2012 Volume Issue 1

January 12, 2012

For a downloadable version, click the following:

Why are interest rates so low? pdf

Why are interest rates so low?

The very short-term interest rate on debt securities of one year to maturity or less, when adjusted for risk, are near or less than 1%, with some approaching zero percent. Despite the increasing threat of sovereign risk, U.S. Government 10 years to maturity trade with a yield around 2% (having gone as low as 1.82% in recent weeks). Even the thirty-year U.S. Government securities are less than 4%. Our Austrian school friends should be yelling that mal-investment is occurring. We shall examine this fear later in this article.

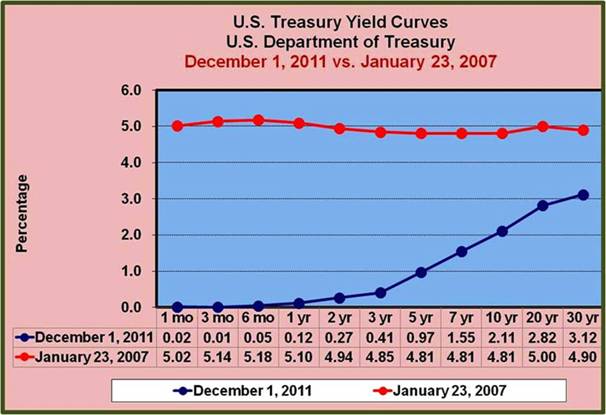

In contrast to the current status of the yield curve (graph of the term structure of interest rates), let's compare the yield curve of U.S. Government securities as it was at some other times such as in 2007, before the Financial-fiasco-of-Two-Thousand-and-Eight began, for short, FFTTE. It is relatively flat – that is to say high at the short end of the market due to restrictive monetary policy (Fed pressuring short-term interest rates upward).

The reader might find it useful to read or re-read earlier newsletter articles on this website when we delved deeply into the behavior of interest rates.

Miracles or Mayhem

What is the Federal Reserve really doing???

(May 15, 2011)

www.econnewsletter.com/may152011.html

When the FED [Federal Reserve – Federal Open Market Committee] decided to drive up interest rates, it was an ill-advised policy since it was one of the major factors that led to the financial fiasco of 2008: operating in only the short term end of the government securities market, they lacked sufficient holdings of the longer term securities to directly impact longer term interest rates.

The dominant theory of the yield curve (the graph of the term structure of interest rates) is the Expectations Theory

(www.econnewsletter.com/apr292005.html). It argues that longer term interest rates are the geometric average of expected short term interest rates over the relevant time period. Lacking a sufficient long term government securities portfolio, The FED could not directly impact the longer term rates through its open market operations, and as a result the market expectations of future short term interest rates dominated the yield curve which flattened and even inverted as short term interest rates rose relative to the longer term interest rates.

The Fed and FOMC

OPEN MARKET OPERATIONS HAVE BEEN – AND - WILL CONTINUE TO BE THE FED'S CHIEF TOOL FOR IMPLEMENTING ITS MONETARY POLICY DECISIONS

October 12, 2011

www.econnewsletter.com/oct122011.html

Recall the inverse relationship between interest rates and security prices. The causality runs both ways: when interest rates rise, security prices fall; and when interest rates fall, security prices rise. The interest rates are the discount rates that determine the discounted present values or market prices of the securities in question. When the FED wants to drive interest rates down as in the QE 1-3 (en.wikipedia.org/wiki/Quantitative_easing), it purchases securities. These actions increased the demand for the securities and caused the price to rise resulting in the yields or interest rates on them to fall.

As will be examined shortly in this article, such current low interest rates pose significant interest rate risk when the rates return to more –normal' levels. Just as some made huge profits by holding debt securities when interest rates collapsed in the early 1980s, holding such securities currently could lead to wealth-killing moves in the price of debt securities when - not if - but when, interest rates return to more normal levels.

In order to understand why an interest rate is relatively high or low and why it changes over time, we prefer to treat an interest rate such as the one-year Treasury bill rate or a 30-year fixed mortgage rate as a composite of factors and examine each of these factors separately. Since we have examined the behavior of interest at other particular times in other articles on this web site, our analysis in this current article will consist of trisecting the current interest rate picture into three factors: the pure interest rate; an inflation premium or deflation discount; and various structures such as the risk structure, term structure and tax structure.

