August 8, 2011

…the following post was inspired by a current student who was curious about the effect (and efficacy) of further government intervention on a monetary (and fiscal) policy level, specifically the much bandied about QE 3 (Quantitative Easing 3), which would follow the recently completed QE 1 and QE 2 (www.econnewsletter.com/jul012011).

For a downloadable version, click the following:

WHAT IS LEFT FOR THE FEDERAL RESERVE POLICY MAKERS (FED) TO DO?

Could a QE 3 be meaningful?

There is an old adage about ‘closing the barn door after the horses have already bolted’. The Federal Reserve Board of Governors (FED) has been chasing the livestock in a desperate attempt to round them up. Damage control is always less efficient than is preventive maintenance. In past articles on this web site, we have quoted statements by FED officials, including Alan Greenspan, the former Chairman of the Federal Reserve Board of Governors and its policy making group, the Federal Open Market Committee (FOMC).

2011 Volume Issue 4

Economic Newsletter for the New Millennium

June 8, 2011

THE BALLAD OF ALAN GREENSPAN: TO DREAM THE IMPOSSIBLE DREAM

In Greenspan’s own words, “Our forecasts and hence policy are becoming increasingly driven by asset price changes. The steep rise in the ratio of household net worth to disposable income in the mid-1990s, after a half-century of stability, is a case in point. Although the ratio fell with the collapse of equity prices in 2000, it has rebounded noticeably over the past couple of years, reflecting the rise in the prices of equities and houses.”

Remarks by Chairman Alan Greenspan

Reflections on central banking

At a symposium sponsored by the Federal Reserve Bank of Kansas City, Jackson Hole, Wyoming

August 26, 2005

www.federalreserve.gov/Boarddocs/Speeches

He (Greenspan) was lamenting the presence of asset bubbles such as the housing market experienced a few years ago. It was only after the asset bubble of residential housing became spectacularly large that the FED pricked the bubble and it burst. The FED, through its FOMC, embarked on a steady path of continuously influencing short-term interest rates upward.

As we commented in an earlier article on this web site, this policy of putting continuous upward pressure on short-term interest rates would trigger rising monthly mortgage payments on the (Adjustable Rate Mortgages, or variable rate mortgages) ARMs as the mortgage interest rates were gradually re-priced upward due to rising short-term interest rates to which they were tied, such as the one year LIBOR rate and often even shorter terms. Along with much higher energy prices, thanks to the anti-trust authorities allowing the re-cartelization of the U.S. segment of the oil industry, the slack in household budgets was MORE than absorbed. This spelled trouble right here in River City.

Volume 2006: Issue 1---January 6, 2006 – yes, 2006!

The Killing Fields: Weak links in an otherwise strong economy

RISING MORTGAGE INTEREST RATES

In addition to the rising energy costs and insecurity in the labor markets, households are now facing an additional burden of rising interest rates, affecting their mortgages. As short-term rates are driven up by the Federal Reserve actions in the Federal Funds rates, it influences other short-term interest rates to rise as well.

In the area of variable rate mortgages (ARMs), the Fed’s actions are gradually triggering the adjustment clauses in these mortgages. This increases the monthly payments, reducing further the disposable income available to purchase other goods and services and also reduces the cushion protecting homeowners from defaulting on mortgages.

The ARMs were meant to protect lenders from accelerating inflation and the resulting fall in real interest rates on fixed rate mortgages. Unfortunately, when the FED pursues a [monetary] policy of monetary restraint, especially at the short term end of the yield curve, (www.econnewsletter.com/aug272007) the result is to effectively trigger rate increases in much the same manner as would occur if inflation was accelerating; all of this in spite of the fact that inflation remained relatively dormant.

Just the same, the carnage in the residential housing market due to the repricing of interest rates on ARMs, and on teaser rate mortgages was soon to begin. The FOMC drove up the Targeted Federal Funds Rate from 1.00% in June 2004 to 5.25% in June 2006 – where it remained until the fall of 2007. The ARMS, linked to the short-term end of the market, followed closely to the rising Effective Fed Funds Rate, driving up the affected homeowners’ monthly mortgage payments in ever higher increments.

In addition to this phenomenon, greedy investment bankers encouraged mortgage bankers to write household mortgages with teaser rates for the first year or two, with substantial increases built into those rates, NOT reliant on market rates reflecting the behavior of inflation (again, these teaser rate mortgages to high risk borrowers are an entirely different beast than are ARMs; they were marketing gimmicks, plain and simple).

