2015 Volume Issue 12

September 30, 2015

For a downloadable version, click the following:

…a bit more compressed version of the PDF

A GROWING ANGST: WILL HISTORY SOON REPEAT ITSELF AT COMING FOMC MEETINGS IN THE NEAR FUTURE?

Treasury Yields at Zero Highlight Concerns Over RiskSeptember 22, 2014

A $15 billion sale of U.S. government debt attracted record demand, even though the securities, which mature in a month, were sold with an interest rate of zero.

Perhaps that has something to do with the FOMC (Federal Open Market Committee) meeting on October 27-28.

…the Drums are beating for the FED to drive up Rates

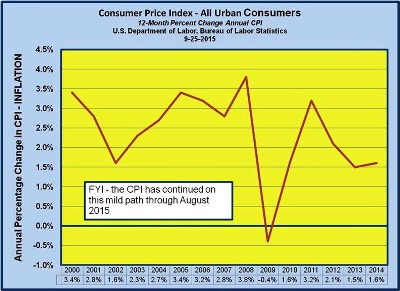

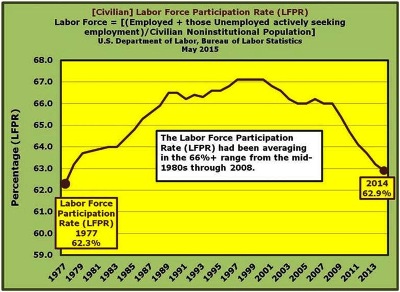

While many, most likely those with vested interests in having higher interest rates, whimpered and whined over the FED’s policy decision at the last FOMC meeting to stay the course of low interest rates a while longer, many nations and their financial markets breathed a sigh of relief. Nearly all had been convinced that the FED of the U.S. of A. would move to a policy of putting upward pressure on interest rates to preempt a boogey man of a much touted but non-existent vigorous economic recovery, which they were beginning to believe was occurring in the U.S. Given the apparent low inflation rate and the persistently low Labor Force Participation Rate, etc., an onslaught of a dangerously rapid economic recovery seems, in a reverse-like manner, ‘visions of sugar plums dancing’ in the FOMC members’ heads.

In this newsletter article we will examine the effects of a policy shift to one of constraint and away from one of monetary ease. The reader is left to determine whether such a policy shift is one of wisdom or one of folly. There are many possible repercussions prompted by a shift to a policy of constraint to preempt a runaway economic recovery. There is this lingering fear in the shadows that has as of yet failed to enter the limelight in the various FED meetings and conferences.

Coverage in the News Media – at Home and Abroad

It is hard for the American public to feel the angst building in financial markets around the world since, with a few exceptions, analysts on American cable and network stations are either incapable of analyzing the economic and financial problems of other nations around the World or are not inclined to cover the international scene for other reasons. We suggest that you tune to the BBC World News www.bbc.com/news/business-34286230 and you will gain an appreciation for the anxiety developing in financial markets around the World.

As past newsletters on this web site have discussed, The FED (Federal Reserve System, the central bank of the U.S. of A. and especially since the reform of the FED in 1934, its policy making committee, the FOMC or Federal Open Market Committee) has been accused by many economic historians, of extending the Great Depression by several more years by shifting to a tight monetary policy dooming any significant recovery prior to post WWII..

What should/will the FED* do on the monetary policy front?

September 11, 2015

www.econnewsletter.com/sep112015.html

As we have pointed out on many occasions on this website over the past 13 years, the power of the FED to influence the economy is NOT symmetrical. It has tremendous power to constrain the economy by making credit more scarce and expensive, but is virtually helpless if economic stimulus is needed.

WHAT IS BEHIND THE FEDERAL RESERVE SYSTEM’S LATEST CAUTIONARY MONETARY POLICY ACTION?

Jan 2, 2014

www.econnewsletter.com/jan022014.html

The FED is pondering the weaning off of its support of the U.S. Government and Mortgage Backed Securities segments of the financial markets. The enormous rise in the Federal Government’s debt would have led to a significant surge in what is termed a ‘Crowding Out’ of funding for private sector spending, especially in the form of very high interest rates. The resulting rise in the cost of capital despite the recession would have led to further difficulties in the business investment, housing and consumer durables segments of aggregate demand and weakened farther an already floundering economy.

Once again, the asymmetry of the FED’s ability to alter economic behavior has manifested itself. While possessing enormous power to slow down the level of economic activity, it is, as the often used expression of ‘Pushing on a Limp String’ implies, nearly powerless to speed up the level of economic activity. The last six years or so, give more proof of the asymmetry in the power of the FED’s monetary policies to change the outcome of the economy’s behavior.

The FED has had an Accommodative Stance since late 2007

What the FED can do is what it has done and has continued to do since the most recent financial crisis began around 2007/08, is to put downward pressure on interest rates so that if a recovery begins, it will not be stalled by rising interest rates and an increasing scarcity of credit.