Example 30-year Mortgage

- Pure Interest Rate: 2.0%

- Inflation Premium: 1.0%

- Risk structure: 1.0%

- Term structure: 1.5%

- *Tax structure: -1.0%

*Which would quickly rise to zero if deductibility of interest on mortgage debt was eliminated.

(Composite Rate) Mortgage Rate: 4.5%

The first two components are more or less common to all interest rate. The third set of components is the chief cause of why there are so many different interest rates. Each component can go its own way, so to speak.

Since earlier newsletters on this web site have analyzed interest rates at earlier times, we will focus on the current interest rate picture.

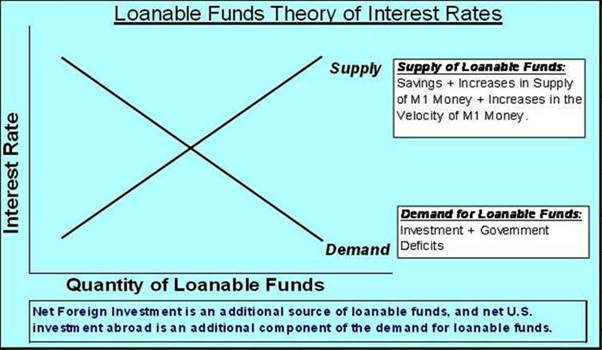

THEORIES OF THE LEVEL OF THE PURE INTEREST RATES; LIQUIDITY PREFERENCE VERSUS LOANABLE FUNDS

Remember that an interest rate is a price and hence is determined by supply and demand. While in the liquidity preference theory of interest rates popularized by John Maynard Keynes, the interest rate is determined by the supply of and demand for M-1 money, we shall use the broader and more inclusive loanable funds theory, as it has evolved from the older classical theory of interest rates. In the loanable funds theory, the interest rate is determined by the supply of and demand for credit.

Economic Ideas that Influence Policy Makers

Monetarism and its diminishing Relevance in the American Economy

February 16, 2004

www.econnewsletter.com/feb162004.html

Both the Wicksellian and Austrian arguments rest on the old classical theory of interest rates, where saving and investment determine the natural interest rates. As that theory was amended including contributions of Wicksell, it has evolved into the Loanable Funds Theory of Interest Rates. Economic historians such as John Gurley and Edward Shaw recognized that other sources of credit (such as increases in the velocity of money) as contributing to more rapid economic growth by driving down interest rates and accelerating the rate of capital accumulation.

Modern financial theory does not deny that mistakes occur by firms in undertaking some expansion requiring capital, but is more due to errors in forecasting future cash flows rather than artificially low interest rates. If one were to look at real interest rates rather than nominal or market rates…interest rates in the inflation-adjusted sense have changed far less than have nominal or market rates of interest not so adjusted.