The rating agencies went along with this practice and overrated the credit quality of the mortgage pools that included teaser rate mortgages. The increases in mortgage rates on both the teaser rate mortgages and the ARMS “were the straws that broke the camel’s back,” so to speak. Foreclosures exploded upward and housing prices collapsed, by 30% or more and in some places by 50% (or more). The real estate bubble burst. This must have made Greenspan and other officials happy, judging by the statement they were making about asset bubbles. You know the rest of the story and the miserable condition in which the U.S. economy is currently wallowing.

www.econnewsletter.com/sep242010

Financial Chaos

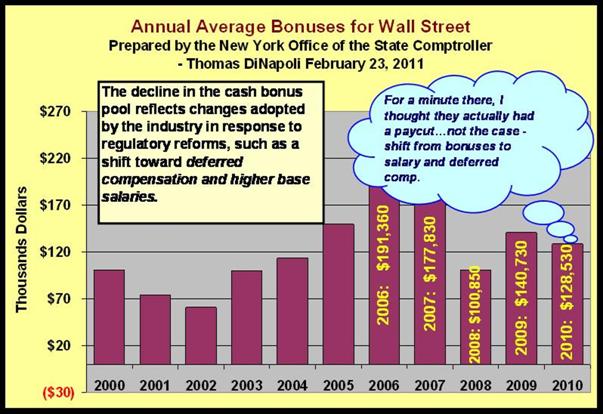

A glaring example of this is the investment banking industry. Literally tens of billions in commissions, bonuses, etc. were paid salesman, managers and partners even though some of their activities were a major cause of the recent and ongoing financial crisis and the recession that it helped to cause.

DiNapoli: Wall Street Bonuses Declined in 2010

Earnings Down from Record High, but Wall Street Has Second Best Year Ever

The FED had the power to adjust the percentage of down payments and the margin percentages on stock purchases to slow, if not stop their asset bubbles from occurring. The FED was loath to do so. Instead they flinched, for some unstated reason…and you know the rest of this sad story.

In an effort at damage control, the FED embarked upon QE 1 and 2. The economy continues to wallow in desperately high levels of unemployment, by the more realistic U-6 measure above 16%.

What is left for the FED to do?

They can continue to buy large amounts of U.S. Government securities as they have over the last few years. This could be “sterilized” by raising legal reserve requirement ratios as we have pointed out in other articles on this website.

THE LOCKED IN EFFECT: Complicating the FED’s (as in Federal Reserve) conduct of monetary policy

…Various Required Reserve Ratios over the years

Reserve Requirements: History, Current Practice, and Potential Reform

www.federalreserve.gov/monetarypolicy/0693lead.pdf

Alas, this would put upward pressure on lending interest rates by depositories, such as banks, to offset the negative impact on banks’ profits and thus their operating leverage. This in turn would negatively impact any recovery from our current economic malaise.

Remember that the FED can only increase the capacity (of depositories such as commercial banks) to create by creating new M-1 money in the form of checkable deposits and ‘lend them out’. Until it is profitable to do so, depositories will sit it out on the sideline and let the increased capacity sit idle as they are currently doing.

The FED could keep spitting legal reserves to depositories, but in terms of effectiveness, they have already, as the vernacular expression goes, ‘shot their wad’.

Could fiscal policy be used instead of monetary policy?

Macroeconomic theory of the Keynesian type has already promoted TRILLION DOLLAR (PLUS) INCREASES over each of the last three years and is slated to do the same for years into the future with dismal effects.

So, what about tax increases proposed by the Obama administrations as a solution to reducing deficits?

This is not only contrary to the Keynesian, neo-Keynesian theory but as Henry Morgenthau (Secretary of the Treasury under Franklin Delano Roosevelt or FDR and his long time friend and confidant) testified before Congress in 1939 (WHAT IS HAPPENING IN THE CRADLE OF DEMOCRACY?), tax increases followed by government spending and large deficits and all other measures take during the Great Depression were failures and even resulted in deeper double dip in 1937.