The FED’s monetary policy affects many markets, both here and abroad. Many analysts argue that the low interest rates have driven some investors to the stock market for higher yields, a type of substitution effect at work. This would account for the upward drift in stock market averages despite an anemic economic recovery at best.

The Impact of a Change in the FED’s Accommodative Policy

When interest rates begin to rise, the talk of its negative impact on business investment in new capital goods will return quickly. Capital budgeting theory tells us that the decision to invest or not to invest relates chiefly to the relationship of the expected rate of return on the proposed investment and the current weighted average cost of capital to finance that new investment. For a given schedule of proposed investments, as interest rates rise and hence the cost of capital rises, an increase volume of proposed investment projects are NO-GOS and rejected. At lower costs of capital some would have been undertaken. This is often cited as a major linkage in the FED’s ability to constrain an excessive growth rate of economic activity.

A related argument is that current low rates of interest reduce saving. The Keynesian tradition has always been that savings is primarily a function of the level on income and production (average and marginal propensities to save) and less so a function of interest rates. The argument is that savings is relatively inelastic in respect to interest rates. The data over similar periods when interest rates rose, also shows that the interest rates charged by financial institutions when creating credit (lending) rises more quickly than on such things as savings accounts. In other words, financial institutions such as commercial banks take advantage of periods in which interest rates are rising by increasing their margins.

An even more important effect of changing interest rates and changing monetary policies by the FED is the ever present inverse relationship between asset prices and interest rates. As interest rates fall, asset prices rise and as interest rise, asset prices fall. This occurs because the consensual required rate of return of investors is the required rate of return that discounts the consensual expected net flow of benefits from the investment in question to determine its discounted net present value or equilibrium market price of an asset. In the case of financial assets the benefits in question are the net cash flows generated by the financial asset.

In a less precise way, real assets, such as housing and commercial real estate, are also similarly affected and their market prices move inversely to the movement of interest rates, all else equal. In commercial real estate, the so-called cap rate is the rate of discount or required rate of return that is used in the discounting process to determine the assets discounted present value or maximum price that should be paid for the asset in question. Some real assets such as homes give the owner a stream of non-cash benefits that should also be related to the market price of housing for rational buyers. To determine the cash equivalent of the benefits of owning a house, the rent paid on similar housing could be used as a starting point. This means that as interest rates rise, so will other related rates rise such as the cap rates and total yield on stocks, thus putting downward pressure on real estate and stock prices, again, all else equal.

Thus a shift of FED policy to constraint resulting in and upward pressure on interest rates, will put downward pressure on the market prices of all existing assets, especially financial assets, and a NEGATIVE wealth effect will set in slowing any economic recovery. When the FED set out on its policy of Quantitative Easing several years back, the resulting fall in interest rates had a positive impact on EXISTING assets although other factors were changing that also influenced asset prices such as rising risk premiums and often overwhelmed the effects of the inverse relationship.

Further Impact resulting from FED Tightening – no more Conundrum

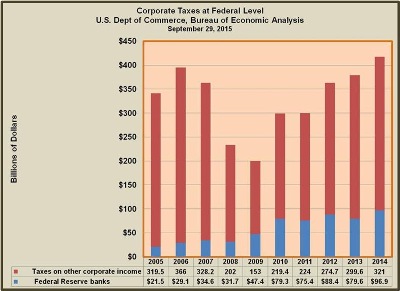

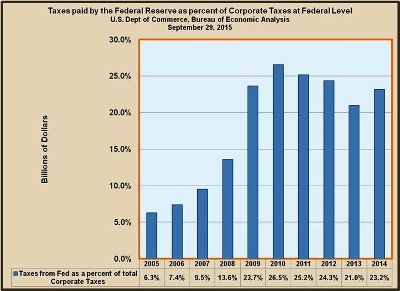

Another result of the FED’s tightening, though less significant than the more general effects of such a policy shift, is that as the FED sells of part of its portfolio in order to put upward pressure on interest rates, it will suffer losses since the market prices of existing debt securities it sells will be pressured downward. Note that the inverse relationship of asset prices to interest rates works in both directions. As asset prices rise, interest rates tend to fall, all else equal. This will also reduce its profits of the FED and hence reduce the resulting subsidy it gives the U.S. Treasury.

One favorable result of the FED’s nearly seven year period of monetary ease, is that it has acquired a much larger portfolio of debt securities than it has had in a long time. Remember that the FED’s major tool for monetary easing or tightening is the open market operation or the buying and selling of financial assets, nearly always debt securities. The use of the Discount Window and Discount Rate is and changes in legal reserve ratios are of much less importance since the Great Depression and the Second World when the U.S. Government marketable ballooned. Additionally, that portfolio is much more balanced in respect to maturities than it was before the financial crisis. This means that if the FED decides to put upward pressure on interest rates, no conundrum phenomenon will occur as happened during the Greenspan years at the FED.