THE PURE RATE OF INTEREST

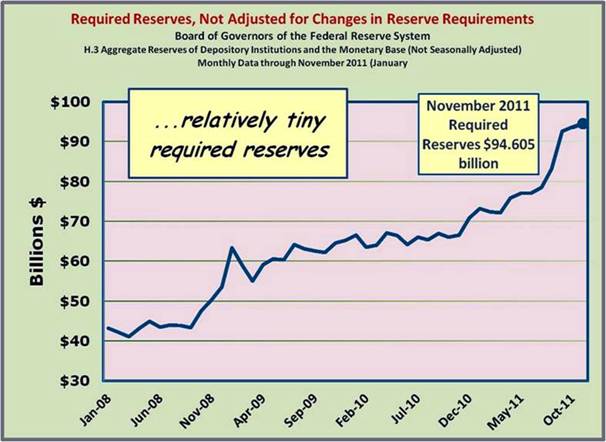

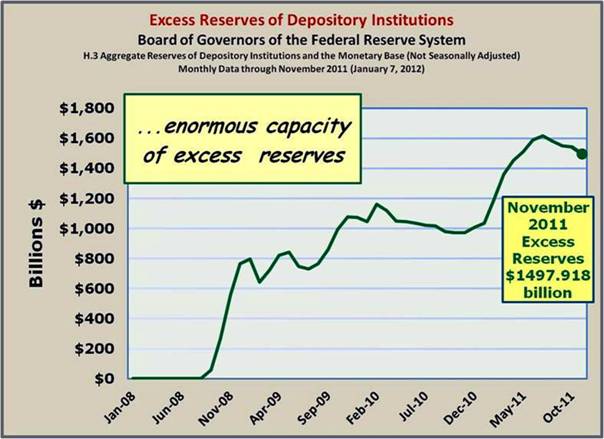

The pure interest rate is what supply and demand would determine if there was no risk present and none expected, no change in the average of prices and none expected, no segmentation of financial markets, etc. Estimates of the range of the pure interest rate over time average about 2% with a range of about 1% to 3%. With the economy experiencing very little economic growth and unemployment rates, however measured from U-1 thro ugh U-6 being very high by historical standards, the pure interest rate is at or near its historical bottom. This is partly due to the FED (Federal Reserve) assuring that the supply of credit will be ample at least in terms of the capacity to create it resulting from a series of quantitative easings called the QEs 1-3. Adding to the factors making the pure interest rate being at near its bottom, is a lack of demand for credit by business and households as they hunker down or are very uncertain due to such factors as the health care legislation that passed and is law and the threats of tax increases.

CHANGES IN THE PRICE LEVEL, A SECOND MAJOR FACTOR IN DETERMINING CURRENT RATES OF INTEREST BOTH NOMINAL AND REAL

Officially, the core rate of inflation appears to be rather mild. The overall rate of inflation is a bit higher, especially due to food prices. While energy prices are high, they have been that way for several years as a result of the re-cartelization of the U.S. portion of the oil industry. The problem is compounded by our nonsensical environmental policies concerning ethanol and the domestic production and use of fossil fuels especially in the production of electricity. The energy price picture is also significantly impacted by the re-cartelization of the American segment of the crude oil industry and its downstream refined products. That re-cartelization occurred from about 1993 to 2003 and weighs heavily on today's market and the determination of such prices.

THE ECONOMICS OF CRUDE OIL PRICES AND THE IMPACT OF COMPETITION, OR THE LACK THEREOF

August 22, 2011

www.econnewsletter.com/aug222011.html

In the most recent supply restriction beginning in 2004, the newly re-cartelized American segment of the oil industry unofficially joined the OPEC thugs and declared they would abide by the market. Of course a market with a cartelized structure which was completed between 1993 and 2003 is not a competitive market unlike that of some cereal grains such as wheat which would come close to a perfectly competitive market if government would cease its intervention as embodied in its farm policies.

As this website has pointed out, some of the inflation data for the last two years or so is suspect because of the de-contenting of products. While some products are tracked by weight, many subtle (and not so subtle) changes are much more difficult to track; quality may be suffering as well. Persistent quality improvements were always an argument; that official inflation rates were biased upward by not being able to adjust for quality improvements. The opposite argument seems more likely to have occurred in many cases since the level of economic activity hit the skids in 2008.

INFLATION BY DECONTENTING

Less roll for your buck?

February 12, 2011

www.econnewsletter.com/feb122011.html

It appears than many firms have decided to effectively increase the prices of their product by what has come to be called DECONTENTING. This means to give the consumer less for the same price either in terms of quantity and/or quality.

Such chicanery may not be reflected in official inflation rates but it has caused a weakness in consumer spending and has helped prolong the agony of the Great Recession that the high unemployment rates indicates, still exists.

Given the state of the housing and labor markets, acceleration in inflation seems unlikely for a year or so. While the series of Quantitative Easing policies of the FED have supplied plenty of capacity for the creation of money and credit and accompanying inflationary pressures, that capacity has been idle and legal reserves pile up as excess reserves. On balance, it seems that there is little or no inflation premium embedded in market rates of interest. Keep in mind that the picture could change rapidly, however.

INTEREST RATE DIVERSITY; RISK, TERM AND TAX STRUCTURES, THE THIRD FACTOR IN DETERMINING THE MARKET RATES OF INTEREST

First we shall examine the risk structure of interest rates. Recall that this is the relationship of the risk premium to the bearing of financial risk. It is often referred to as the risk-reward relationship.

The risk in finance is the uncertainty of the expected cash flow from investing. In case you have not noticed, nothing is really guaranteed and often cash flows, not guaranteed, are effectively made more certain by such reckless policies as the "too big to fail" doctrine. This in turn is a way of saying, protect the old boy network… you know, investment bankers, large so-called hedge funds, et al.