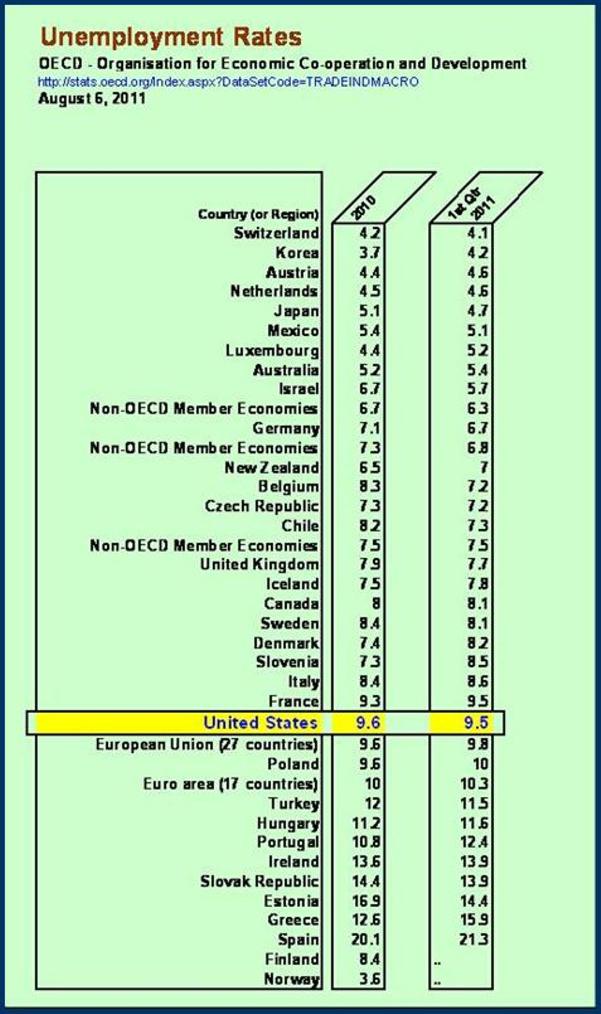

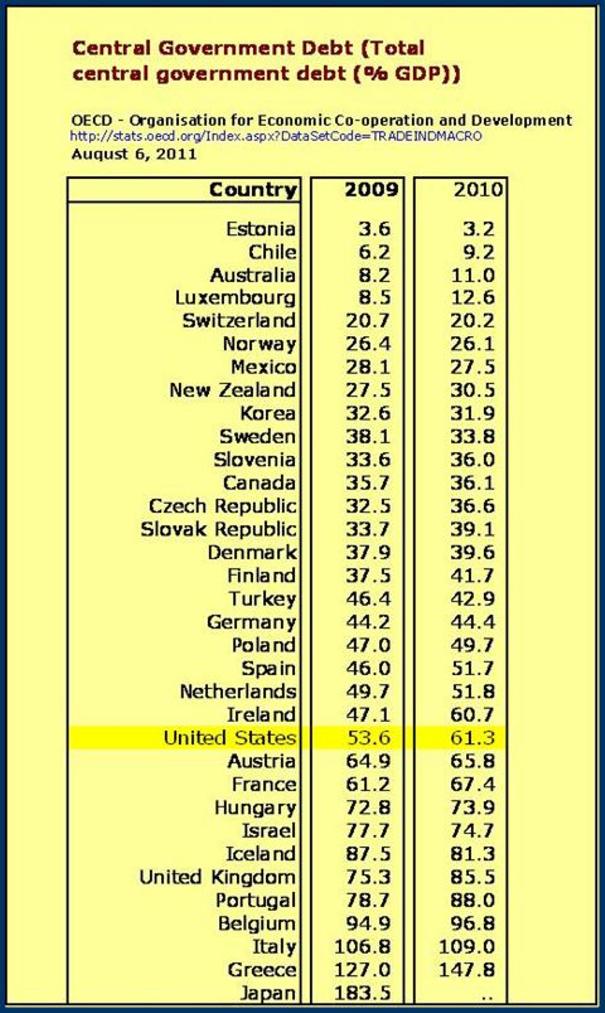

Perhaps the pessimists regarding government intervention may have something to add to the debate. Is more government the solution or is government failure just as bad if not worse than market failure? Creeping socialism does not seem to have helped Europe – see the following tables.

Could tax rate decreases be the answer?

Arthur Laffer has suggested just that on several occasions. Cut the tax rates and grow the tax base. We still have a bit of room left if the financial markets are convinced that continuance of deficits in the Federal budget will bring about a recovery. We cannot, however, wait much longer as the ratio of Federal debt to GDP is rising rapidly. These huge, TRILLION PLUS DOLLAR DEFICITS BEGAN WITH a Federal debt in the $11 to $12 trillion dollar range. That has now climbed to close to $15 trillion dollar range. In terms of GDP, the ratio of the Federal Government debt has risen. The Federal debt as a percentage of GDP rose in one year from 2009 to 2010 from 53.6% to 61.3%. While it is nowhere near as bad as that of Greece and Portugal, it is greater than the Netherlands, Germany, and Sweden as the accompanying table shows.

As we have asked before on this web site, is the goal a fast recovery from the depths in which we are floundering or is it to move toward more government and socialism? We had better get serious and give some thought to these broader issues. Delays usually eliminate many of the better solutions leaving only some of the worst as fallback, or dare we say – default solutions.

ANOTHER QUICK, YET PAINFUL WALK THROUGH EMPLOYMENT- July 2011

…The net result is that this drives down the Labor Force Participation Rate to its 28 year low of 63.9%.

…Again, as we pointed out in a previous newsletter article (Down the Rabbit Hole), in May 2011 we needed on the order of 525,000 jobs per month over the subsequent 2-years to reach 66.2% Labor Force Participation Rate and 5% unemployment rate, both modest goals.

A last case in point is that where once we had a distinct advantage in terms of consistently lower overall unemployment rates relative to Europe, we are currently foundering even in that regard, with no clear path forward…