depreciation would tend to keep prices down in the domestic (U.S.) markets

Wrap-up

While competitive currency depreciation is certainly going on, and it will certainly continue to amplify the trade deficit for the foreseeable future.

The Laffer Curve and the J-Curve are Analytically like Two Peas in a Pod

www.econnewsletter.com/dec022010.html

December 2, 2010

You might want to take a look at this earlier article regarding the J-Curve and the association between exchange rates and trade. It’s not simply a matter of good or bad, where one person likes a strong dollar, while another prefers a weaker dollar. It really comes down to the economic consequences of both, and whether or not we want to accommodate the actions of other countries or oppose them (or something in between).

On a promising note, increasing domestic production of crude oil and natural gas has certainly helped offset what would be an even larger trade deficit.