Ignoring the plethora of intellectual and moral gaffs in respect to national policies related to financial risk, in –normal' times the greater the volatility of expected cash flows from an investment, all else equal, the greater the risk premium and the higher the reward on such investments the market demands. This is true whether the investment is on claims issued by households, business or governments.

A number of factors point toward a higher risk premium in several financial markets. If the bankruptcy settlement of GM establishes a new trend where the bond holders no longer become the owners or stockholders, but rather, the labor force, or rather the unions representing labor become the owners along with government who decided to bail them out; it increases the uncertainty for bond holders.

UAW Makes Out (Again) on GM Bankruptcy

Submitted by Mark Modica on Thu, 01/13/2011

nlpc.org/stories/2011/01/13/uaw

Let's Not Forget Ethical Shortcomings of Auto Bailout

Submitted by Mark Modica on Tue, 06/28/2011

nlpc.org/stories/2011/06/28/ex–car–czar

Modica: Will State & Muni Bondholders Get Crushed to Benefit Unions?

Submitted by Peter Flaherty on Wed, 02/02/2011

nlpc.org/stories/2011/02/02/modica

If this trend continues in bankruptcy settlements it will increase the risk premium of debt capital, raising the cost of capital to firms, especially to those using significant debt or financial leverage. This would then tend to result in reduced level of debt or financial leverage and firms would have to raise operating leverage in the attempt to offset this reduced financial leverage and so on. The point is that by connecting the dots, seemingly unrelated occurrences come together to paint a far different picture.

The following will be very helpful in understanding the concept of leverage…

IS THE FED TIGHTENING THE SCREWS ON BANK LENDING?

…risk based capital ratios reconsidered

www.econnewsletter.com/jul162011.html

As pointed out earlier, the cost of equity capital, or the market's required rate of return on equity investments is predominantly related to the uncertainty and volatility of the cash flows from such investments. The roller coaster performance of the stock market increases such volatility.

Commercial banks have become a competitor with longer-term capital markets, especially the bond market. After WWII the commercial banks moved from the commercial loan doctrine to management philosophies that accepted more risk in order to raise profits and operating leverage. Regulatory practices to rein in such a high level of risk taking such as higher capital ratios have reduced the effective degree of financial leverage and have increased the pressure for higher profits to raise the operating leverage in order to prevent the decline of the return on equity. As we have written elsewhere on this website, chasing higher profits really means accepting higher risks. This is a real –Catch 22' and may force commercial banks back to more of a short-term lender than they have been in recent years.

Other factors such as the recent experience in the mortgage lending market either directly or indirectly by investing in collateralized debt obligations including mortgage backed securities have caused many banks to re-think their business plans. The gist of all this is that relying on bank supplied credit will be more expensive at each level of risk taking.

This all points to a steeper reward to risk relationship and is another contributor to firm's facing higher costs of capital.

THE TERM STRUCTURE AND FUTURE INTEREST RATES

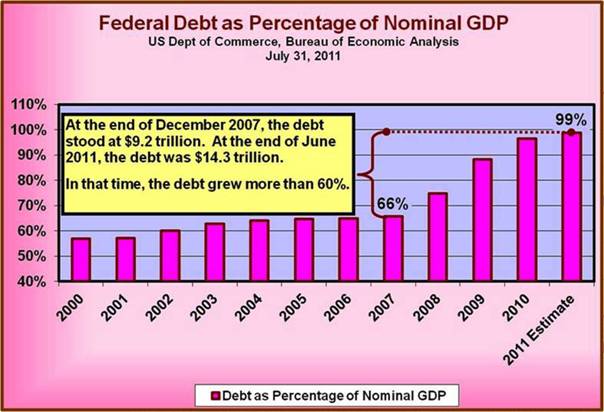

In this section we will base our examination on the expectation theory of the term structure of interest rates. The probability of short-term interest rates rising is greater the lower are those short-term interest rates. Considering the term structure of U.S. Government marketable securities, these short-term interest rates are indeed very low due especially to the FED's QE 1-3 policies. Despite the rapidly rising ratio of U.S. National debt to GDP, compared to other alternatives such as the debt of European Union nations e. g., the dollar is still the safe haven for –flights to quality', especially U.S. Government marketable securities.