The FED is now in a position to sell securities across the maturity spectrum and shift the yield curve upward in a more parallel pattern rather than just driving up interest rates at the short-term end of the maturity spectrum and having little or no effect on the med and long-term portions of the yield curve as was more the case in the Greenspan years. In short, they can successfully counter any market expectations to the contrary, an ability which the Greenspan FED did not have and was the essence of the Conundrum Phenomenon.

Here comes the Capital Inflow from Abroad – a Further Appreciating Dollar

If the fears of other nations materialize and increasing interest rates in the U.S. increase the capital flows into the U.S. from abroad, the Dollar will tend to appreciate even more so than has been occurring lately. U.S. Imports will become cheaper in Dollar terms and this will tend to increase our imports. As our Dollar appreciates, our exports will become more expensive t other nations’ currencies and will tend to fall, all else equal. The increase in our imports and decrease in our exports will worsen our Trade balance, already in deficit and from a macroeconomic perspective, depress the level of economic activity in the U.S. Remember that this would be on top of recent and current efforts by other nations, such as Mainland China, to increase their net exports to us by devaluing or pressuring their currencies to depreciate against the Dollar. Shades of the 1930s all over again with the return of ‘Beggar thy Neighbor’ policies; “Why stand we here idle.”

Many express concerns over the trouble developing and newly emerging nations are facing. Yet we do nothing to stop the ‘Brain Drain’ and the ‘Capital Drain’ from those nations. Talk is cheap. Greed is contagious.

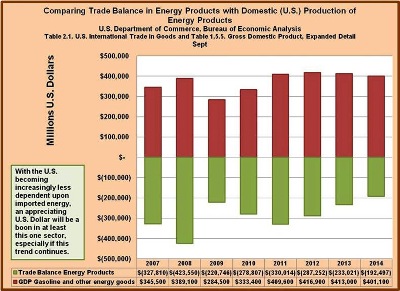

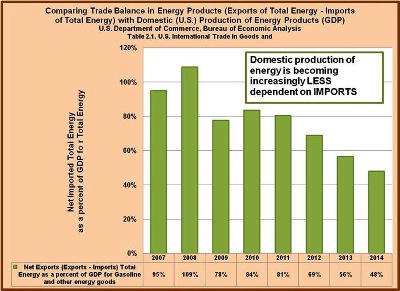

Will the Increase in Energy Production (Oil, Natural Gas, etc.) help offset or at least mitigate a widening Trade Deficit?

The rapid increase in the supply of crude and natural gas, especially due to the success of fracking, has altered the outlook for the Trade Balance, the price of energy, and the inflation rate. It is beginning to take some of the wind out of the sails of OPEC and lessen the problems associated with the use of the profits from these activities. Not only have the price of crude oil and its refined downstream products fallen significantly, but the U.S. will soon be energy independent on a net basis. This reduces inflationary pressures and lessens the Trade Deficit, a part of which was due to petroleum imports. The only downside of this is that it may provide an additional factor causing the appreciation of the U.S. Dollar.

U.S. Goods Exports Plummet as Dollar Rises, Commodity Prices Fall

(Exports of goods slid 3.2% in August to $123.09 billion)

Sept. 29, 2015 1:02 p.m. ET

www.wsj.com/articles/u-s-goods-exports-plummet-as-dollar-rises-commodity-prices-fall-1443546129

Exports of goods slid a seasonally adjusted 3.2% to $123.09 billion as overseas sales of industrial supplies—which includes oil—autos, consumer goods and foods all fell, according to the Commerce Department’s advance report on trade in goods. While the report’s historical data only reaches back to 2013, other figures suggest that exports dipped to the lowest level since mid-2011.

Imports, meanwhile, advanced 2.2% to $190.28 billion on a surge in consumer goods and a smaller rise in capital goods, widening the trade gap. The goods deficit expanded 13.6% to $67.19 billion last month.

The Aftermath in the Ramping up of Interest Rates

When the FED’s monetary policy finally shifts away from one of ease, an ironical twist is certain to occur. You may have wondered why the quieting down of the talk on the crisis facing pension funds of the defined benefit variety. Underfunding was the great fear. The discounted present value of future benefit payments was greater than the value of the funds’ assets. As interest rates fell, the prices of existing financial assets tended to rise for reasons discussed above. What appeared to be an exception were the mortgage backed assets which helped trigger the financial crisis several years ago. This was a case where the credit risk overwhelmed the price risk of this group of assets.

Falling interest rates caused the prices of the financial assets of defined benefit pension funds to increase and thus the value of the portfolio of these pension funds rose reducing the degree of underfunding. When interest rates begin to rise to more normal levels, the opposite will occur. The prices of existing financial assets will tend to fall (inverse relationship of interest rates to asset prices), all else equal, and the underfunding of defined benefit pension funds will worsen and the issue will begin to make the headlines once again. The retirement of the baby boomers, even though moderated by a rise in their labor force participation rate of the cohort over 60 years of age, will worsen the picture of these defined benefit pension funds and the issue of underfunding will return.

There are some other consequences of shifts in the levels of interest rates but enough of them have been mentioned to generate some serious thinking on the issue of the effects of a shift in the FED’s monetary policy.