When a solid recovery begins, the FED will quickly warn of their heightened concern for inflation. If the FED fears significant inflation will occur, they will quickly change monetary policy to one of monetary restraint. The problem is that just as in the immediate post World War II period, a large amount of excess legal reserves has accumulated along with a pent up demand due to wartime shortages of consumer durable goods, so to have a large amount of excess legal reserves accumulated and if rapid job growth occurred to re-fuel a moribund level of consumer spending, a pent up consumer demand would probably occur. What could the FED do? It could raise legal reserve ratios converting excess legal reserves in to required legal reserves as they have previously in such situations. Alternately, or in combination with such increase in legal reserve ratios, they could reduce their security holdings. Some of this would have occurred as debt holdings reached their maturity dates and could be allowed to run off. Remember the mortgage backed securities have a much shorter effective maturity than appears due to pay offs and in the last few years foreclosures.

This would certainly slow any recovery. The FED since 1980 has shown little tolerance to the increase in inflationary pressures as their policies such as the one helping trigger higher adjustable mortgage rates beginning in June 2004 and reversing course in the fall of 2007 well into the collapse of the financial system. When it comes to combating inflation, the FED has shown itself to have a –damn the torpedoes attitude'.

(The Financial Fiasco of Two-Thousand Eight (FFTTE))

January 2, 2009

www.econnewsletter.com/jan022009.html

In this very newsletter, again back in January 2006, we warned of the dire results of two "Killing Fields" that were devouring the public's discretionary income. Those two factors that were to ignite the explosion of the financial system were the historically high energy prices reflected in the price of crude oil peaking around $145 per barrel and rising mortgage payments resulting from the FED's ill advised policy of monetary restraint in 2004. The financial fiasco came to be, with the collapse of the housing market and the revelation of unacceptably bad behavior of the financial services industry led by the greed kings, the investment banking industry.

It seems pretty clear that a strengthening recovery, especially if the unemployment rates fell rapidly, would reverse the FED's current policies. The FED's FOMC (Federal Open Market Committee) is increasingly filled with appointee's of President Obama. They may be more tolerant of inflationary pressures, if they are accompanied by a faster economic recovery.

The risk premium on U.S. Government debt will depend on how large the federal budgetary deficits are and how rapidly the ratio of National Debt to GDP rises. This would affect the longer-term maturities especially hard.

Who should you trust for the good life, free market capitalism or creeping socialism?

www.econnewsletter.com/aug012011.html

It appears that sooner or later, short term interest rates will rise and appreciable so. According to the expectations theory of the term structure of interest rates, this should cause longer term interest rates to rise accordingly. As we have warned earlier in this article and in other articles on this website, such a scenario will trigger the fall in the market prices debt securities (and offset some of the rise in equity security due to rising profits), the extent of the fall increasing as the duration of the securities increases. Remember that the duration of a bond for example, increases with the time to maturity increases and is inversely related to the coupon yield (only on zero coupon securities is the duration equal to the time to maturity).

This means capital losses if the securities are sold or to avoid such, a locked-in effect could occur. If lower of cost or market or marking to the market is required, the locked in affect as a strategy of avoiding realized capital losses is negated. Institutions and individuals who –flew' to securities and avoided loans, especially variable rate loans, would sufferer significantly. This is a very realistic possibility. The default risk may fall but you will have to deal with the materialization of interest rate risk!

THE TAX STRUCTURE AND FUTURE INTEREST RATES

Remember that increasing uncertainty raises the riskiness of investing and puts upward pressure on the cost of business capital as well as the cost of borrowing by households and government. Talk of tax increases for whatever purpose reduces the expected cash flow to not only business but households as well. Lower cash flow to households in two ways: lower after tax wages and lower after tax yields on their financial assets, INCLUDING THEIR PENSION FUNDS.

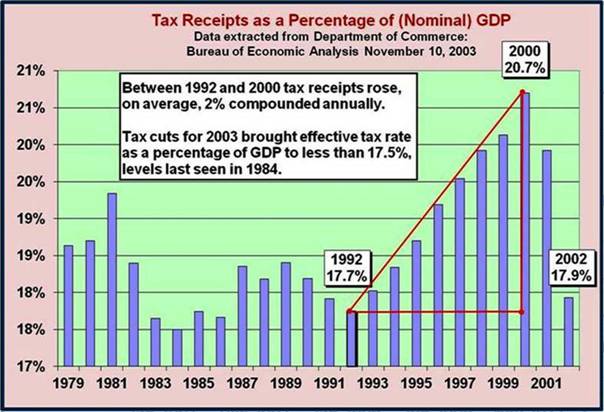

Higher tax rates, for whatever reason, will slow the recovery and slow any increase in the tax base. Remember that tax revenues are equal to the tax base times the tax rates. Such policies were tired by Hoover and FDR and failed as a previous article on the website showed very clearly from the data of the 1930s. Tax increases for the purpose of reducing the federal government's deficit and outstanding debt ultimately led to an economic collapse during the year 2000, Bill Clinton's last year as president.

A CASE STUDY IN HISTORICAL REVISIONISM

www.econnewsletter.com/dec232011.html

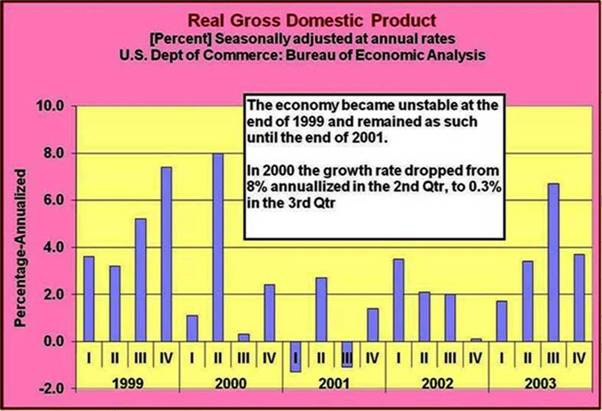

The rapidly rising tax revenues resulting from several years of tax rate increases recommended by the Treasury Secretary Robert Rubin were turning the Federal Government Budget deficit into a surplus and applying a heavy duty braking to the U.S. economy. A growing trade deficit was also applying additional braking to the economy. Shortly after the FED joined the orgy of policy restraints, the economy collapsed in the third quarter of 2000. It fell from a real growth rate of 7.3% in the Fourth Quarter of 1999 to a negative real growth rate of 0.5% in the Third Quarter of 2000 – not 2001.

If mortgage interest is no longer deductible, it will raise the cost of housing to households be they renters or home owners. In turn this will reduce consumer spending on other areas such as services and non-durables, and durables.

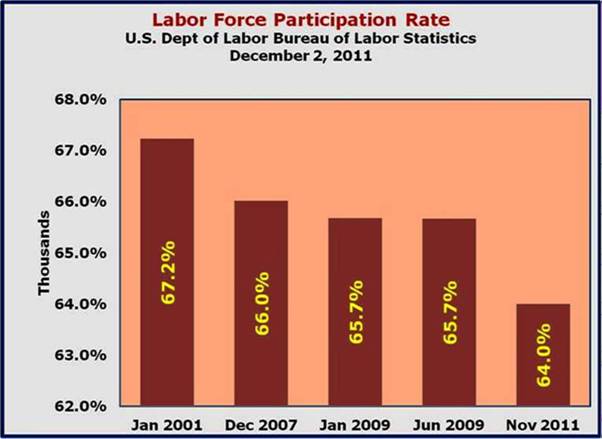

Interest rates will rise, that is certain. The real question is when. That in turn depends upon when the rate of economic growth will increase and the unemployment rates will fall AND THE LABOR FORCE PARTICIPATION RATE RISES TO A MORE NORMAL LEVEL.

Lies, Damned lies, and Statistics

www.econnewsletter.com/dec052011.html

Labor force Participation Rate

The labor force participation rate represents the proportion of the civilian noninstitutional population that is in the labor force. This measure of labor force activity grew from about 60 percent nationally in 1970 to about 67 percent in 2000, with much of the increase resulting from increased participation by women.

From April 1996 through March 2001, the average Labor Force Participation Rate was 67.1%. In our presentation, we adjusted the reported rates to reflect the 67.1% to identify the discouraged workers who have entirely given up any hope of gaining employment. When you experience lengthy bouts of unemployment, the discouraged worker effect is amplified, beyond even the normal levels when shorter term unemployment cycles occur.

Labor Force Participation Rate

- January 2001 = 67.2%

- November 2011 = 64.0%

- Difference = -3.2%

There is already a significant redistribution of income built into the current tax structures. A greater degree of income redistribution will not create jobs but only defer the day when the economic growth rate and the rate of economic recovery will assume a rate high enough to reduce the unemployment rate. None of this is speculative. History is the experimental lab for the social sciences such as economic and finance. Learn history of you will live to repeat it as Santayana warned us.